For many Nigerians, the idea of owning their own house often feels like an impossible dream. Every year, many people renew their rent, moving from one apartment to another, trapped in a cycle of payments that never end.

Yet across the country, a quiet initiative is taking place, one that’s giving ordinary Nigerians the chance to own houses of their own through something called a mortgage. And at the center of that revolution is the Ministry of Finance Incorporated Real Estate Investment Fund (MREIF), a government-backed initiative that’s simplifying homeownership, lowering mortgage costs, and helping thousands of Nigerians transition from tenants to proud homeowners.

A mortgage is simply a type of loan that helps you buy a home. Instead of paying the full cost of the house upfront, which for most people would be impossible, a mortgage allows you to pay gradually over a long period, usually between 10 and 20 years.

A bank or mortgage institution pays the seller of the house on your behalf, and you then repay the bank every month with a small amount of interest added. The home serves as security for the loan, meaning the bank keeps a claim on it until you’ve completed your payments. Once the mortgage is fully paid, the house is completely yours.

In simpler terms, a mortgage allows you to use the house you want to buy as collateral so you can move in today and pay over time rather than spending decades saving up before you can own a house.

While the concept sounds straightforward, mortgages in Nigeria have traditionally been expensive and inaccessible.

Most banks charge very high interest rates, sometimes over 20 percent per annum, which makes repayment unaffordable for the average income earner. In addition, many mortgage processes require large upfront deposits, strict documentation, and long waiting periods.

As a result, millions of Nigerians have chosen to keep renting instead of navigating a system that seemed designed for only the wealthy or well-connected.

That’s where the Ministry of Finance Incorporated Real Estate Investment Fund comes in. Launched by the Federal Government of Nigeria under the leadership of President Bola Tinubu, with strategic oversight from the Honourable Minister of Finance and Coordinating Minister of the Economy, Mr. Wale Edun, MREIF was created to tackle one of the country’s biggest challenges: housing affordability.

The fund, managed by ARM Investment Managers, provides long-term, low-cost financing to banks and mortgage institutions, enabling them to give Nigerians mortgages at single-digit interest rates. This means homebuyers can access financing at just 9.75% per annum rather than 20% or more in the traditional market.

At this rate, mortgage repayments become significantly lower and easier to manage.

A lower interest rate doesn’t just save borrowers money; it makes homeownership achievable for people who previously thought it was out of reach. MREIF also requires only 10% down payment, compared to the 20% or higher demanded by most financial institutions. Even better, that down payment can be funded from your Pension if you have one.

The repayment period stretches up to 20 years, allowing homeowners to spread out their payments comfortably. Because the program is backed by the Federal Government through the Ministry of Finance Incorporated, Nigerians can trust that the initiative is credible, transparent, and sustainable. It’s not just another housing scheme; it’s a structured financial solution built to last.

Applying for an MREIF mortgage is straightforward. You can visit the MREIF website at www.mreif.com.ng and sign up. After creating an account, you can choose a property from approved housing developments listed under the scheme or bring your own property that meets the eligibility requirements.

Applications can be submitted online or through any of MREIF’s partner banks and mortgage institutions, including Access Bank, Stanbic IBTC Bank, FCMB, Globus Bank, Providus Bank, Union Bank, AG Mortgage Bank, Infinity Trust Mortgage, Homebase Mortgage Bank, Abbey Mortgage Bank, Living Trust Mortgage Bank, Nigerian Police Mortgage Bank, Imperial Homes Mortgage Bank.

Once your income and documentation are verified, the mortgage is approved, and disbursement is made directly to the developer, allowing you to move in and begin repayment.

Since the launch of the fund, more than 1,000 Nigerians have successfully bought houses through the MREIF initiative. These are teachers, entrepreneurs, civil servants, and young professionals who, for years, believed homeownership was out of reach. For them, this isn’t just a financial milestone; it’s a generational one.

Owning a house creates stability, builds equity, and provides a foundation for long-term wealth. One of the key goals of MREIF is to bridge Nigeria’s housing deficit, estimated at more than 28 million units, by funding developers and making mortgages accessible for everyday Nigerians.

For Nigerians living abroad, MREIF is also providing a safe and structured way to invest in houses back home. Many Nigerians in the diaspora have struggled with unreliable real estate agents and fraudulent building arrangements. MREIF eliminates these risks by offering vetted developers, secure financing channels, and verifiable homeownership processes. Now, Nigerians abroad can buy houses confidently, knowing their investment is legitimate, protected, and government-backed.

Beyond helping individuals, MREIF is playing a major role in strengthening Nigeria’s economy. By creating demand for affordable housing, the initiative stimulates the construction sector, generates jobs, and expands access to mortgage financing. Every new house built creates opportunities for builders, engineers, artisans, and suppliers, driving inclusive economic growth.

It’s not just about owning a house; it’s about building a country where more people can live securely, plan their futures, and create intergenerational wealth.

Of course, challenges still exist. Inflation, high construction costs, and limited access to land titles continue to make housing a complex issue. But the foundation has been laid. With continued government support, active participation from banks and developers, and the growing interest of everyday Nigerians, MREIF represents a powerful shift toward real housing reform. The initiative proves that when policy, finance, and purpose come together, tangible progress is possible.

Owning a house is more than just a financial transaction. It’s about dignity, stability, and belonging. It’s about having a space to call your own, a roof that no landlord can take away, and a legacy you can pass on. Thanks to initiatives like MREIF, that dream is no longer out of reach.

Whether you’re a young professional in Otukpo, a business owner in Nnewi, or a Nigerian abroad looking to invest back home, the doors to homeownership are finally open.

Visit www.mreif.com.ng today to start your journey toward owning your home.

Every week, Zikoko seeks to understand how people move the Naira in and out of their lives. Some stories will be struggle-ish, others will be bougie. All the time, it’ll be revealing.

Tired of your money giving you zero returns? With Mkobo’s Save & Win, your ₦10,000 could turn into ₦1,000,000 —no stress, no long stories. Just save smart and win big! The more you save, the higher your chances. Click here to get started. #EveryKoboCounts

What’s your earliest memory of money?

I was 18 years old and had just finished secondary school. I needed money to pay for my exam, so I worked at a bakery for ₦100/day.

What exam?

GCE. I remember that was the one I could afford. NECO was free because it was relatively new, and WAEC was too expensive. I needed to write both, so I settled for external GCE.

I worked at the bakery until I gathered the ₦7500 exam registration fee. It was a lot of work, but also my only option to raise the money. My parents couldn’t afford it.

What did your parents do for money?

My dad was a welder, and my mum was a petty trader. They had six children, and we all lived in a single room. Try to imagine eight people living in one room. It was so bad.

I remember growing up, my dad earned ₦10k/month. He’d remove ₦3k for his transport fare and give my mum the rest to buy food for the month. On the other hand, my mum jumped from selling one thing to another, depending on which moved faster.

My siblings and I also helped her hawk these items after school. I hawked everything from kuli-kuli to fried fish and dried ponmo.

Back to the GCE. I wrote the exam and got good grades. Unfortunately, my sibling and I finished secondary school at the same time. My elder brother was also in the polytechnic. By my calculations, my parents couldn’t afford to send us all to a higher institution. I had to look for another way to make money.

Did you find any?

I did. One of my dad’s brothers drove for a banker, and I joined him at the quarters where he lived. His neighbourhood was filled with car dealers who lined cars on the road, so I started helping them wash the vehicles.

My pay was ₦10k/month, but I frequently made more from tips and extra money from my oga, especially when he made a sale. Sometimes, I made up to ₦25k or ₦30k monthly. December was the best month, especially when the diaspora guys came and paid in cash. I could make up to ₦40k in December.

Would you say it was good money?

It wasn’t mine to spend alone, so I couldn’t do much with it. I planned to save some of my salary for school, but I also had responsibilities.

I had to support my uncle. He was a driver, so he wasn’t buoyant. He had two wives back in our hometown, and travelled to see them every month. So, after I collected my salary, I’d give him ₦7k to hold. Sometimes, he borrowed money from me and never paid it back.

There was also black tax. I had to send money home to support my brother in school. Sometimes, I’d get calls from home after my brother had come home and packed all the food back to school, so of course, I’d have to send money. Then, I’d survive on the remaining money left for the month. I saved a little, but it wasn’t enough to do much.

I worked at the car dealer for about two years. Something interesting happened along the way.

Tell me about it

I started attending a church in the area, which reshaped my mind. I joined a cell group, and my cell leader helped me set values for myself; to look beyond my circumstances and see how I could be more. I knew I couldn’t continue washing cars indefinitely. My hands peeled a lot because of the water and soap. I kept praying and asking God, “What next?”

Then one day, while cleaning the cars and preparing to close, I met a pastor. His car had issues and stopped near our parking slot, so he asked me to help him. I pushed the car into the slot, and even lent him a battery from one of our cars to start his car. We tried several things. Still, the car didn’t start.

The pastor begged to drop the car there overnight, and he’d send his mechanic the next day. At this point, it was 10 p.m. I agreed, but refused the money he offered. He returned the next day with his mechanic, and I still refused money after the car started working. Surprised, he gave me his card and said I should call him. I didn’t remember to call him for days.

Ah

I stumbled on his card one Sunday after service and called him. He told me to come to his office, which wasn’t too far from where I worked. When I got there, he was with his friend. The friend asked, “Is this boy you’re talking about?” Apparently, the pastor had told him the story of how I helped him without collecting money.

To cut the story short, the pastor asked me to work with him. He was also a real estate consultant. Me that was already looking for job. I immediately agreed.

Join 1,000+ Nigerians, finance experts and industry leaders at The Naira Life Conference by Zikoko for a day of real, raw conversations about money and financial freedom. Click here to buy a ticket and secure your spot at the money event of the year, where you’ll get the practical tools to 10x your income, network with the biggest players in your industry, and level up in your career and business.

What were your duties?

I just followed him around, running errands for ₦25k/month. The errands were mostly, “Go give this survey plan to XYZ person.” I didn’t understand how real estate or surveying worked, but I wanted to learn. A fellow employee who studied estate surveying and valuation taught me the basics, but I didn’t fully understand it.

After six months of working with the pastor, I decided to leave. The ₦25k wasn’t great, considering I didn’t get tips like at the car slot. My salary hardly covered my bills. The office was also not as close to my house as the car slot, so I spent more on transportation. It wasn’t worth it.

So, what did you do next?

I decided I didn’t want to work under anyone again. I moved back home and asked around for people who could teach me surveying. I didn’t have the money to attend school, but I knew the basics and needed someone to train me.

A relative finally introduced me to a surveyor, and I put my heart and soul into learning the business. I’d trek about an hour every morning to the surveyor’s office. Once there, I’d clean, run errands, and follow the surveyors everywhere. They took me to sites, taught me to read tape, and sent me to the Ministry of Lands to process approvals. I caught on quickly and was training younger people in the office within months.

Were you getting paid?

I wasn’t working under the surveyor, so I didn’t have a salary — I was just learning the business. However, I made money from practising what I was learning and doing my own thing. I find it easy to relate to people, so I befriended many of the ministry’s staff. It helped me get a lot of opportunities.

Someone could just ask, “I want to sell this land, but I don’t have a survey plan. Can you do it?” I always said yes. I’d go there, measure, and they’d pay me. Sometimes, I charged up to ₦100k. Other times, I negotiated a percentage of the land sale.

