About two years ago, the federal government announced plans to finally renovate the National Theatre. The government handed the project over to the CBN’s Bankers’ Committee, who worked with an initial budget of $100 million. But on December 10, 2022, Meffy said it would take about $200 million —an estimated ₦89 billion — to complete the project.

Judging by how expensive the project is, you may wonder why this national monument is necessary and why the government is willing to spend so much money on it.

The history of the National Theatre

The National Theatre, located in Iganmu, Lagos State, is often referred to as the home of entertainment and performing arts. It’s to Nigeria what the Sydney Opera House is to Australia and also, it’s to many of our parents what malls and cinemas are to us now.

The construction of this military hat-shaped landmark started in 1973 and was completed during the regime of General Olusegun Obasanjo in 1976. It was the centre for preserving and promoting black arts and culture and housed banquet halls, two cinema halls and a world-class 5000-seater amphitheatre. It also hosted many historical events, people, and shows like the Festival of Arts and Culture in 1977 (FESTAC ‘77), Fela Anikulapo-Kuti and Stevie Wonder.

Unfortunately, as with most things in this country, the theatre fell into poor management, and it wasn’t long before it entered a state of deterioration and left at the mercy of hoodlums.

The renovation of this national monument wouldn’t only fix the damaged parts of the theatre but also restore over 70 historical artworks and sculptures.

Why’s this renovation necessary?

Job creation

Unlike the naira redesign, which is creating some new problems, the restoration of the National Theatre is projected to create over 1,000 jobs. This would be a big relief considering Nigeria’s unemployment rate is at 33%. It’s not a lot, but it’s something.

It would diversify the economy

A significant problem Nigeria has is the government’s obsession with oil money, so it more often than not seems like they’ve turned a blind eye to many other sources of revenue. According to Meffy, India makes about $240 billion from exporting movies, music, fashion and technology. With this renovation, we’d finally be able to earn billions with the creative industry and compete internationally.

Tourism

The renovations include plans to create hubs and centres to showcase our fashion, music, film and technology. This should encourage foreign investors and open up a way for the monument to serve fully as a tourist site.

The renovation of the National Theatre is expected to be completed in May 2023. Hopefully, with the funds injected into this project, this national monument will be restored to its former glory.

Are you bougie like the dollar or are your ways stressful and confusing like the naira? Take this quiz and we’ll tell you which currency matches your energy.

We’ll dash you (fake) $1m on this quiz. Spend it and we’ll suggest a career that fits you.

Much like everything else in Nigeria, it’s a hard time for the naira. The currency’s value against the dollar has been falling for decades. But the alarming freefall of what little value it has left seems to suggest it doesn’t have a praying mother.

…only a praying father

The naira slumped to N710 per $1 at the parallel market just days after we also found out Nigeria doesn’t earn as much as it needs to service debt. The naira’s depreciation is at the worst level it’s ever been, and right now, it’s barely hanging on for dear life.

The naira’s race to the bottom

One of the reasons for the naira’s troubles is the scarcity of dollars in the official Investors & Exporters window. This has pushed many to the parallel market where Bureau De Change (BDC) operators are king.

Nigeria’s foreign exchange earnings are derived from crude oil export profits, proceeds from non-oil exports, diaspora remittances and foreign direct investment (FDI). But all these channels have been inadequate in plugging the dollar shortage in the market.

The rising inflation rate, which hit 18.6% in June, has further damaged trust in the naira and fueled even more demand for dollars.

It’s so bad that the governor of the Central Bank of Nigeria (CBN), Godwin Emefiele, was desperate enough to threaten Nigerians not to buy dollars with the naira. And speaking of that guy….

Meffy the naira crusader

Emefiele (or Meffy for short) eats a big portion of the blame for the rags-to-more-rags story of the naira. When he assumed office in 2014, the dollar exchanged for ₦167 on the black market. Eight years and dozens of failed experiments later, the exchange rate has risen to ₦710 per dollar.

Meffy has done quite a terrible job, but no one can accuse him of not trying his best to cover the naira’s nakedness numerous times.

This man has given it his all. But sometimes, you cannot do more than yourself.

Meffy the naira scapegoat

On Wednesday, July 27th, 2022, senators agonised over the state of the naira because it’s touching everybody. Senator Biodun Olujimi put it best when she said, “What’s happening to the dollar [sic] is a replica of what’s happening to Nigeria.”

The senators resolved to invite Meffy to the chamber to explain the rapid depreciation of the naira to them. It’s quite like being called to the principal’s office to explain why your SS3 set is the worst in the school’s history.

Unfortunately, this meeting will take place behind closed doors and won’t be accessible to the public. But we don’t imagine Meffy has any new ideas on how to save the naira, and Buhari just wants to print more money.

We don’t know who else is out there capable of saving the naira from the further damaging disgrace that’s impacting Nigerian lives negatively. But based on his eight years of history, it’s probably not Meffy.

