It’s been three weeks since President Bola Tinubu assumed office, and Nigerians are getting a clearer picture of his economic plans for the country.

In May 2023, Tinubu’s Policy Advisory Council developed a report that wants to double Nigeria’s economy to become a trillion-dollar one by 2031. The 50-page report only became publicly available last week. We went through it to highlight some key findings.

Senator Tokunbo Abiru chaired the economic sub-committee that drafted this report. The committee also comprised Yemi Cardoso, Samaila Zubairu, and Doris Anite. The audit and advisory firm KPMG contributed to this report.

[Source: Policy Advisory Council Report, May 2023]

What are the highlights of the report?

The report identified five areas of focus that it wants to pursue to hit its big targets.

[Source: Policy Advisory Council Report, May 2023]

On the fiscal side, the government says it wants to boost revenue, lower expenditure, and refinance debt. It has moved to lower expenditure by removing the fuel subsidy, shifting the burden from the government to the people. To generate revenue, this government will aggressively focus on deepening tax collection. It will also “rationalise select government assets.” (A finance term that means reorganising assets to make them more efficient to boost a company’s bottom line.) This can be achieved by either divesting the assets or selling them off.

[Source: Policy Advisory Council Report, May 2023]

The government is also looking to address oil theft. It wants to achieve this by expanding security contracts in the Niger Delta. Taken at face value, this might explain Asari Dokubo’s visit to the villa last week, which in all likelihood, wasn’t just a courtesy visit but at the invitation of the President.

The report also speaks on boosting Nigeria’s oil production and making Ministries, Departments & Agencies (MDA) more efficient by implementing the Oronsaye report to remove duplicity.

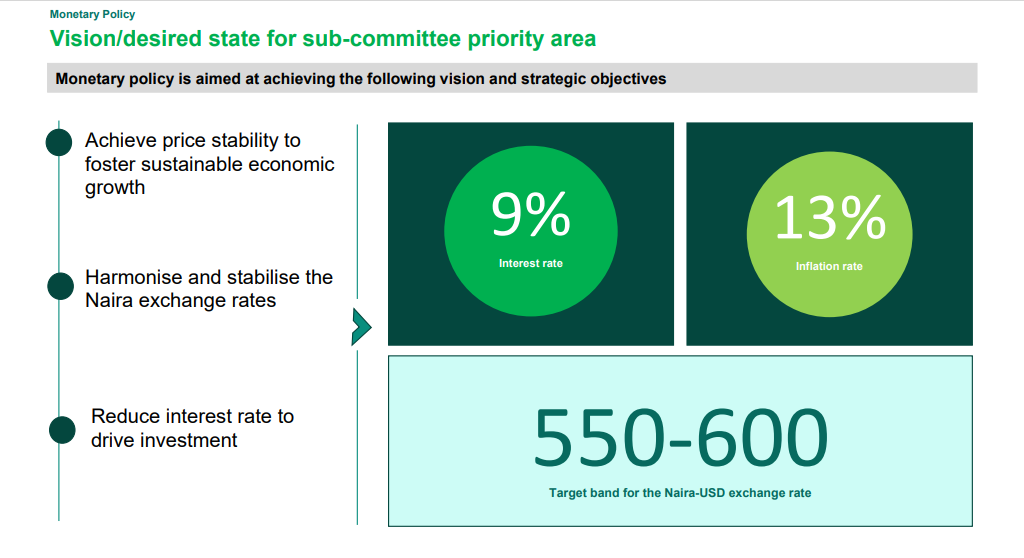

The monetary policy goal is to keep the exchange rate within ₦550-600 to the dollar and to bring inflation and interest rates to 13% and nine per cent, respectively. Currently, inflation is at 22.41%, and the interest rate is at 18.5%. We explained here why that’s bad.

[Source: Policy Advisory Council Report, May 2023]

There are also suggestions to extend the deadline for turning in old notes to December 31, 2024.

Under industry and trade, plans are to boost the manufacturing sector’s output to $50 billion annually. The agenda includes training 100,000 artisans annually, subsidising interest rates for manufacturers, creating a five per cent tax incentive, leveraging on a ₦9 trillion pension fund and passing a foreclosure law to “deepen credit penetration.”

The highlight for the capital market is to make data more accurate and eliminate multiple taxes that can put off investors.

How feasible are these objectives?

The report rehashes some worn-out promises we’ve heard from the previous administration, like lifting 100 million Nigerians out of poverty. It’s one thing that’s sweet to say but very hard to achieve. Buhari’s terrible economic record points to that, having thrown 133 million Nigerians into multidimensional poverty.

There are also doubts about how workable these plans are. First, consider the growth numbers. Let’s look at Buhari’s numbers:

Tinubu is saying he’ll rebound the economy to grow at an average of seven per cent. Frankly speaking, pulling that off would be nothing short of a miracle. The plan to double our economy into a trillion-dollar one in eight years is just as incredible. It might be best to file that under wishful thinking.

For one, mathematics doesn’t support it. In finance, there’s a rule of thumb known as the Rule of 72. It’s a shortcut to calculate the time it takes for anything to double, be it an investment, the GDP, or the population. All you need to do is divide 72 by the rate of return.

That means that even if seven per cent were to happen, GDP wouldn’t double for at least another eleven years. KPMG, which consulted on the report, seems to agree, which is why it said earlier in June that Tinubu’s plan to grow the economy at six per cent on average in his first four years isn’t feasible. They said the best-case scenario is hitting 4-4.5%. Factoring in the devaluation of the naira, this revised estimate means it may take Nigeria even longer to hit the trillion-dollar mark.

The goal to create 50 million jobs is also questionable in light of Nigeria’s high unemployment rate. One observation about the government so far is that it asks for concessions from Nigerians without making any itself. Its palliative goals are, in its words, “non-cash”, like public transport vouchers, education, and healthcare support. But it’s silent on how it wants to do it, just as it’s silent on what the new minimum wage will be.

The plan to outsource the security of pipelines to “contractors” signals that it’s business as usual. We wish the government good luck in this venture.

The foreclosure law, which it plans to pass to deepen credit financing, needs clarity. This is vital. The government wants to encourage mortgaging as a means to access loans, following which, in the case of a default, the government seizes control of the property.

Final words

So far, Tinubu has hit the ground running as promised. Yet, in the face of growing pains coming from the subsidy removal and the high cost of living, the patience of Nigerians may quickly grow thin.

As political commentator Feyi Fawehinmi puts it in the Financial Times, “Tinubu’s early moves have all been plucking low-hanging fruits. But you still have to credit him for bothering to pluck them.

“The bar is incredibly low. Buhari did not bother to pluck any fruits, low hanging or not. Tinubu will eventually run out of easy wins; the test starts then.”

Download the Citizen Election Report: Navigating Nigeria’s Political Journey