I was the guy who knew how to do everything. Want to buy land? I can help you with the property search. Need a Certificate of Occupancy (C of O) or building approval from the ministry? It’s me. Whatever it was, I did it. People also constantly referred me for jobs.

Between 2006 and 2009, I comfortably earned up to ₦250k/month — sometimes more. I rented a mini flat, furnished it, and even had an air conditioner.

Energy!

I was making cool money. In 2009, I planned to finally go to a higher institution to get an actual certification in surveying. I even rewrote the GCE because the first one I did was for science subjects, and I needed commercial subjects for surveying. I passed, but had to pause school plans again, like the last time.

What happened this time?

I got someone pregnant. She was my church member, and the church didn’t want to hear that we had the baby outside of wedlock. So, we got married and I had to leave my school plans to focus on my family and increased responsibilities.

This was the same period I got my big break.

I’m listening

I met someone who would turn out to be my long-term business partner. Let’s call him Alhaji. We sat beside each other on a bus, and I noticed he was a property guy because he was on a call.

The person he spoke to on the phone asked him a logic question: How many acres make one hectare? The person probably wanted to make sure Alhaji knew the business he was trying to sell. I noticed Alhaji struggled with answering the question, so I whispered to him, “It’s 2.5 acres.”

After Alhaji finished his conversation, he turned to me and asked if I was a surveyor. I said yes, and he said he’d like to work with me. He was a property consultant and needed a surveyor to work hand-in-hand with him. We exchanged contacts, and within a week, I got my first big job from him: ₦10m.

Woah. How did that happen?

Alhaji had acquired a lot of land in Ibeju Lekki and Ajah, which were just springing up. He wanted to build an estate on one of those massive sites and needed someone who could handle it. It was a waterlogged area, meaning double work.

I did the job, signed the perimeter copy, and lodged the record with the ministry. Everything went smoothly, and he was happy. I was extra happy. It was the first time I made so much. I couldn’t sleep. For one week, I was just shouting.

That job was such a major step for me. Prior to this, I’d bid for jobs worth ₦2m – ₦3m, but the clients wouldn’t call me back, except when they had smaller jobs of ₦150k – ₦200k. When I asked why, they’d say I was young and clients were sceptical that I could handle big jobs. I was 24 or 25 years old.

Hmmm

I’ll forever be grateful to Alhaji for trusting me with that opportunity. He took me along on subsequent jobs, and my network expanded. I met more people who were willing to pay well for my work.

I also got a recurring gig with a telecommunications company. They needed a surveyor to convert latitude/longitude data to UTM coordinates and use that to acquire land to erect masts. Those gigs took me around Nigeria and made me good money.

How good was the money?

I made between ₦1m – ₦4m per gig, and they came consistently for a year. I built my first house that year and bought a Toyota Muscle. This was around 2010/2011 when the car had just entered Nigeria. Me too, I did big boy.

After the gig ended, I faced my regular surveying jobs, making money here and there. Then, in 2017, I started thinking about more ways to make money. I didn’t have a problem finding clients, but the ones that paid well didn’t come daily. After much thought, I decided to build a hotel. It seemed like a way to get steady business.

I discussed with a friend, and we found land near my area for ₦5m. I paid for it and did the necessary documentation. Three weeks later, my friend called and said someone just priced it for ₦7m. A ₦2m profit in less than a month? I sold the land immediately. That incident gave me the idea for my next business: buying land to resell.

How did you go about that?

I began diverting any money I made from surveying into buying land. After selling the first one, I found another full plot of land with a small house on it. I bought it for ₦12m and made an extra ₦6m after reselling.

Trust land agents, they started calling me regularly to inform me whenever land was available. I bought another one for ₦15m and sold it for ₦25m; ₦10m profit just like that. At one point, I thought, “What if I build on these lands and sell the property?” A bag of cement was still ₦2600. It wouldn’t cost me too much to build, and I’d profit even more.

So, I bought three plots of land for ₦28m. I sold part and designed the rest like a mini-estate. I built the first duplex for ₦20m, and sold it for ₦40m. I used the ₦40m to build three more house units to sell. By the time I finished the mini-estate, I had close to ₦100m in my account. It blew my mind.

I mean, my mind is blown too

Since that first experiment, building houses and mini-estates for sale has remained a consistent income source. Land value and people’s interest in it increase as soon as they see a building on it. I pay attention to the entire infrastructure, from securing NEPA poles to getting prepaid metres and interlocking the roads to ensure people invest.

I don’t build all the time. Sometimes, I just resell the land for a profit. I haven’t abandoned surveying either. My old clients still call me for surveying jobs, and I can’t tell them no. I don’t reject “small” jobs. All I need to do is just drop my big car and carry the small one to the site, so they don’t get scared and stop calling me.

In fact, I recently went to do a ₦100k job. I still go to the Ministry of Lands myself to sort out approvals and relate with the staff like I used to. The only difference now is that I’m also doing my own thing in a big way.

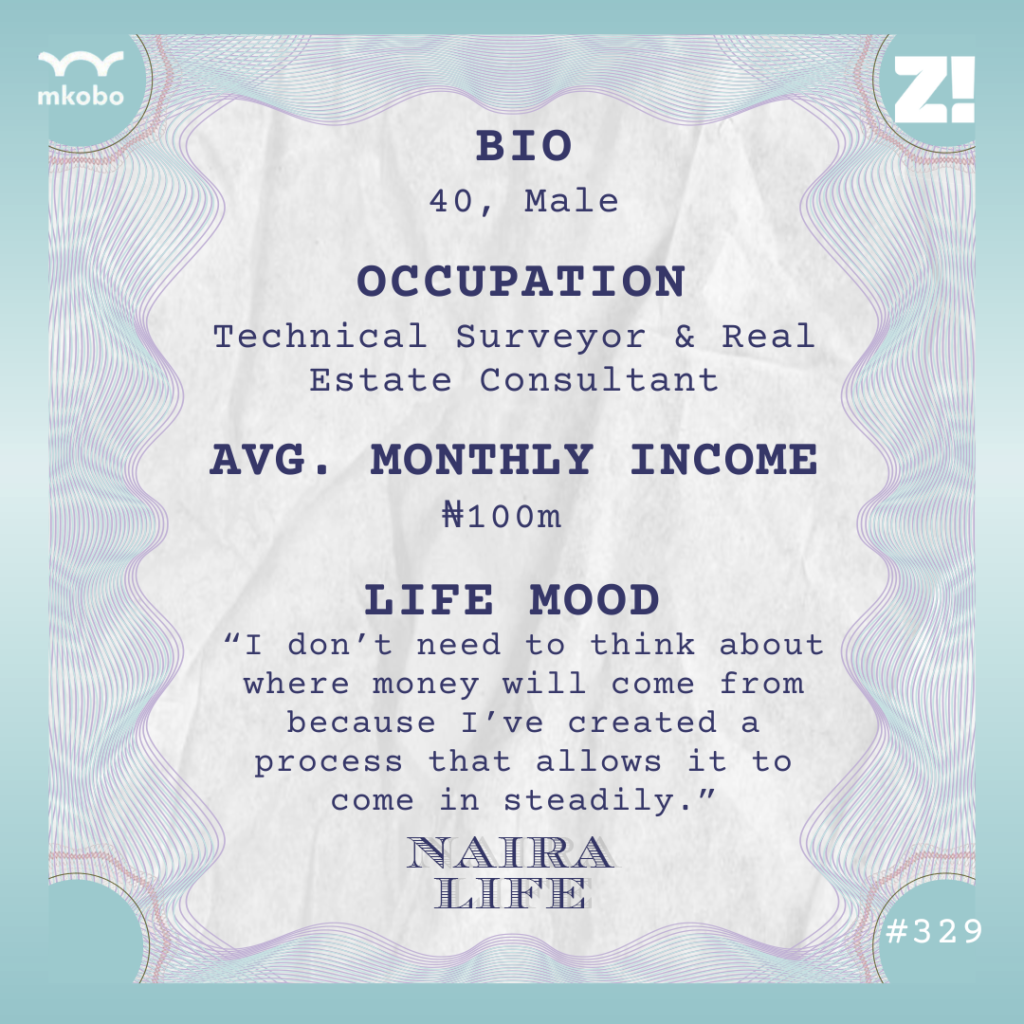

What’s your current monthly income like?

₦100m is a typical average from my surveying and real estate companies. In a good month, I can make up to ₦200m. It can also be as low as ₦10m in a bad month, especially when I’m in between projects.

It typically takes me three to four months to complete a project, and I can work on two or three estates simultaneously. I have engineers who work for me, but I like being able to get to my sites to check on progress quickly. Clients are often ready to buy my buildings as soon as they’re complete because I’ve built a reputation for using good materials. Sometimes, they buy while we’re still painting.

In addition to my businesses, I have five properties that bring me ₦15m in rent annually and a ₦70k/day shortlet.

You’ve literally gone from 0 to 100. How has your income growth impacted how you think about money?

Once you use money well, it will work for you. I think everyone must reach a point in life where their money works for them even while they sleep. That’s the level I’m currently at. I don’t need to think about where money will come from because I’ve created a process that allows it to come in steadily.

I also don’t keep money. As it enters my hand, I channel it back to the business. About two years ago, my account officer tried to get me to save ₦100m in treasury bills, but the returns didn’t make sense. I think it was supposed to be about ₦1.5m.

Why would I lock money up somewhere for small returns when I can use it to build a house and make double my investment? So, I don’t save money anywhere; everything returns to the business.

Are there risks to putting all your money into the buildings, though?

Not really. I’m a technical surveyor, so I know how to acquire good land. I know the potential problems to look out for, and I don’t go near government commitment lands.

That said, I still have problems with Omo Onile from time to time. I lost ₦15m to an Omo Onile dispute a while ago. The dispute became a police case, but I later abandoned it because it wasn’t worth it.

Why chase ₦15m when I could make more without stress? I just took it as a lesson. Before I make any purchase now, I meet the Oba and every community leader. If there’s a need for settlement, I tackle it immediately.

Out of curiosity, what kind of lifestyle does your income afford you?