While we wait for a saviour, we just have one appeal to the dollar:

Earning in dollars is the new rave, but this can take longer than you want. Have you ever wondered if it’s possible to make $1000 before the week runs out? Well, it is, and Zikoko is here with answers for you.

Change your naira to Zimbabwean Dollars

You can just change your naira to Zimbabwean dollars, and it’s “mission accomplished” already. It’s still dollars anyway, no? Not everytime USD. Sometimes, support Africa.

Get a glucose guardian

It’s not even hard to do this. Just find a much older person willing to shoulder the financial responsibilities of a young adult, and you’re good to go. Whatever they want in return is just fine print and details. We’re sure you can work it out.

Become a social media political campaign officer

This is a new and vibrant job market. All you have to do is defend the most questionable crop of people we have in Nigeria — politicians. If you don’t mind all the moral baggage that comes with it, then you should have your $1000 by the end of the week.

Start selling akara

This might sound like a joke, but we’re not even kidding. Remember this tweet about how an akara seller makes ₦600k monthly? That’s a business plan waiting for you already. And if your business is five times hers, you can be pulling in your $1000 by the end of the week. See? As easy as saying beans.

Someone once said the fastest way to get rich is to be born rich, and the second fastest is to marry a rich person. We can’t help you with the first, but we have the cheat code for the second. Just tell them you’re their spirit husband or wife. It works like a charm, no pun intended. But if somehow, it doesn’t, tell them you’re from Zikoko. You’ll go straight to the altar.

Borrow and return after one week

Well, in all fairness, we said we’ll show you how to make $1000 in a week. We didn’t say anything about keeping the $1000. So just borrow the money from your rich friends and give it back to them once the week is over.

Wake up from your slumber

Because you must be dreaming. It’s not only $1000; it’s $1,000,000. You better wake up and start going to work. It’s a Monday morning.

One thing I can assure you that most humans think is money. Whether its the joy of getting it or the fear losing/not making enough of it, we’re all thinking of money. Today, we’ve going to talk about the fears people have about money.. In this article, 10 Nigerians, on different pay grades, talk about their anxieties with money.

1. “Absolutely nothing”

— Gbenga, 45

I work as a development consultant, and beyond my salary, I have slowly invested in equity and stocks. I’ve come a long way from earning in Naira. In my 20s, I understood that money comes and goes. Maybe the open relationship with my father about money helped. He earned good money as a pilot but never shied away from saying “No Gbenga, we can’t afford that.” Now that I earn $250,000 per month, nothing scares me about money. I could wake up broke tomorrow, and I’d start all over again with no worries. I have the network, so why fear?

2. “Impromptu emergencies”

— Fisayo, 26

As the breadwinner of my family, I’m scared of the uncertainty of each month. When my salary drops, I save over half of it. Not because I want to, but because I’m scared of the billings. Like the month I had to spend my entire ₦800k on my father’s dialysis. I feel like I’m in a rat race that’ll never end, and that terrifies me.

3. “I’m losing old friends as I earn more”

— Chiamaka, 31

I grew up in a village in Enugu, and the biggest fear I have about money is leaving the people I started with behind. My friends and I moved to Lagos and in seven years, I’m the only one that has consistently grown. Earning ₦1.5 million monthly doesn’t feel as great because I have to hold back on the balling I want to do.

4. “I’ll never be more”

— Sandra, 28

I worry that I’ll feel too comfortable and never make it past where I am. I’ve been earning ₦600k a month for four years and haven’t been able to move up. ₦600k isn’t even worth what it was in 2018 so it feels like I’m earning ₦200k. As the years go by, it feels like I’m regressing because Nigeria will always mess up the purchasing power of whatever I’m earning..

5. “Never making more of it”

— Paul, 30

I’m scared I’ll never make it in life. I’m earning ₦80k month at 30, and It’s hard to keep trusting I can move up the ladder.

6. “Affording luxury”

— Patricia, 27

This may seem shallow, but I’m scared of spending my whole life working without living life. I want to be able to afford designer bags, clothes, take a vacation — the fine things of life. With my ₦200k monthly salary, I’m scared it will never happen. There’s some progress in life, but I’m scared of spending my whole life working and never actually living.

7. “Finding who to spend it with”

— Fred, 38

When it comes to money, I’m worried about not finding someone to match my energy. I don’t want an entitled partner. I want someone who has big money goals and a saving culture — it’s tough on these streets. ₦5 million a month is great, but with the way the economy is, it’s also nothing.

8. “Spending all of it on my kids”

— Aisha, 45

I love them to death, but my kids are so entitled and lackadaisical with life. I have a son who’s 25 years old and has refuses to either go to college or get a job. I know it’s not helping, but I also can’t say no. As a single mother, I’m scared he’ll find a less than reputable way to get the money. I earn at least $100,000 per annum and most of it goes into indulging my kids. I really don’t know how to hold back at this point.