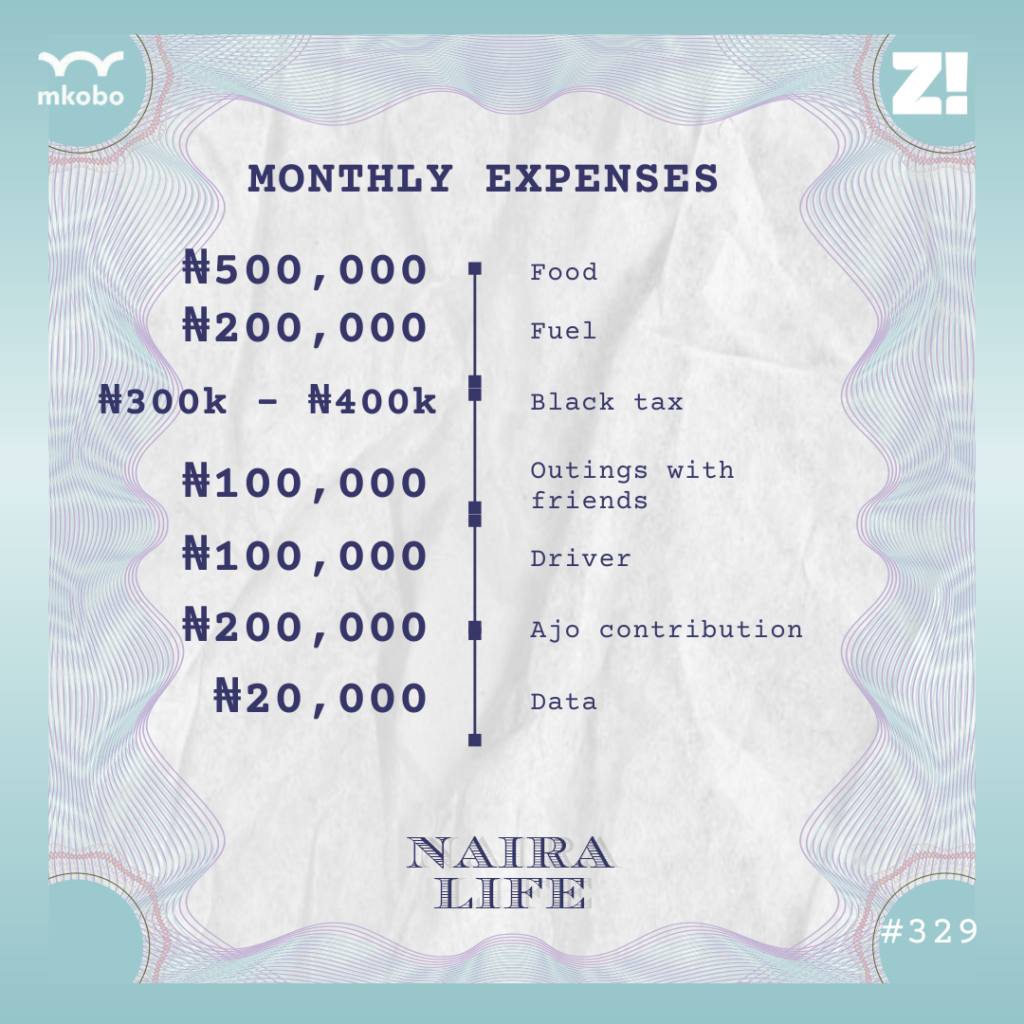

Well, I have the resources, but I live a moderate life. I still live in the same house I built years ago, and my three cars are easy to maintain. I have one driver, and my children don’t attend overly expensive schools. My typical expenses are mostly food and school fees. I don’t live extravagantly at all.

Let’s break down these expenses into a typical month

I think I comfortably live on less than ₦2m in most months:

My ajo contribution also serves as my travel budget. My share is usually ₦2m at the end of the year, then I add more money to it to travel overseas for a short break.

Is there anything you want right now but can’t afford?

Not at all. The only reason I wouldn’t be able to get it is if I don’t want it.

How about the last thing you bought that made you happy?

I did a crazy thing and bought a 2022 Jeep two months ago for ₦25m. I just thought, “All this money I’m making sef. How much am I even eating out of it?” Material things don’t necessarily make me happy; I just wanted to splurge on something, and I chose the car.

Do you typically feel that way? Like you’re not spending your money on yourself?

Of course. I don’t even eat much, so it’s not like I’m using the money to buy food. Sometimes, I feel like I’m making all this money, but I’m just there. I don’t do anything out of the ordinary.

However, I remember what it was like for my family to live in a leaky room, so I still work. Also, I take God’s word seriously, and it shapes my mindset. I know he expects me to live a greater life and achieve more, so I keep gunning for more. I set targets to hit higher financial levels because I want to improve and do more.

What are some of these levels you still want to reach?

I listened to a podcast the other day, and the real estate guy said he bought land for ₦3.4bn. I knew this person years ago, and even the land he was talking about.

This person might’ve had better funding opportunities, while I started my own small small. But I know I can attain such a level too; where I can push bigger projects, employ more people and change their lives too.

Recently, one of my workers told me about the house he just built. Another one said he was planning to build close to me. Those are the things I like; I want to directly impact other people’s success as I grow as well.

I should mention that I finally returned to school about two years ago. My colleagues kept saying it was past time to have gotten the certification part sorted, so I’m back at it.

Rooting for you. How would you rate your financial happiness on a scale of 1-10?

9.5. I learned how to use my money well, and the results speak for themselves.

If you’re interested in talking about your Naira Life story, this is a good place to start.

Subscribe to our newsletters and never miss any of the action

[ad]

Receiving or giving Valentine’s Day gifts is cute and all, but what if we told you the nature of the gift itself can determine just how serious your relationship actually is? Well, it can. Walk with us.

Flowers

This gives “We’re new in the relationship, so let’s see how it goes” vibes. Flowers can also mean there’s plenty of romance in your relationship, but unfortunately, they’re not a reliable indicator of how serious it might be.

Money bouquet

Money is always a good idea, but why are you stressing the love of your life with the task of unfolding several notes? What happened to just transferring the money or giving them stacks if a cash gift is the goal? The relationship might be serious, but they’re probably not seriously in love with you.

Investments

Your relationship is not just serious; your partner is also concerned about your future. Nothing says true love quite like discussing how to build wealth and secure your financial future. Bonus if it’s a real estate investment that appreciates over time and can be a passive income source like Gazania Park, inside Periwinkle Estate, developed by Blue Square Limited. All that’s needed to start is a 40% initial deposit; you can even pool investments with your partner or friend.

Food

This could go in two ways. Your partner either understands that you value having a full stomach before anything else, or food was the easiest gift option they could think of. Whatever the case, the seriousness of your relationship is in question. They had 364 days to give you food. Couldn’t they switch it up for Valentine’s Day?

Words of affirmation

In the immortal words of Shakespeare, “Na words of affirmation we go chop?” I mean, your partner loves you and wants you to know it, but let’s be honest. If they were serious, they’d have planned to add something tangible to the gift.

Dinner date

Your partner is willing to visit an overpriced restaurant on what’s probably the most expensive night of the year to show their love for you. That’s pretty serious.

A house

This is as serious as it gets. Your partner clearly sees you in their future and wants to create a legacy with you.

Pro tip: Push your partner in the right direction by telling them to check out Blue Square Limited. They’re a property development company in Nigeria that helps young Nigerians invest in real estate and grow income through rental yields. They even have payment plans and mortgage options, so you can start at your own pace. You should check them out.

[ad]

In 1998, this 53-year-old retiree took charge of her financial freedom with small, consistent investments. Over the years, she strategically grew her assets and positioned herself for an early, comfortable retirement.

This is how she made it work in Nigeria.

As Told To Aisha Bello

Model not affiliated with the story. Actual subject is anonymous.

I spent my entire career as an accountant in an insurance company, helping people plan for retirement. During my active years, I saw firsthand what happens when people don’t prepare early enough — the anxiety, the regrets, and the desperate attempts to stretch out insufficient pensions.

I was 26 when I received my first paycheck, and I never wanted that to be me.

Also, I didn’t grow up rich. From a young age, I understood that if I wanted financial security when I was older, I had to build it myself. So, while most people were thinking about how to spend their salary, I was thinking about my retirement plans.

That’s why, from my first paycheck, I made a non-negotiable rule: save and invest 40% of my income, no matter what.

27 years later, I retired at 53 as a director, with a portfolio worth over ₦1 billion spread across real estate, stocks, bonds, forex, and fixed deposits. Over the next 20 years, I’ll also receive a monthly pension of ₦500,000.

This didn’t happen by luck. It was the result of deliberate decisions, smart investments, and some hard lessons along the way.

Breaking down my Retirement Portfolio

Here’s what my assets look like today:

Now, let’s talk about how I built each of these.

Fixed Deposit: The early money move that made a difference (₦65M)

In 1997, I started my career as an entry-level accountant, earning ₦16,000 per month. At this point, the Nigerian minimum wage was ₦450 before President Olusegun Obasanjo passed a new wage bill to give workers ₦5,500 in 2000.

At the time, I wasn’t investing; I was just saving aggressively. But everything changed when a friend at National Bank introduced me to fixed deposits.

That small decision laid the foundation for the rest of my financial journey.

My organisation had a unique payment structure: I received a portion of my salary monthly, while the rest was paid upfront at the beginning of the year. My basic salary (₦16,000) accounted for 60% of my total income (₦26,000 per month), while the remaining 40%, which covered housing and furniture allowances, was paid in bulk annually.

In 1998, I decided to take a risk with my annual upfront salary, which was about ₦128,000.

Subsequently, I saved my annual upfronts in fixed deposits with the National Bank until the bank failed to meet the Central Bank of Nigeria’s capital requirement in 2002. The CBN took control, and three years later, the bank was acquired by Wema Bank. Afterwards, I made fixed deposits with different banks to grow my savings.

Today, I no longer use banks for fixed deposits — except for VFD Microfinance Bank, where I’m a shareholder. Instead, I invest through asset management companies like Vetiva, FSDH and Anchoria because of their higher interest rates.

Right now, I have ₦65 million in fixed deposits and earn fixed interest annually.

Real Estate: My biggest asset class (₦500M)

I’ve always believed that owning property is key to financial security in Nigeria.

In 2001, I bought my first property in Isolo, Lagos, for ₦7 million. When I sold it in 2008, its value had appreciated to ₦100 million, a 1328% increase.

In 2009, I bought a plot of land in Ajah for ₦3 million. Seven years later, I sold it for ₦45 million. The value skyrocketed because of rapid development in the area; new housing projects were being built, and the road network improved significantly, driving more people to rent homes there.

I currently own three properties in Lagos worth a combined ₦500 million and earn ₦10 million in rental income from each property annually.

FGN Bonds: My safety net (₦300M)

I prioritise security, so Federal Government of Nigeria (FGN) bonds have always been part of my plan. And as an accountant, I’ve always known about them.

FGN bonds are managed by the Debt Management Office (DMO), which allows the government to borrow money from citizens in exchange for interest payments.

Regular FGN bonds require a minimum of ₦50 million, and these predominantly long-term investments range from three to fifty years.

FGN Savings Bonds, which are short-term, offer a more accessible option. They have a minimum subscription of ₦5,000 and a two- to three-year term. Once the bond matures, the principal is returned.

With FGN Savings Bonds, I receive quarterly interest (coupon payments), while longer-term FGN bonds pay interest twice a year. At the beginning of every month, the government issues savings bonds for those who want to buy; the most recent interest rate was around 18%.

My children also have FGN Savings Bonds, and they’re already earning passive income, with quarterly interest payments deposited into their accounts. Since they don’t need the funds, I reinvest their earnings to compound their wealth over time.

To get FGN bonds, you need an agent. I have bought through GT Bank, FSDH, and Vetiva in the past, but I currently use Afrinvest. I reviewed their financials while working, so I knew it was safe to go through them.

I hold both short- and long-term FGN bonds worth ₦300 million.