9. “That one day, the POS will reject my card”

— Irene, 26

₦100k a month isn’t enough money, but I’ll never hold back from a good time. How can I live a life without Alfredo pasta? For me, I just hope my card doesn’t get declined at a restaurant. I’m really not bothered about anything concerning money besides that. Overthinking how much I make won’t change anything. After all, YOLO.

10. “I think about my pension a lot”

— Ben, 77

I’m an old man, so money doesn’t mean as much to me. The only thing I think about is whether I worked enough to live on my pension. I gave 40 years to the police force and it wasn’t great money because moving up the rank was difficult. My children are there to help me, but I don’t want to be a burden. I’m not sure about how much I have left, but I hope my pension lasts until my final day my final day.

If you have $1000 and don’t know what to use it to do, we have a few practical ideas you can try. If you don’t have the $1000, fear not, you’re still our target market. We’re just preparing for when your money comes.

1) Buy crypto

So that when your mates are talking about buying the dip, you too can add your mouth to the conversation. You can’t spell drip without dip, so buy today and get ready to drip forever more. It’s not financial advice; it’s Zikoko advice.

2) Marry

If you’re already married, then marry again. It’s a very Nigerian thing to do that when you get some money, you marry. Please invite us and don’t forget that we’d like the Amala hot hot.

3) Buy a Macbook

Don’t you want to be earning 23x your current income? Then you better get ready to pivot into tech and the first step is to own a Macbook. Put your dollars to good use and get ready to Python and Java your way into success.

4) Become a demon investor

Angel investors are completely overrated. Be different, set yourself apart and drop the $1000 in a startup as ask for 90% equity. They might curse you, but that’s why you’re a demon investor. You don’t do things the normal way, you’re built different.

5) Dinner with Jay-Z

If you’re going to spend $1000 on a dinner, at least let it be a dinner with someone that has been the object of a lot of Twitter debates. Make your money work for you.

6) Start a business

In the era of akara sellers making over ₦30k in profit a day, you need to consider tapping into uncommon business ideas. How about a million-dollar beans business? A roasted corn startup? Think outside the box: Puff-puffing the unpuffed or decentralizing access to bole.

7) Do giveaway

There are a lot of people whose lives can change with just a bit of that money. You can start with us at Zikoko, it’s not like we’re begging. If the Lord puts it in your heart to bless us, who are we to say no?

[donation]

The Central Bank of Nigeria’s (CBN) governor, Godwin Emefiele, has had one job since 2015 – make ₦1 the same as $1.

The biggest problem Meffy, as he’s called by fans and haters, has faced is the management of Nigeria’s foreign exchange (FX) market.

$1 was ₦133 when he was appointed in June 2014, and we all thought that was rock bottom.

The good old days when you could fill your dinner table with just 5k

$1 now trades at ₦417 which, if you’re paying attention, is a 213.5% increment from 2014, and 41600% off the target of ₦1 = $1.

Let’s not even talk about the black market where $1 is trading for over ₦570.

Who is making Meffy’s job difficult?

Nigeria’s main FX earning is derived from crude oil export profits, which can be unstable depending on the global demand for oil, as well as pricing.

Other channels for our FX inflow are proceeds from non-oil exports, diaspora remittances, and foreign direct investment (FDI), all of which are even more unreliable than crude oil profits.

Nigeria’s unstable FX earnings put pressure on the reserves, which everyone in the country relies on for foreign trade.

One of the biggest dependents were importers who needed dollars to trade until Meffy decided they were sucking the life out of the reserves.

So he started restricting the sale of FX to importers of certain goods like pork, beef, cement, mosquito repellant coils, toothpicks, maize, sugar, and many others.

Also, bye bye foreign rice. It was nice to know you.

But Meffy was not done because foreign reserves still suffered from the Sapa wave.

Last year he accused Bureau de Change operators of sabotaging his goal of safeguarding the value of the naira.

This left just the banks as the direct recipients of dollars from the CBN who gave strict instructions regarding who they are allowed to sell to.

Banks are on the menu nowtoo

No one is safe from Meffy’s trigger fingers, and now banks may have to watch themselves or may sooner or later have their own taps closed too.

The CBN governor said at a media briefing last week that he wants the banks to start generating their export proceeds and stop bringing their begging bowls to his door.

“It is coming to an end before or at the latest the end of this year. We will tell them don’t come to the Central Bank for foreign exchange again,” he said.

Meffy’s plan

Meffy now expects banks to build their own FX earnings from their export customers to fund the demand of their import customers.

To help boost FX inflow, the CBN has launched the RT200 FX Programme. The key goal of this is to rely less on oil profits and earn more FX from non-oil exports.

Meffy expects the programme will help Nigeria earn $200 billion in FX exclusively from non-oil exports over the next three to five years.

This will be achieved by funding businesses that add value to non-oil commodities, making them more lucrative for export.

This would make it possible for Nigeria, as a major exporter of cocoa, to earn more than the $800 million it currently gets annually from the chocolate market worth over $130 billion.

According to Meffy, Nigeria had no problem meeting its FX obligations with non-oil export sources until crude oil was discovered decades ago and everybody went mad.