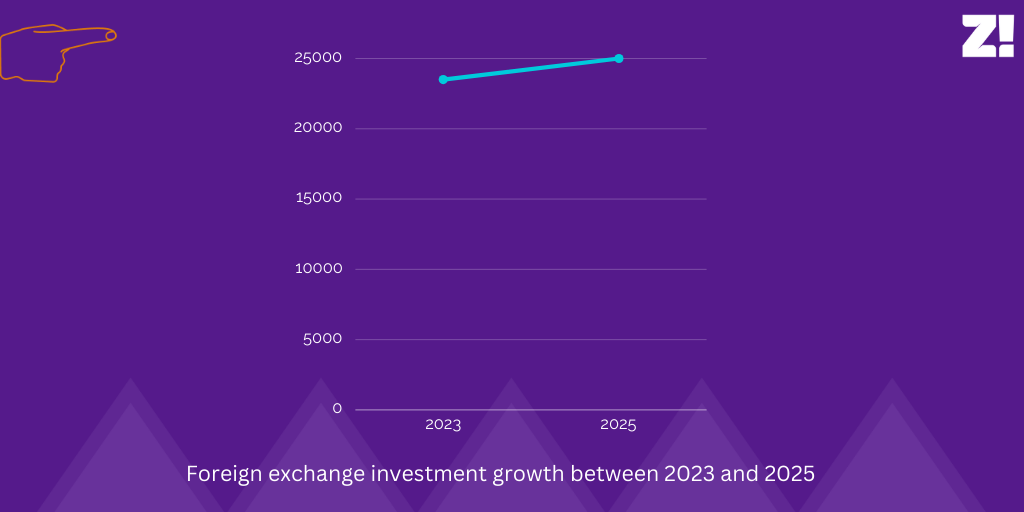

Foreign Exchange Investment: Beating inflation with hard currency ($25,000)

For foreign exchange investments, I use Zenith Bank and FSDH for fixed deposits and Vetiva for my Eurobond investments. This is different from online forex trading, where people actively buy and sell various currencies to make a profit. Forex trading is high-risk and requires active monitoring.

I focus on foreign currency investments by depositing dollars in fixed-income instruments like Eurobonds and dollar-denominated fixed deposits. This protects my money from naira devaluation while earning a stable return.

I started investing in forex two years ago when the naira started losing value. My initial investment of $23,500 has since grown by 6%.

Stocks: Slow and steady growth (₦22M)

I invested heavily in stocks until the 2008 stock market crash changed everything. The market dropped by at least 70%, and people lost their lives over the financial ruin. At the time, I had invested ₦500,000 and later bought rights issues worth ₦4 million to increase my shares. Rights issues allow existing shareholders to buy more shares when a company wants to raise capital.

The Nigerian stock market has only recently regained some stability. After the 2008 crash, I stopped actively investing in stocks, though I held the ones I already owned. I still receive annual dividends from solid companies like GTB, First Bank, Flour Mills, Nestlé, and Transcorp Hotels. At this point, I’ve already gotten my initial investment and continue to earn from them.

The only new stock I’ve bought recently is VFD Microfinance because I trust the company’s growth potential. I initially invested ₦5 million, then bought their rights issue for ₦8 million.

Today, my stock portfolio is valued at ₦22 million.

An exterior view shows the Nigerian Stock Exchange building in Lagos, Nigeria.

Pension: The passive income that gives me peace of mind (₦500K/Month)

In 2004, the federal government introduced a new pension scheme that required me to contribute 8% and my employer 10% of my salary towards retirement.

I also had the option for voluntary pension contributions, which I locked into because it meant more pension income. Before this, we had a fixed system where every employee had to pay ₦4 monthly, while the employer added ₦10. That didn’t do anything, but the new scheme meant my pension was directly proportional to what I earned in service.

When it comes to pensions in Nigeria, you can either choose Programmed Withdrawal (PW) or Annuity. With Programmed Withdrawal, you receive a set amount of money for a set period, say 10 or 20 years, after which the payments stop.

An annuity, on the other hand, is paid for life. When you opt for an annuity, your money is transferred to a life insurance company that administers income until you die. This type of pension is for life but can be transferable to living family members based on the specific terms of the contract.

I opted for Programmed Withdrawal because, as an accountant, I prefer to have control over my finances. With an annuity, I’d need to transfer my entire balance to an insurance company and receive fixed payments for life. I don’t need any company to manage my money; I have the experience. With Programmed Withdrawal, my funds remain invested, and I can still benefit from returns.

I now receive a monthly pension of ₦500,000 and will continue to receive that for the next twenty years.

In addition, I bought a personal pension plan from the insurance company where I worked. A year before retiring, I stopped the plan, took my money, and invested it in other assets.

Investment Diversification: Not all eggs in one basket

If a project requires funding, I liquidate some of my investments to finance it. Then, when I have more funds available, I’ll reinvest.

But the rules are different with government bonds. If I invest in a two- or three-year bond, I wait until maturity to access my funds. Although I can sell the bond, it’s not a liquid asset, and I won’t get my money back immediately.

In contrast, fixed deposits with banks are more flexible. If I invest in a one-month fixed deposit, I can withdraw my funds at the end of the month or even before that if needed.

I’ve had real estate projects that required funding, so I terminated some investments to finance them. Then, when I generated returns, I reinvested what I took out.

I believe in diversifying my investments, so I don’t put all my eggs in one basket. I mix fixed deposits, government savings bonds, real estate, and shares. I’m also into foreign exchange investments. If I decide to run a business now and invest some funds, that’s diversification.

This way, I can rely on others for support if anything happens in one sector.

My Two Cents on Investing For The Future

Economic challenges are constant – inflation, downturns, market volatility, and instability have always existed and won’t stop. Regardless of any economic downturn, you must plan and invest towards your retirement to ensure a secure financial future. My two cents:

Start early, no matter how small.

The best time to start investing is with your first paycheck.

Prioritise investments over saving. Think of savings as money you can access anytime, but it doesn’t grow much. And investments as money locked for a period, earning higher interest.

When you save, your money sits in the bank, earning minimal interest, but when you invest, you put your money to work.

Don’t worry if the interest seems small at first; consistency is key.

Increase your investments as your income grows.

Aim to save at least 30% of your salary.

If 30% is too much, start lower and increase it gradually.

Don’t be greedy about earning high interest rates. Explore low-risk investments, start investing early, be consistent, and aim to invest at least 30% of your income.

Editor’s note: This subject chose to keep her legal name and information confidential for privacy reasons, and Zikoko has verified her assets and earnings via income statements and necessary documentation.

In 2024, this entrepreneur experimented with naira and dollar investments and grew her net worth by 29% across three different investment instruments. This is how she did it.

As told to Boluwatife

Model not affiliated with the story. Actual subject is anonymous.

In 2024, I decided to take financial literacy and investments seriously. Until then, I’d stuck with saving; it was straightforward at a time I felt investment instruments like mutual funds and treasury bills were complicated. I didn’t want to lose my money.

But the naira’s downward spiral since mid-2023 and its negative effect on my import-heavy ready-to-wear clothing business changed my attitude toward saving money.

I started saving in dollars. It was a more stable currency, and my business was at least 60% dollar-denominated, so it made perfect sense.

For my dollar savings to work, I needed a fintech product where I could convert my naira easily. So, I picked Risevest. The app automatically converts my money to dollars when I send naira to my savings wallet. Plus, there’s some interest paid on the savings at the end of every month. Win-win.

Using the app made me curious about investments again. They offered different investment instruments, and I started learning about risk appetites and investment options.

But first, research. I turned to YouTube videos and disturbed two friends who work in finance when I came across concepts I didn’t understand.

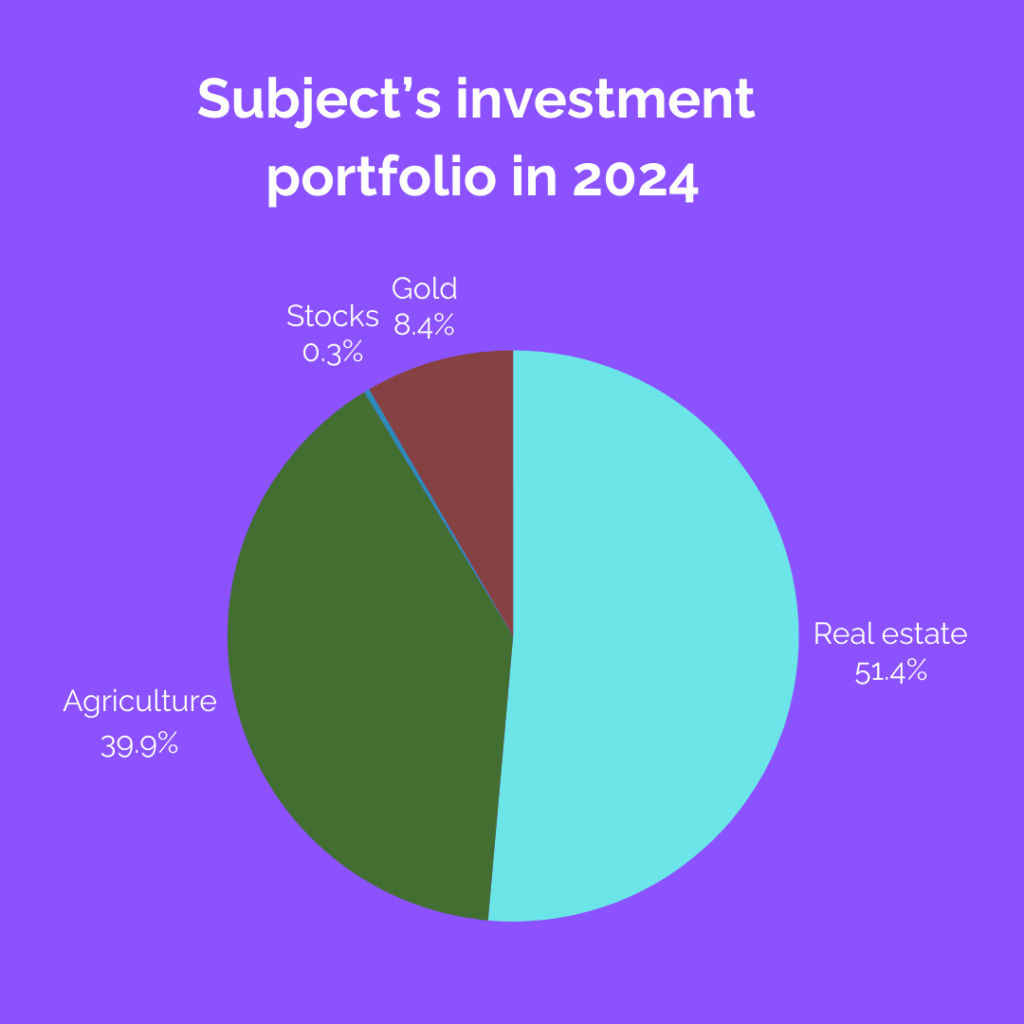

Ultimately, I decided I wanted to put my money into investments, starting with four options. This is how they did:

US Real Estate

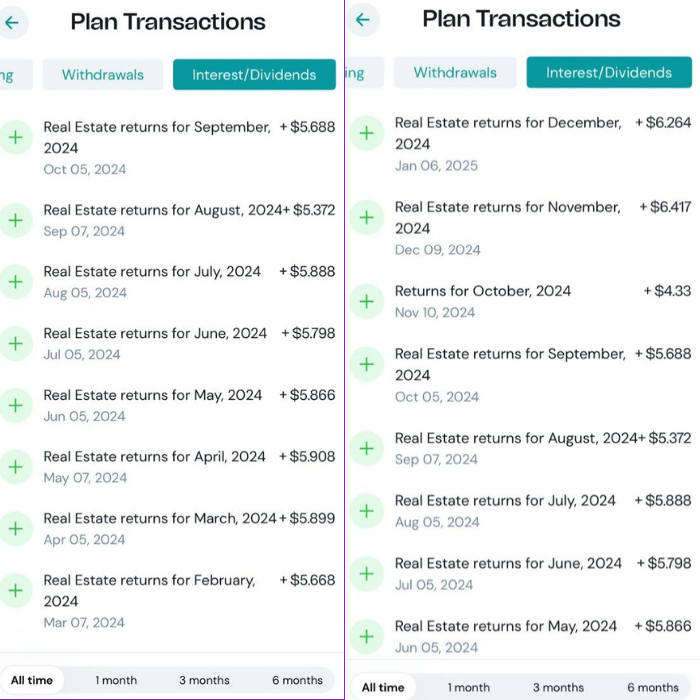

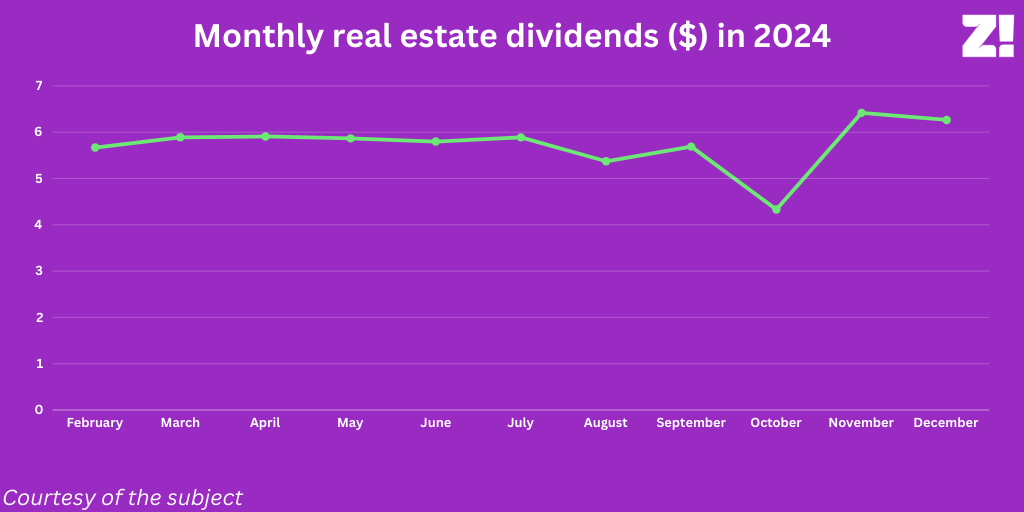

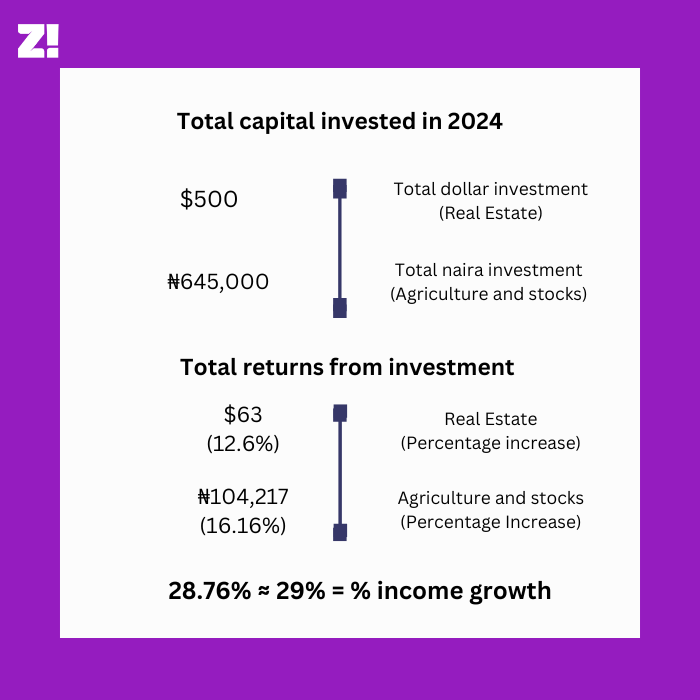

On the 9th of February 2024, I put my $500 savings into a year-long real estate plan on my fintech app.

The real estate plan is a medium-risk plan that uses the invested capital to purchase rental properties in the US. The returns come in monthly, but the amounts aren’t set in stone as they depend on the housing market’s performance.

At the end of the first month, I got almost $6 in returns. It continued every month with varying returns, and I remember thinking, “What? This is great!” It felt like free money.

Also, I saw the returns coming in, but I couldn’t touch the money until my investment matured at the end of the year. It worked for me because I wanted to teach myself discipline.

In total, I made about $63 in dividends in 2024 — 12.6% of my invested capital — and I expect more when my plan matures in February 2025. I intend to put more money into the real estate plan and re-invest this year. I’ll possibly keep re-investing for a while; I don’t need the money now, so I’d rather it keep growing.

Agriculture

I’m from Maiduguri, and it’s common to negotiate with corn farmers during planting season — you buy bags of corn from them in anticipation of harvest, store the bags until the demand for corn increases, then sell them for a profit.

I tried this investment for the first time in 2022. I gave my mum ₦200k to buy five bags of corn at ₦40k each, and when she returned my money four months later, I’d made ₦20k profit on each bag, bringing my total returns to ₦100k. It was a sweet 50% profit, and I knew I’d try the investment option again.

So, in 2024, I invested ₦640k in corn cultivation. I bought eight bags at ₦80k each but made ₦12k on each bag four months later.

I didn’t make as much profit this time due to the terrible Nigerian economy and decreased demand for corn. Insecurity was another problem: you could purchase bags from a farmer to discover that bandits had raided his farm, and he lost everything. Storage issues and pests also affected the produce quality.

So, my agricultural investment wasn’t as profitable as I expected. I made only 15% profit on my invested capital. 15% is great; I just hate that the Nigerian economy might be ruining this income opportunity. I plan to try corn farming again and diversify to cocoa and cassava in 2025.

Nigerian Stocks

In September 2024, I heard about Bamboo and downloaded it to see what they were doing there.

An investment banker friend I reached out to explained that investing in stocks requires a lot of informed intuition. Stocks are high-risk investments, and prospective investors need to listen to news about the company they want to invest in. This helps them understand when the company is likely to increase or decrease in value.

I funded my account with ₦5k — an amount I knew I could “gamble with” and bought a few units of MECURE stocks. I was lucky and my stocks tripled in value three months later, and I sold my position at ₦13,217 — a 164% growth. I didn’t want to risk leaving the stocks and potentially losing my initial capital.

The money is still in my Bamboo wallet, and I’ll probably use it for some investment experiments this year. If I lose my money, fine. I can just add a bit more over time and use it to properly understand how stocks work. Who knows? I could also become more comfortable taking risks.

Physical Assets

Another thing I tried in 2024 was investing in gold. I haven’t made any money from it, but in September, I bought a gram of 24-carat gold at ₦135k. Today, a gram costs ₦165k. I don’t plan to resell soon; I just think of gold as a valuable asset in an emergency. I can sell gold at any time. I’ll possibly sell gold before converting my dollars to naira.

Bonus: Dollar Savings

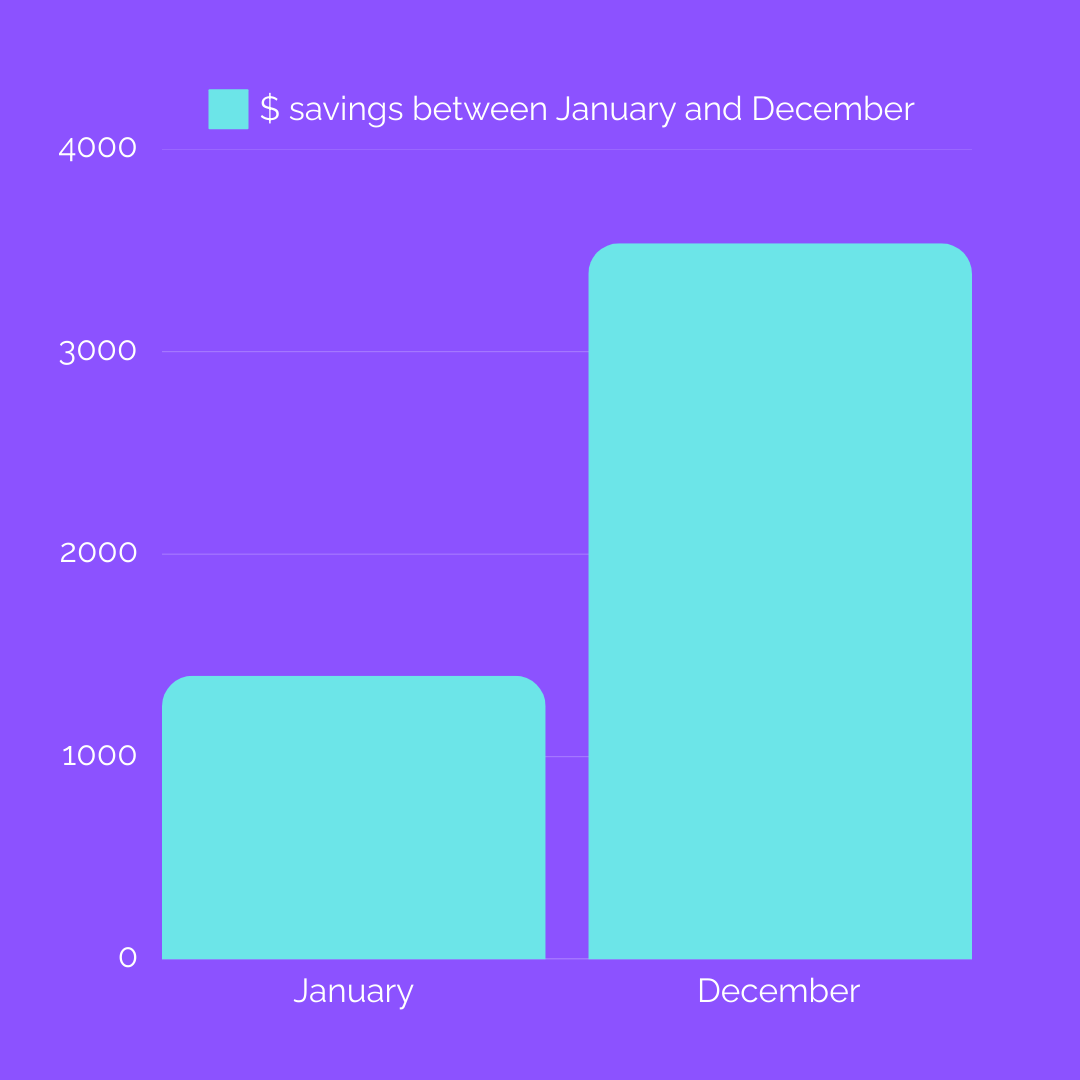

In 2024, I also decided to build up my savings portfolio specifically for investments. Every month, I saved at least 25% of my income plus any extra money I got in my dollar savings wallet. This ensured I had capital for the little investments I did.

This approach also helped me increase my savings by about 60%. In January 2024, I had $1400+ saved. By December, this had grown to $3,535 — minus the capital locked in real estate.