Import obligations were funded from exports like cocoa, palm oil, rubber, and a lot of goods that had nothing to do with oil.

Meffy wants banks to return to that past where they didn’t need dollar handouts from the CBN.

All of this hard work, we figure, is to make Meffy’s job easier as he prepares to be begged to run for president.

A Week in the Life” is a weekly Zikoko series that explores the working-class struggles of Nigerians. It captures the very spirit of what it means to hustle in Nigeria and puts you in the shoes of the subject for a week.

The subject of today’s “A Week In The Life” is a businessman who sells electronic gadgets for a living. He talks about his unconventional approach to business, being dealt with by the exchange rate and why he’s considering getting a 9-5.

MONDAY:

Today was a rough day. I woke up late, got delayed in Lagos traffic and had to pursue dispatch riders up and down. On top of that, I also had to figure out where to buy dollars at an affordable rate so I could restock my goods.

Between clueless bank officials, CBN’s ever-changing policies and dispatch riders, I had my hands full in fire fighting mode.

Frustrated by the bank, I spent a huge part of the day on the internet looking for someone who wanted to send naira home. Then I also spent some time recalculating the cost of my goods and giving room for price fluctuations.

In the middle of this, I kept on getting calls from customers asking for their goods, and dispatch riders complaining about one problem or the other.

When I could no longer bear the information overload, I put my phone on silent, paused all notifications, and went to cool my head.

I just told myself that tomorrow is another day to try again.

TUESDAY:

I run my gadget business unconventionally. I don’t own a physical store, nor have social media presence or even hold on to stock for long. I work mostly based on word of mouth referrals. I take custom orders to help people buy phones on eBay, Amazon or from trusted dealers. And when I buy stuff for myself, I sell everything off at computer village. I don’t keep any stock.

I don’t know why I’m like this. Maybe it’s because I’m not crazy about the idea of owning a store, or perhaps it’s because I dislike the processes that come with keeping stock.

My method is less stressful because I can fulfill orders on my phone. I also have a car to drive around for pickups and occasional deliveries.

I’ve been running this business like this for over 10 years, so I guess I’m doing something right. In recent times, though, the business hasn’t been as good as it used to be. I’ve gone from making 10-20% on a phone sale to making 5-8%. This means that if I used to make ₦25,000 on one sale, I now make around ₦8,000.

I blame two things: high exchange rates and losing my customer base to japa. While I don’t have the answer to stopping my customers from running away, I’d rather not dwell on the dollar matter. I don’t want to sound like a broken record.

Today, I’m going to personally deliver all the goods the dispatch riders failed to deliver yesterday. The thought of the traffic I’m going to face is discouraging me from leaving the comfort of my bed.

WEDNESDAY:

Well, I guess that there’s something in the air this week. First, I woke up to an email from Amazon saying that they had blocked my account and frozen my money. According to them, I had too many “suspicious” card activities. They didn’t even give me a chance to explain that because I’m always sourcing for affordable dollar rates, I have to use different cards from my family and friends abroad.

This afternoon, my agent called to say that my goods were experiencing delays at the port. A few minutes later, customers who had paid upfront started calling me to ask for their property. There I was, caught between not wanting to lie and not wanting to give excuses.

Well, since you asked, my day went perfectly well. How was yours?

THURSDAY:

I’m up early today, not for work but to think. In recent times, business has been slow. What was once a sweet business with highs and lows now has a lot more lows. And the hoops to jump through keep on increasing.

Now, I’m considering getting a job that serves as a safety net.

But what are the prospects out there for someone who hasn’t worked in a formal job for more than 8 months in 10 years?

I’m definitely not doing anything that requires me to submit a CV or write one foolish essay or test. . Tech sounds nice but I don’t want to code. Maybe I’ll do hardware…

Truthfully, my ideal job is one where I’m helping people solve their gadget problems. Just text me that your laptop has a problem or you’re unsure of what laptop to buy and watch me light up. Not sure what phone to get? I’m your guy. You want someone to give IT support? Na me.

I’m honestly a bit confused and my head hurts from all the thinking I’ve had to do this week.

Wo, I don’t know what the future holds, but I’m grateful for the life I currently have.

Regardless of how my job search turns out, I know I have no regrets about running a business.

Check back every Tuesday by 9 am for more “A Week In The Life ” goodness, and if you would like to be featured or you know anyone who fits the profile, fill this form.

Every week, Zikoko seeks to understand how people move the Naira in and out of their lives. Some stories will be struggle-ish, others will be bougie. All the time, it’ll be revealing.

This week’s Naira Life is brought to you by QuickCredit. With QuickCredit, you not only get the funds you need instantly, but you also get to pay back at the lowest interest rate in Nigeria.