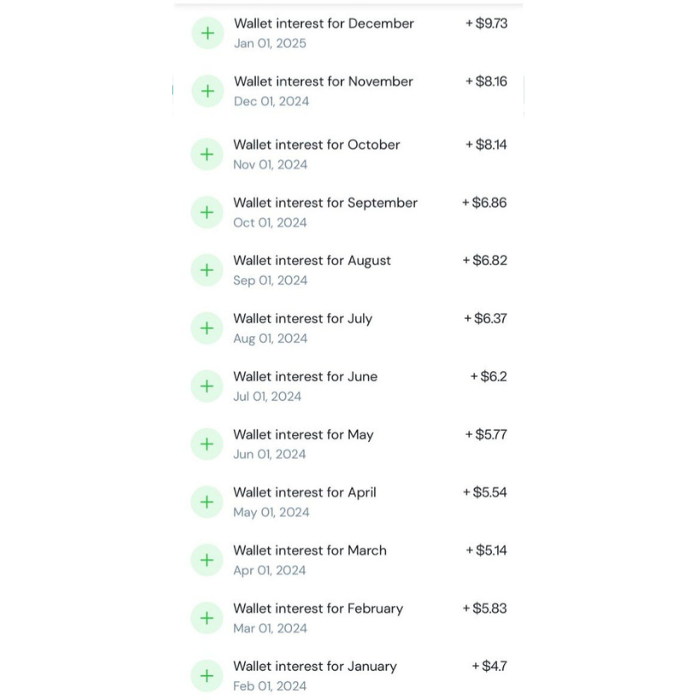

Additionally, the app pays up to 8% annual interest (paid monthly) on wallet savings. The total interest payments came to $79.26 by December 2024.

My investment outlook for 2025

Investing was the best financial decision I made in 2024. Seeing how much I made from the different instruments drove me back to the investment books in November. I liked the idea of extra money and wanted to know more.

I researched more about channels I previously didn’t understand, like treasury bills and mutual funds. I also got advice from my friends, and I’m really proud of how much I know now.

In 2025, I plan to diversify my investment portfolio and grow my wealth as much as possible. In January, I put ₦500k in treasury bills and ₦1.5m in the money market using an investment banking firm called Cordros Capital.

The returns on both investments are fixed at 20% and 25% per annum, respectively. I like that the rate is fixed and not subject to market speculation at all. So, I know that I can look forward to ₦475k returns from both at the end of the year.

If I have extra money, I might dabble in US and Nigerian stocks in the middle of the year. Of course, I’ll reinvest in real estate and agriculture and see how it goes. I’ve also thought about cryptocurrency, but I now accept that I’ll probably never understand it. So, I won’t be investing in crypto.

If you ask me to break my key investment learnings in the past year into action points, they’ll look like this:

My cardinal rule for investing is to only put my money into things I understand and can explain to anyone else. It’s what I’d advise anyone too.

Also, knowledge is essential in an investment journey. I took advantage of online resources, friends and communities like Money Africa. I also asked questions at every step of the way, and I’m glad I did. These days, almost all one needs to do is tag investment gurus on social media timelines to get answers. You can also ask questions on Reddit or NairaLand.

Find something simple you can understand and consistently set a small amount aside to build a savings and investment culture. There’s a culture of shame around savings and investments, especially when we come online and see how much others have saved up.

I’m comfortable with my little nest egg, and you should be too.

Editor’s note: This is not financial advice. Please do all due diligence before investing in any of the channels mentioned in this article.

Every week, Zikoko seeks to understand how people move the Naira in and out of their lives. Some stories will be struggle-ish, others will be bougie. All the time, it’ll be revealing.

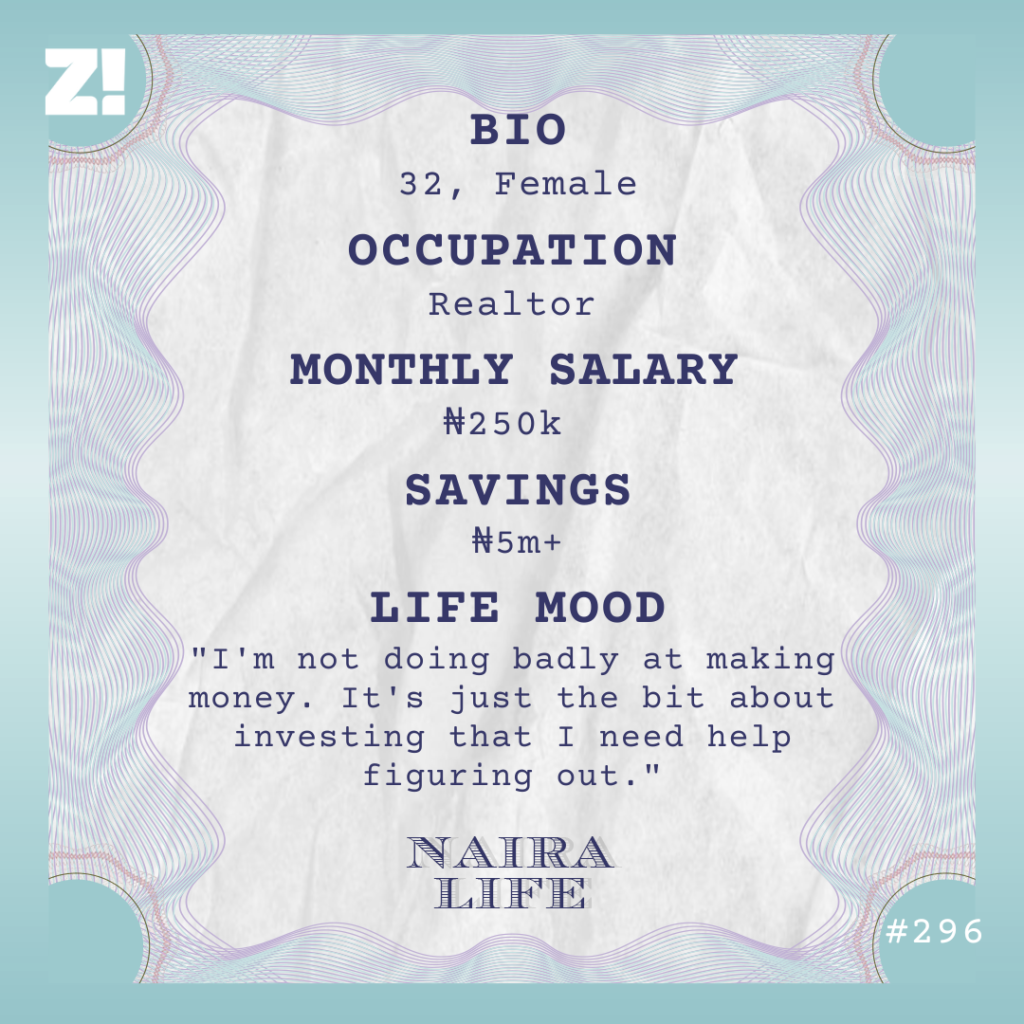

Let’s talk about your earliest memory of money

At 14, I got my first job at a movie rental, earning ₦500/week. It wasn’t an actual job, to be honest. I was in SS 3, preparing for my JAMB exams, and usually finished early from school.

My mum decided it was best I waited in the rental shop until she returned home from work. I started helping the shop owner attend to customers, and she paid me for my help. The pay wasn’t regular, and I spent it on suya whenever it came. I also bought airtime for my mum a few times.

What was the financial situation at home like?

We were comfortable. My sperm-donor father decided he didn’t want the responsibility and left when I was about a year old, so it was just me and my mum for a long time. My mum worked at a multinational, and she drove me to school every day before she went to work. We also lived in an estate, so yeah, I’d say we were pretty comfortable.

My mum remarried shortly after I entered the university in 2007. I remember a friend asking why I wasn’t angry that my mum was “replacing” my father. How do you replace someone who was never there?

Plus, my bonus dad is a good man. He has been in the picture since I was in secondary school as my mum’s “friend”. They came clean about their relationship after I entered uni. I think that was their way of making sure I was grown enough to adjust. I honestly didn’t mind. It also didn’t hurt that my bonus dad started spoiling me with money.

Define spoiled

He started giving me a ₦25k monthly allowance even though he knew my mum already sent ₦10k/month. He worked in transportation and started doing cute things like bringing me clothes and fashion accessories whenever he returned from his regular travels.

My bonus dad even told me to always call him first for whatever I needed. I used to joke that he didn’t need to buy my love because I already accepted him.

That’s so sweet. Aside from the allowance, did you have any other income source in uni?

I had a stint selling earrings in the 200 level. I actually started the business by accident. I was wearing one of the earrings my dad bought me when a coursemate said she liked it.

I showed her the other pieces; she picked one and paid me ₦1k. The next day, someone else expressed interest in my earrings. That’s when it clicked that I could sell them. So, I told my dad to buy me a few more pieces, and I started selling.

I’m not sure how much profit I made since my dad refused to let me pay, but I sold each piece for between ₦1k and ₦1500. I did that for two months and stopped when I had to leave the university.

Why did you leave?

I started hearing talk about how the uni wasn’t accredited. It was a fairly new private university that had about three sets of graduated students. Those students kept complaining that they were stuck and couldn’t go for NYSC because of the accreditation issue.

My parents thought it was too risky for me to stay, hoping the issue would be resolved before I graduated, so I left in 2009. By the time I left, I’d secured another admission to a college of health to study community health extension work, so I just changed schools.

What do community health extension workers do in Nigeria?

So, they also call them “CHEW”. They’re the health workers you see wearing ash-colour uniforms in primary health centres. CHEWs typically work in semi-rural communities with limited access to health care.

I was studying nursing at the uni I left, and when I had to leave, a friend of my mum recommended the CHEW course. I felt like both courses were one and the same, so I didn’t object. I was happy as long as I went to school like my friends.

It doesn’t sound like you were thrilled about the course

I didn’t know what I wanted to do, actually. I didn’t even choose nursing. My mum wanted me to study medicine, but a lecturer at the university suggested nursing to increase my chances of getting admission since medicine was competitive. It’s not like anyone forced the course on me. I didn’t have strong opinions about any other course, so I just agreed.

I did end up liking CHEW. However, I didn’t have time to consider business opportunities because the course required me to go on unpaid work experience placements in health centres. But my parents still gave me the ₦35k monthly allowance, so I was never broke.

I assume that means ₦35k was enough to give you a good life

It was. I lived alone in an apartment that my parents paid for, and I didn’t like cooking, so I constantly bought food. ₦35k was enough to feed me for a whole month, take me to and fro school and still have a little extra to buy perfumes and look good.

However, the allowance stopped after I finished school in 2012, and I suddenly knew what broke meant. I mean, I lived with my parents, and they fed me. But a young woman needs to have money in her account, you know?

Right. So, what did you do?

I started job-hunting. I found one at a private hospital, but at ₦30k/month, the salary was ridiculous. To make matters worse, I was practically working as both a CHEW and nurse. I worked nights, assisted in surgery and lab work, and attended to patients. It was exhausting.

I worked at the hospital for about two years and survived only by taking additional locum (or temporary) gigs here and there. The gigs were shift-based, so I took them when I was off duty at my hospital job. I usually did at least one locum gig monthly during those two years, which usually brought an extra ₦20k – ₦30k.

There were also random money tips from patients — nothing big, but substantial enough that I hardly touched my salary for transport costs. I still lived at home, so I only spent money on transport, food at work and the occasional snack for my siblings.

I’m not sure if I can accurately say I was balling on that salary because I didn’t even have time to ball. But I became a super saver. In some months, I saved as much as ₦30k. Work was stressful, but at least I was getting the hang of my finances.

Why did you only work at the hospital for two years, though?

I was pursuing government work for job security and better pay. My mum’s friend found me a plug who claimed he had the right connections to get me the job. So, I quit the hospital on impulse, thinking the government job was sure. I think the matron annoyed me that day, and I was just like, “To hell with your job madam.”

Two weeks after quitting, my “sure plug” disappointed me. This was in 2015.

Yikes. So you were effectively jobless

I had about ₦400k in my savings, but I knew the money wouldn’t last if I didn’t get another job. I’d also hoped the government job would give me an excuse to leave home and rent an apartment.

I was in a relationship with my boyfriend (now husband), and it was difficult to do relationship things while still living with my parents. If I wasn’t at work, I had to explain why I was going out and I didn’t like it. But since the job didn’t come through, I just had to double my hustle.

Locum jobs came to the rescue again, and I did that for a while. I still found full-time opportunities at hospitals, but I didn’t think they were worth it. All the jobs I saw offered between ₦40k and ₦60k, and it didn’t make sense to me. I preferred to do only a few shifts a month and get ₦20k than stress myself working full-time. I managed till 2016 when I decided to pursue a career selling real estate.

How did real estate enter the picture?

My boyfriend was a video editor who often worked with a real estate company. He was always talking about how there was money in the industry. He told me all about how the company paid affiliate marketers 10% of whatever they helped to sell and tried to encourage me to try it as a side hustle.

At first, I didn’t consider it because I didn’t see myself as the person who had the courage to convince people to buy things, not to talk of expensive real estate.

But by 2016, I was already tired of my work as a CHEW. Career and income growth opportunities were limited, except I worked in the government or returned to school to upgrade to nursing or public health.

So, I decided to give the real estate thing a try.

How did it go?

The company gave me access to pictures and videos of the landed property and buildings available on sale. I could also visit the sites to take pictures by myself. Once I got a client, I’d direct them to pay, and the company would give me my cut.

It seemed straightforward enough, but the hard part was selling. I designed my WhatsApp status and Facebook page with different pictures and videos of properties, but nobody came to buy.

I didn’t make any sales in the first eight months. By then, I’d pretty much stopped taking locum jobs because I was always going from one site to another. My mum didn’t understand why I left a reputable job to sell houses, but my dad was supportive and always helped me with transport fare.

Tell me about that first sale

It was a ₦3m plot of land. The buyer came from Facebook, and I remember being wary that someone I didn’t know was willing to trust me with millions.

I should note that I’d grown from only posting pictures of properties. To build credibility, I’d also started posting short articles about real estate: pieces about documents to look out for when buying land, regulatory bodies for buildings, etc. I thought it made me seem more professional and knowledgeable about what I was selling.

Anyway, the man bought the land, and I got my ₦300k commission. I was so excited. It’d taken me about a year to save ₦300k, and I made it just like that. It fueled my resolve. I was like, “This real estate? We’ll make this money there.”

Energy!

I worked for that company for about two years and earned an average of ₦700k/year.

One thing about real estate is that it’s a lot easier to sell after you’ve made your first few sales. This is because the people you sell to likely have friends in the same income bracket, and they can easily refer those friends to a trusted person (which is you).

In 2019, the company offered me a role as a real estate consultant. My job basically involved handling social media marketing, planning property showings, and offering investment advice. I took the role because it came with a sure ₦150k salary, and I’d still get my 10% commission for every sale I facilitated.

I made good money in 2019. I was still saving most of my income but began keeping half of my savings in dollars on a Fintech app. A friend in finance suggested that because I was just piling money up and didn’t know what to do with it. At least, with dollars, my money wouldn’t reduce in value.

By the end of 2019, I had close to $3k and another ₦2m in my savings. Then I got married.

Did marriage come with some financial responsibility?

Yes. I think marriage was my first introduction to adulthood. Before the wedding, my husband and I agreed he’d handle the big bills like rent and utility bills while I’d assist with feeding. I feel like I played myself because feeding isn’t a small bill at all.

While I lived with my parents, I didn’t have any business with the food bill. I dropped the random ₦10k to support, but I didn’t know just how much food cost.

Imagine my shock after I got married and realised I was spending ₦20k weekly to cook for only two people.

Then, the pandemic happened, and my husband couldn’t get as many videography gigs because there were no events. I had to take on more bills at home. Property sales also reduced, and my bosses slashed my salary to ₦75k for about six months since nothing was coming in. We had to rely on my savings for almost all of 2020.

Thankfully, things picked back up in 2021, and we’ve mostly gone back to my husband handling the major bills.

What’s your monthly income like these days?

I still work with the real estate company on ₦250k/month, but most of my income comes from my commissions and realtor dealings on the side.

I started my own mini realtor business in 2022 to have direct access to sellers and not have to share commissions with real estate companies. I can negotiate 15% – 20% with the original seller as my commission.

Of course, sales don’t happen monthly, and it can take several months to make a huge sale. It has even gotten worse between 2023 and now. Before, I could be sure of at least ₦3m – ₦5m/year, but I’ve not made ₦1m this year.

Why do you think that is?

The economy. People aren’t buying as much these days. You’ll see one generic duplex and hear that the price is ₦150m. It’s usually people with dodgy income sources who can afford those types of houses, and they also expect you to shake body.

What does “shake body” mean in this context?

Sexual demands. This doesn’t happen all the time, but in this line of work, I’ve seen men who see a woman selling real estate and expect she’s ready to do anything to convince you to buy. I don’t know if some people do it, but I’m not chasing commissions that seriously.

I guess it’s just one of the job hazards. The economy is my major concern, and it doesn’t look like things will get better. I’m still sticking around to make enough money to build an investment portfolio and safety nets for whenever I have children.

What kind of investment options are you considering?

That’s been one of my major financial headaches, actually. It’s easy for me to pile up money, but I get scared of the prospect of investing my money somewhere and losing it.

I still save in dollars, but I’m looking for options that will actually grow my money. I have $1k in Bamboo stocks and ₦1m in mutual funds, but I want to overcome my fear and diversify my portfolio. My savings—both in naira and dollars—are about ₦4m currently.

I notice you didn’t mention real estate investments

I can’t say this outside, but I don’t really believe in investing in real estate. It’s wild because that’s literally what I sell, but I don’t think I want to go that route, especially in Lagos. It’s not worth it.

Please tell me more

It’s just really problematic. If you decide to buy land, you have to accept the possibility of the government or one random person contending with you for it. You can choose to buy in an estate, but those are often overpriced with plenty of hidden charges. To get a decently priced piece of land in Lagos, you have to enter the bush.

If you decide to just leave the land and buy a house outright, that also comes with some risk. I’ve worked with these guys; some just build with substandard materials. Plus, I don’t like how new buildings all have tiny windows and high roofs. I prefer to build based on my specifications. But that also comes with the challenge of the ridiculously high cost of building materials.

Even if I close my eyes now and buy land, who knows how much cement and paint will cost when I’m ready to build? Let me not say never sha. If I see free money, I can buy land in my village. But this Lagos? I don’t want to.

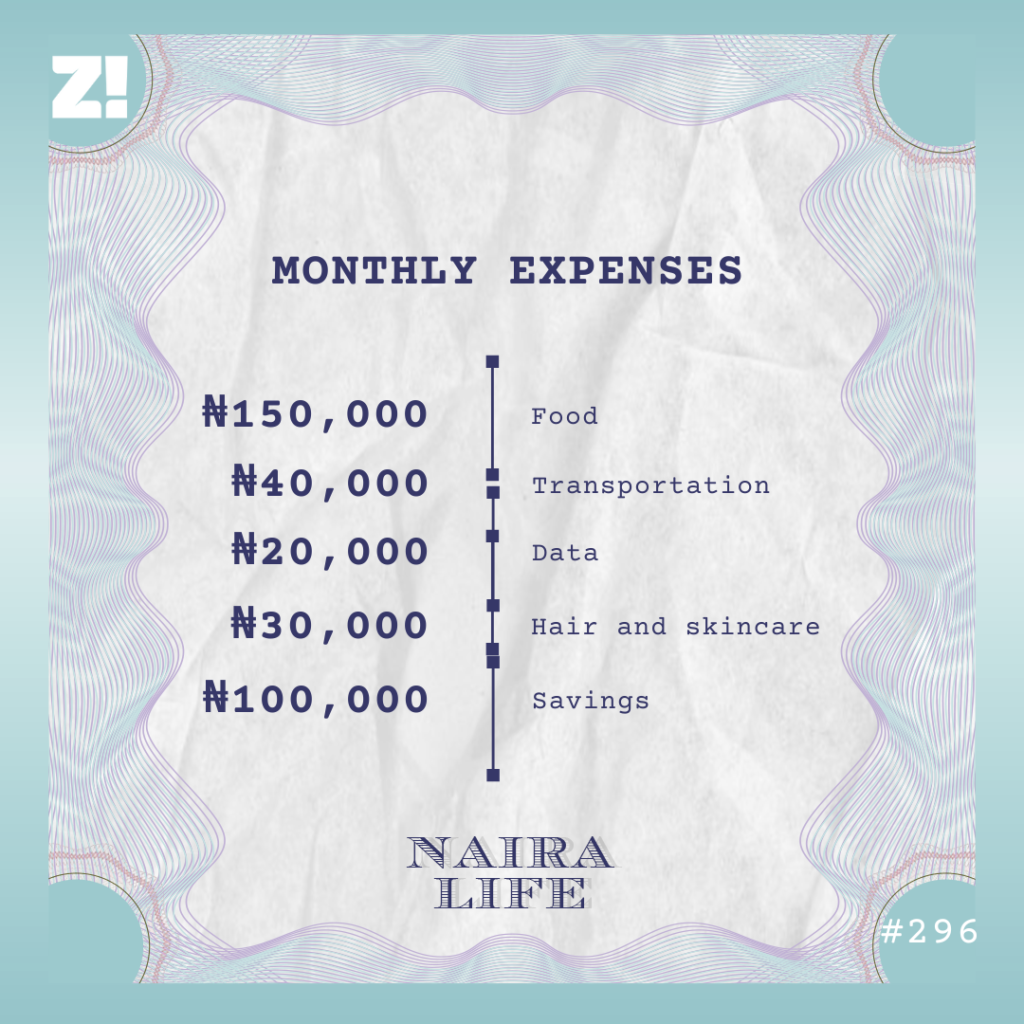

Fair. Let’s break down your typical monthly expenses

I complained to my husband early this year about the rising cost of food, so he now gives me a ₦100k monthly allowance to support the food bill. It goes like this:

How would you describe your relationship with money?

I think I’m still figuring things out. I hope to soon get to a point where I’m not just gathering money because I like seeing a heavy balance in my account but that my money is actually working for me. If I can hack investments and start earning passive income, I’ll be able to take a step back from real estate.

What would you be doing if you took a break from real estate?

Maybe I’ll try my hand at being a stay-at-home wife. Who am I kidding? I’ll probably die of boredom and return to selling land within a week.

Haha. What’s one thing you want but can’t afford?