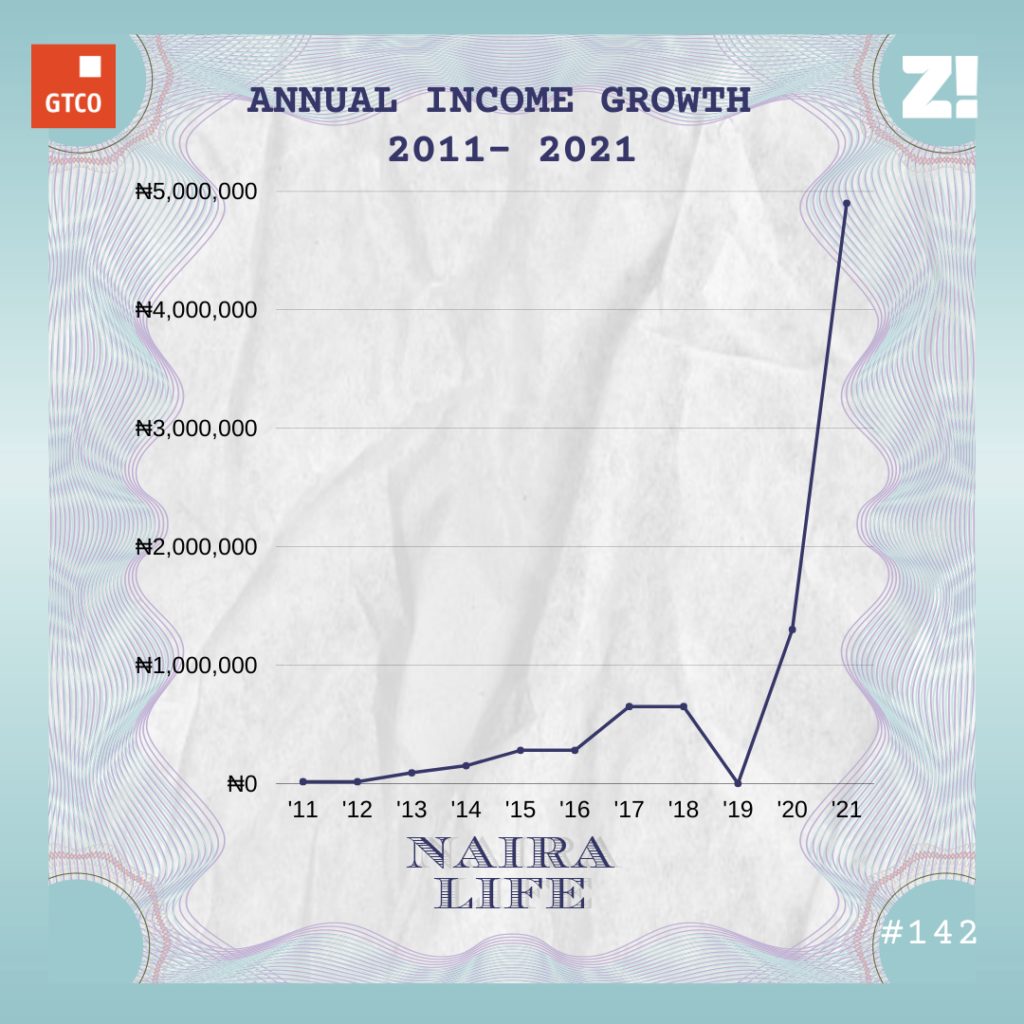

The first time the guy in this story tried to make money, he was beaten for it. Years later, he became a product manager and was slowly building up his wealth until a work mishap sent him out of a job and wiped out his life savings. Two years later, he’s building it back up and at $9800/month; it’s never been easier.

What’s your oldest memory of money?

It dates back to 1994 when I was in primary three or four, I stole ₦20 from my mum to buy some biscuits and sweets for a teacher so I could become their favourite student. I said it was from my mum. Unfortunately for me, the following week was Open Day and the teacher thanked my mum for the gifts. When we got home, she asked me to explain and I came clean. I got the beating of my life.

Wiun. Could you paint a picture of what it was like growing up?

My mum was a teacher in the civil service and my dad was a jack of all trades. What both of them made wasn’t always enough for a family of eight. Things were especially tough during periods when the government owed my mum salaries or times when my dad’s businesses didn’t do so well. We were pretty much alternating between plenty and lack for the longest time.

Do you remember the first time you made money?

1997, and I was about 10 years old. I had friends who worked at the local market. They helped people carry their goods for a fee. I asked to follow them one day to observe how they worked. After watching for a while, I joined them. I made ₦16 on that evening and was so proud of myself. Unfortunately, one of my church members saw me and reported to my mum. I got another round of beating for “embarrassing the family and making people think we were hungry.”

I don’t even remember what I used the money for anymore. But I stayed off trying to do anything for money until I got into university to study computer science. This was in 2005.

What was the next thing you did for money?

I helped someone write a math exam in the second semester of my first year, and I got ₦2k for it. I got over the guilt of what I had done when I got the money. For context, my allowance from home was ₦1k/month.

When I got to my second year, he introduced me to another guy who had missed out on school for the entire semester due to a personal tragedy. He was going to write six exams that semester, and I agreed to do it for ₦6k per course. That brought in ₦36k.

I knew it was illegal and could get into a lot of trouble, so I pivoted into something different in my third year.

What was this?

I started a tutorial centre to teach students in the lower levels. The centre caught on, and I was always booked and busy during the exam periods. On the side, I was writing final year projects and seminar papers for final year students. On average, I was making more than ₦150k per semester. I did these things until I left university in 2011. By that time, I had about ₦1m in savings.

Hmm.

One of my cousins was going to a university in the UK that year, and I started thinking about the possibility of going abroad for my master’s degree. He directed me to the affiliate centre that helped him with the whole process, and I went there to make enquiries. But I missed the floor and found myself at an I.T training centre. Somehow, the facilitator of the centre convinced me to get some certifications with them instead and showed me a pathway of how I could use this to get into tech. I thought it sounded good, so I paid for six certifications in software development and network engineering. It cost me ₦600k.

The courses lasted for six months. The centre retained me as a facilitator after I finished my programme and paid me ₦15k/month. On the side, I was also looking for a better paying job, but nothing came until NYSC in 2012.

Two weeks before my service year ended, I got a job as a systems and server admin with a contractor doing some IT work for the government.

How much was the pay?

₦90k. But I also had to be transferred to a state in the south-south. However, I was at the job for only three months. I resigned in May 2013.

Ah, why?

I found out that my chances of growth were low. On my team, there were people who had been working there for two to three years and were still at the same income level they were when they joined. I didn’t want that for myself. I’ll admit that I made the decision because I had a bit of savings. ₦450k.

Fair enough. What came after?

Unemployment. I was at home for five months.

Uh-oh.

I was getting interviews but I either didn’t think the companies I was interviewing with were the right fit for me or they were offering me ridiculous salaries. I was bent on not accepting any offer below ₦100k and these companies were offering me ₦40k or ₦50k.

By the fifth month, I had burnt through my savings and had ₦70k left. I was beginning to realise that saving money only works if you’re earning.

Thankfully, a company reached out to me in October 2013. Someone at my last job had referred me to them. I got an offer almost immediately after I did my interview. They wanted me to come join them as IT support staff and my starting salary was ₦90k. Not the ₦100k I was looking for, but it was close.

I get that. How long did you spend there?

Six months. I left in March 2014 after I got a better offer from an FMCG company. They brought me on as an IT lead and my salary was ₦150k. This was probably one of the most toxic places I’ve worked at.

Why, what happened?

First, an IT lead was the highest role for the Nigerians who worked there. The supervisor positions and other superior roles went to foreigners. So, there was no opportunity for growth for me. I spent six months there and left in August 2014 after an argument with one of the supervisors.

Here’s where it got interesting: they didn’t accept my resignation.

Why not?

A lot of the foreigners on the team were in violation of their visas, and they feared I would report them to immigration if I left like that. They gave me an offer instead: they would pay my salary for six months if I didn’t get another job within that time frame. I accepted it.

Sweet.

I got a new job lead at a fintech company about two weeks after I left. Two months and a series of interviews later, they offered me a senior IT role. My basic salary was ₦250k, but there was an extra ₦30k transport allowance, which brought my total monthly earnings to ₦280k. Another ₦150k was coming in from my last job. In total, I was earning ₦430k until November 2014. Somehow, my former workplace found out that I had gotten another job and stopped the payments.

Hehe. How did it go at the fintech company?

Oh, it was great. I spent three years there. A lot of growth and learning happened there, so I wasn’t in a rush to leave. However, I never got a salary raise even once. It probably wouldn’t have mattered much, but I got married in 2015, so I had to earn more. Ultimately, it was one of the reasons I left.

Another fintech company had been trying to bring me on board, but I didn’t give them a lot of attention. I accepted their invitation to interview when I made a decision to leave the company I was with at the time. They liked me, and I got the job. Like that, my salary grew from ₦280k to ₦650k. It was a massive move I should have made earlier.

It does seem that way.

Haha. Apart from my salary, there was at least one bulk payout in every quarter of the year: leave allowance in March, performance bonus in June, Profit from the previous business year in September, and end of the year bonus in December.

Could you tell me a bit about how you navigated money at the time?

I was saving 40% of my monthly salary. The remaining 60% was spread across other expenses, mostly household expenses and black tax. At the end of everything, my core savings was enough to cover house rent, which was ₦1.8m.

The bonuses I got on the job went into investments.

What kind of investments?

Bank investments. Treasury bills were hot and at an all-time high, bringing in 13% – 14% per year. I also had a fixed deposit account I was putting money into. By 2018, I had gathered ₦6m in core savings and investments.

Then something happened.

Uh-oh.

At the fintech where I worked, I was on a product team where we managed high network individuals. We helped them buy international portfolios and investments to reduce tax.