A car. We have a 2007 Toyota Corolla, but my husband often uses it for his events, and I end up taking cabs to property showings. We can’t afford to maintain two cars right now — I’m even scared of checking how much a Tokunbo car costs now — but it will definitely make my life easier.

How would you rate your financial happiness on a scale of 1-10?

7. I’m not doing badly at making money. It’s just the bit about investing that I need help figuring out.

If you’re interested in talking about your Naira Life story, this is a good place to start.

There’s a chance you know that there are mortgage banks in Nigeria, but you don’t think much about them. Let’s start with the basics: owning a home is generally a high-cost endeavour, but Nigerians historically prefer building their homes or buying outright. The kicker here is that both require deep pockets, and only a few who have this financial power can take on these projects.

Enter mortgage banks.

Mortgage banks exist to fill this financial gap, allowing low—to mid-income earners to own real estate that is ordinarily out of their financial reach. They could be particularly useful in Nigeria, where a housing deficit of 28 million units requires up to ₦21 trillion to fill.

In addition, mortgage banks in Nigeria serve as an alternative to home loans from commercial banks, where interest rates could be as high as 25% and payback periods much shorter. That said, mortgage loans are somewhat unattractive to end users because of the same interest rates, but other factors, including strict lending criteria, significant down payment requirements, and access to credit, affect the adoption of mortgage banks in Nigeria.

That said, there are about 32 primary mortgage banks in Nigeria, proving one thing: borrowers have multiple mortgage opportunities. The first critical step to considering a mortgage loan is to understand the scope of banks that give mortgage loans to borrowers.

So, what are the functions of mortgage banks?

Functions of mortgage banks in Nigeria

Mortgage origination

Mortgage banks in Nigeria give loans to people or businesses buying property. Part of this process is handling the paperwork, assessing credit, and ensuring compliance with regulations.

Simply put, their job is to connect borrowers with the credit they need to own a home, but they must verify critical details like income and credit history along the way.

Loan Underwriting

Mortgage banks want to ensure you’re safe from financial ruin. So, they look into your credit score, job stability, income, and the value of the property to see if you can handle the loan.

Talented underwriters ensure that only financially stable applicants get approved, reducing the risk of defaults.

Loan Servicing

Loan servicing is how mortgage banks manage your mortgage from start to finish. They collect payments, handle escrow for taxes and insurance, and address any questions you have. For banks that give mortgage loans in Nigeria, good loan servicing keeps everything running smoothly and ensures borrowers get the support they need.

Risk Management

It’s the mortgage bank’s job to protect itself from financial losses. They assess credit risk by checking borrowers’ ability to repay, manage interest rate risk by guarding against rate changes, and monitor market risks like shifts in property values or economic conditions. All these efforts ensure safe lending and investment.

Home Purchase Loans

Home purchase loans are a core service and functions mortgage banks in Nigeria serve to help people buy homes. These loans come with different terms and rates, giving borrowers options that fit their needs.

Home Improvement Loans

Home improvement loans from mortgage banks help homeowners fund renovations or upgrade their properties. These loans provide the cash needed to boost home value or enhance living conditions, from kitchen makeovers to roof repairs. Banks often release the funds in stages as the work progresses and may ask for proof of the planned improvements.

Equity Release Programs

Equity release programs from mortgage banks in Nigeria let homeowners access the value of their property without selling or moving. Whether through home equity loans or lines of credit, homeowners can unlock funds for debt consolidation or retirement planning while still living in and owning their homes.

Top 5 Mortgage Banks in Nigeria

Now that you have an idea of some of mortgage banks’ core functions with respect to risk assessment and home financing, let’s take a step further and look at a list of mortgage banks in Nigeria that effectively do this.

As we started earlier, there are about 32 primary mortgage banks in Nigeria, but a few rank higher for several factors, including their size, loan requirements, processes and operations, etc.

1. Infinity Trust Mortgage Bank

Equity contribution (Think of this as a downpayment. The amount of money you, as a borrower, need to pay upfront when getting the loan): 20% of property value.

Repayment period: Up to 20 years.

Since starting operations in 2002, Infinity Trust Mortgage Bank has become a market leader in the Nigerian mortgage industry and a publicly traded company. Under its mortgage loan scheme, the bank loans borrowers up to ₦100,000,000 to finance their homes and has provided this service to more than 10,000 Nigerian families.

In addition, the bank has a separate National Housing Funds Scheme designed for low—and mid-income earners (such as civil servants) who cannot afford the commercial housing loan product. For this category, they offer benefits including a 0 – 10% equity contribution, loans of up to ₦10 – ₦15 million, and a repayment period of up to 30 years.

Founded in 1991 as Abbey Building Society PLC, the bank’s primary job was to connect potential homeowners with affordable housing solutions. Three decades later, Abbey Mortgage Bank is one of the largest and most profitable mortgage banks in Nigeria. It is also one of seven national Primary Mortgage Banks licensed by the Central Bank of Nigeria and the Federal Mortgage Bank of Nigeria (FMBN).

The bank’s mortgage product is available to Nigerian residents. Find out more about their services here.

3. FirstTrust Mortgage Bank

Equity Contribution: 20% for salary earners and 30% for the self-employed.

Repayment period: Up to 15 years.

One thing you need to know about FirstTrust mortgage bank is that its capital base and assets are over ₦36 billion, putting it in a prime position to be one of the strongest mortgage lenders in Nigeria.

Equity Contribution: 20% – 30% for properties in liaison with the bank.

40-50% for properties not in liaison with the bank.

Repayment period: Up to 25 years (depending on the product).

Since 1992, Platinum Mortgage Bank has been providing loans to hopeful homeowners in Nigeria. The bank’s suites of products is built for individual needs—one is designed for borrowers who are looking to buy properties from the open real estate market, and another is for people who want properties marketed by the bank.

You should check out more about their products and services here.

5. Federal Mortgage Bank of Nigeria

This is the only government-backed on this list of banks that give mortgage loans in Nigeria. Since 1956, the bank has had the same the same objective as other mortgage banks in Nigeria: Making mortgages more accessible. Perhaps it is one of few banks with robust and specific mortgage servicing options. They include:

National Housing Fund.

Estate Development Loan.

Home Renovation Loan.

Rent-to-Own Scheme.

Construction Loan

Diaspora NHF Mortgage Loan.

Each product has specific benefits and requirements, so you should check them out before making a decision. This is an excellent place to start.

[ad] [ad]

This is debatable, but the most dangerous venture, apart from dodging a Nigerian mother’s slap, is investing in land — especially in Lagos. If it’s not the fear of getting scammed, it’s navigating “omo onile” and hoping you aren’t buying land in an area that’ll be demolished by the government in the future for one reason or another.

However, land remains a valuable long-term investment option, and you can invest safely by following these tips I got from discussing with Grace Ogunlaja, the lead consultant at I-Brow Properties.

Check for the type of land

Not all land in Lagos is for residential purposes. Some have been earmarked for agricultural, commercial, or even mixed use. Buying a residential land and using it to produce pure water may earn you visits from the authorities, and you’ll probably lose ownership. Some lands can even be in locations under territorial dispute. You can verify the type of land at the state Ministry of Lands (or Lands Bureau).

Does it have a title?

You should always confirm the land title with the land seller or real estate developer. Do NOT purchase any land without a title.

A title can be the Certificate of Occupancy (AKA, C of O) or Governor’s Consent. The C of O is a state-provided document demonstrating land rights to an individual; It proves ownership. Governor’s Consent is given when someone buys land that already has a C of O and wants to notify the Governor and the general public that the land has a new owner.

Land title differs from the deed of assignment or receipt the land seller gives after purchase. Those documents just indicate that you’ve bought something. You still need to confirm you didn’t buy stolen property, or worse, land that’s been mapped out for government purposes. Like a coastal road project, for instance.

Run away from “freehold”

Some real estate agents in Lagos will try to sell you land and claim it has freehold rights, meaning you own the land in perpetuity (or forever) and can use it for anything. This doesn’t exactly work because all land belongs to the government. Also, freehold isn’t exactly a land title, and chances are that the land isn’t free from government acquisition. When in doubt, always verify at the Ministry of Lands.

Go with your own surveyor

The seller may try to convince you that the land already has a registered survey plan approved by the State’s Surveyor General, but those can easily be falsified. You should always go with your own surveyor to pick the land coordinates and verify them at the ministry.

Get familiar with the authorities

When buying land, you must verify everything with the Ministry of Lands because land issues quickly become complicated in Lagos state. If proper verification isn’t done, you risk losing your investment.

Also, verification doesn’t end with buying the land. You also need to obtain building approval from the state government before doing anything on the land. If you build something different from what was stated on the approved building plan, the government has the right to demolish it without giving any compensation.

Remember: The government can come for your land

It’s important to make peace with the fact that the government can claim land for major projects at any time, even if the owner has a C of O or Governor’s Consent. The only difference is, having the correct land titles gives the owner the right to sue the government or collect compensation. The owner has no compensation or fighting rights if it’s untitled land.

Is your significant other the best thing since agege bread or is it time to return to the streets?

These are surefire signs that your partner doesn’t mean you well:

They don’t brush their teeth first thing in the morning

Do we need to tell you that they’re trying to suffocate you with bad breath? Stay woke.

They brush their teeth immediately they wake up

Who are they trying to smell good and stay healthy for, exactly? Check the streets, your boo might be there.

They like pasta

If your partner has a taste for creamy pasta and its cousins, your account or your lactose intolerant bowels are in danger.

Their beliefs are questionable

If your significant other is already saying stuff like, “30+ women are expired goods,” “partners don’t need to know about each other’s finances” or “Semo is nice,” why are you still there?

They have to travel 6 times a year

Are they in a weird competition with Bubu? Your partner clearly has no other plans than to erase your account. Avoid them.

You’ve still not seen their apartment

They’re trying to show you that they live on the streets. You have no future there.

Their mantra is “I can’t kill myself”

They spend money anyhow and blame it on mercury and her lucozade. Do you really want to be with someone that discourages you from smart financial decisions and investments in this economy?

All you both do is watch TikTok videos

You: “Baby, I really want to learn more about real estate, Bitcoin and NFTs.”

Them:

They don’t listen to the “To Be Quite Honest” Podcast

If your partner hasn’t told you about this podcast, they obviously don’t mean you well. They talk about real estate, investment opportunities, social trends, and other stuff that’ll bring you out of poverty. It’s not every time food or movies, sometimes think about your future.

To Be Quite Honest Podcast is a fun and engaging stop for everything about real estate investment. Get updates on new episodes on Instagram via @tobequitehonestpod

For millennials and GenZers, real estate agents are the people we love to hate. I talked to Oluwaseun Lisk-Carew, a certified real estate agent based in Lagos and Ibadan, Nigeria, about why there are so many costs involved in renting a house and why the hell inspection fees exist.

Why did you become a real estate agent?

I’ve always loved buildings. In 2020, friends and family encouraged me to give real estate a shot. At the time, it seemed like a lucrative business. I heard agents brag about their commissions even if they didn’t mention figures, so I didn’t hesitate to try my hands at it.

I understudied a few experienced agents for a while and found that I loved touring properties and helping people decide where to live. They showed me how to register my business and get certified as a real estate agent. There is this joy I feel after I close a deal; I can’t explain it. I also picked up interior decor — I’d helped my brother decorate his house even before I broke into the industry.

What does a typical day as an agent look like?