Everything ran smoothly until December 2018. I got a call from work and was notified that the infrastructure we used to facilitate these transactions had been exposed. What had happened was that the systems could not verify if the transactions we had made on that day to the BDCs — who were the middlemen — were successful, so we ended sending money to these people more than twice. And these were large volumes of money — $30k here, $20k there, some were more than that.

By January 2019, we had recovered most of it. But the other BDC agents went underground with the money. The total debt that was on our head was $2m.

Ehn? This sounds like a nightmare.

It was. The affected High Net Worth Individuals were on the company’s neck. Before long, the regulators got wind of it and everything spiralled out of control. My line manager resigned. I was next in line, so I had to be the fall guy.

When the regulators came knocking, they seized the assets of everyone on my team to recover the money. All the money I thought I had went up in smoke.

How much?

About ₦8.2m. They also took two cars belonging to me and my wife and some pieces of land I had bought. I was at level 0.

Damn.

The company asked me to resign, so I was without a job for the most part of 2019. Marrying my best friend saved me. My wife took over providing for the family on her ₦200k salary.

Seven other people were affected by the asset freezes, and we were fighting it in court. But I pulled out in 2019 because I realised how long court cases in Nigeria can drag on. I had to move on.

What did moving on look like for you?

For starters, I had to figure out how to make rent in October. Thankfully, there was something to look forward to.

What was that?

Before the whole situation started, I had been talking with some Chinese acquaintances about the possibility of bringing in Android POS machines into the country, and I had paid ₦700k for it. In March 2019, 10 POS machines were delivered to me. I had the infrastructure and configuration skills, but zero coding skills to integrate the POS into the Nigerian payment gateways and teach them how to read ATM cards. I went back to the same fintech company I worked at the previous year and convinced two friends to work on it with me, promising them 15% equity each. After five months, we figured it out.

Agent banking was already becoming popular in the country, so it wasn’t hard to find 10 agents. I got ₦120k in revenue from the 10 machines in the first month. It increased to ₦300k in the second month.

Then I ran into another problem.

What was it this time?

Regulators again. I got an email and they informed me that I was running the operation without a license. That’s how I was back to fighting for my life. I still had a relationship with the MD of the last fintech company I worked with, so I thought I could leverage it. After a series of back and forth, the company bought me out and paid me ₦10m for the POS machines and the solution I had built.

Whew.

I paid my guys ₦1.5m each per our equity agreement, ₦2m fine to the regulators and paid my rent, which had been due for a month. At the end of everything, I had ₦3m left. Things were beginning to look up again.

Did you ever get another job?

I did in the same month. My former boss came through again and referred me to a company that needed somebody to manage their payment gateway. The salary was ₦350k.

It was less than what I earned at my last 9-5, but it was either that or rely on the ₦3m I had left. I spent only three months there and left in January 2020. The people there weren’t open to change and preferred to stick with their old ways of doing things.

The same week I left, I got a call from an oil and gas company. They were looking to build a product for efficient fuelling for their fleet offshore and someone had referred me to them. I got a six-month contract as senior product manager for the product. ₦750k per month. When I left, I had built my savings to about ₦5m.

Then I got another job.

Tell me about it.

I wasn’t even keen on another 9-5, but it was a digital bank and the offer was good. ₦1.3m. It’s funny when I think about it now, but it took me about eight years to hit ₦1m every month.

Inside life.

The product I was building went live in December, but I stayed two extra months before I left in February 2021. The plan was to take some time off, build and ship my own product. But I couldn’t refuse the next offer I got.

Ghen Ghen.

One of the VPs of a digital bank in South America DMed on Twitter and asked if I was interested in a senior product manager role at the bank. I got an offer from them in April 2021.

How much?

$11k gross. $9800 net. That’s about ₦4.9m per month.

Omo. How do you move money in and out now?

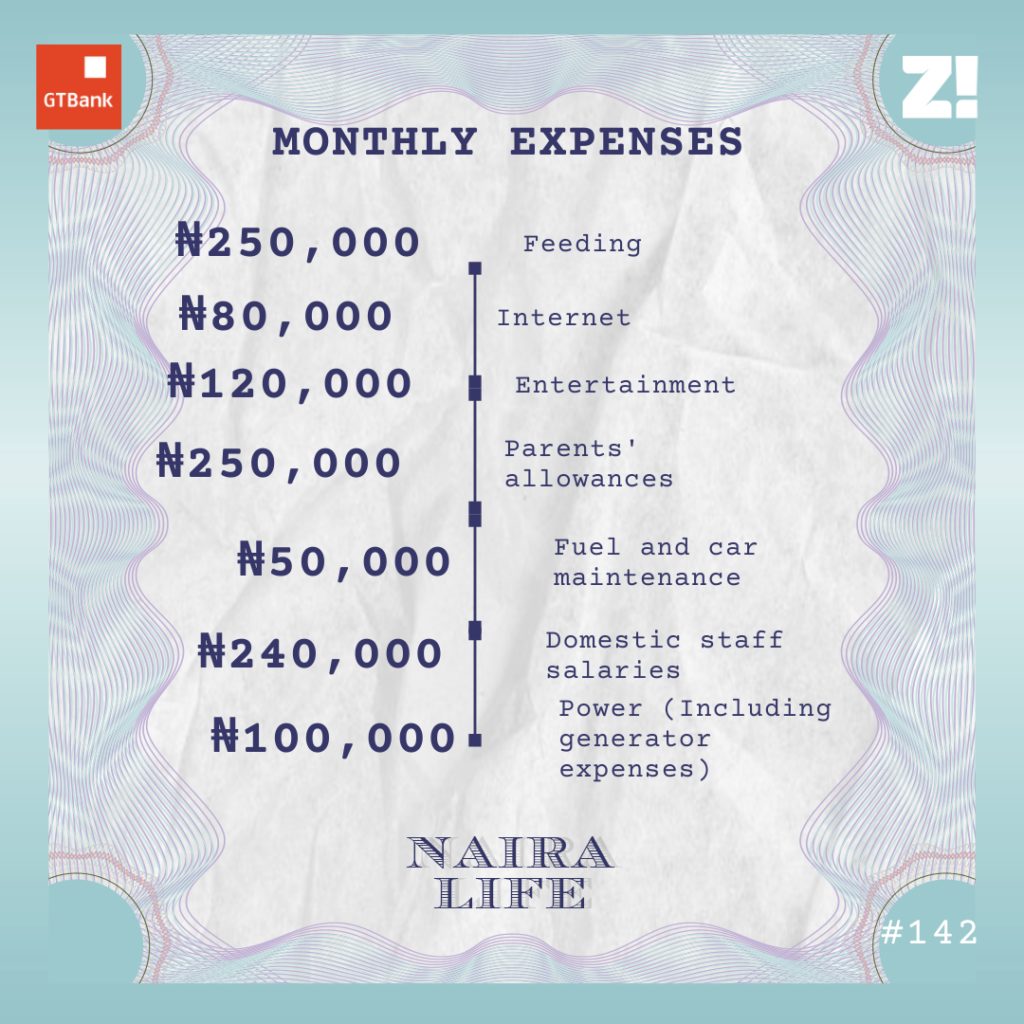

Every month, I take $2k out for my monthly running costs, $2900 for short term investments, and I leave the rest in my international bank account. My wife and I should leave the country before the end of the year because of my new job, so I’m saving for when the time comes.

Let’s start with a breakdown of your running costs.

This is not an exhaustive list, but I imagine it looks something like this.

What about your short term investments?

Every month, $900 is spread across different crypto investments. $400 goes into my PiggyVest for any emergency expenses. I put $1k in mutual funds, and this is to raise the tuition for my two kids when it’s time every three months. I also put $600 across a couple of agritech investments.

What has all of this done to your perspective about money?

First, your risk appetite is directly proportional to how much you’re earning. I’ve realised that the more I earn, the more my interest in investments grows. A couple of years ago, I wouldn’t have considered investing in crypto.

Also, whoever says money doesn’t give happiness isn’t being fair. I would know because I was at my lowest point in 2019, and I know what that did to me. I developed high blood pressure during those months that I now have to manage for the rest of my life.

I’m sorry about that.

Thank you. I’m fine. But perhaps the most important shift is realising that people who depend on you will manage without you if you don’t have money. For the entire time I was down to zero, calls from members of my extended family were non-existent. The good thing about that is it’s now easier to say no to them when they come knocking. So, maybe don’t kill yourself so others could live.

How much do you think you should be earning now?

I don’t think I should be earning a salary at this stage. I feel like I should have launched a couple of products in the market and earn money based on their market valuations. That’s one of the things I’m looking to do in the next five years.

Let’s come back to the present for a bit. Is there anything you want but can’t afford?

I’m big on family houses. I’ve been thinking about a building that would accommodate my family, my parents, and my siblings and their families. I know the location I want for this project, but I’d have to buy old properties from the current owners and tear them down, and that alone will cost about ₦90m. It’s a huge investment I can’t take on yet.

That’s an ambitious project. Is there anything you’ve bought recently that’s improved the quality of your life?

An air fryer. I bought it for health reasons, and it’s been absolutely worth it. It cost only ₦120k.

Ah, nice. Is there a question you think I should have asked but didn’t?

My financial happiness.

I was coming to that, but let’s hear it.

It’s a six. 2019 was tough, but it could have been worse. I’m also glad that I’m bouncing back. I’m not 100% fulfilled yet because I haven’t built and shipped a product for myself — all the ones I’ve worked on have been for companies I’ve worked with. When this finally happens, I’m moving up to an eight or nine.

Great! You got to the end of this article. Know what’s even better? You can get QuickCredit faster than the time it took you to read this article. With Quickcredit, GTBank customers can get N2million in less than 2 minutes and pay back over 12 months at an interest rate of 1.5%. No forms. No collateral. No hidden charges. Get Your Quick Credit on GTWorld