Every week, Zikoko seeks to understand how people move the Naira in and out of their lives. Some stories will be struggle-ish, others will be bougie. All the time, it’ll be revealing.

What’s your earliest memory of money?

My earliest memories were mostly around the rise and fall of my parents’ careers and incomes.

We started small. When I was little, we lived in a boys’ quarter. Then, a few years later, when my younger sister turned three, we moved into a two-bedroom apartment. Things began to look more comfortable. My dad had an architectural firm, and he’d drop me at school each morning on his way to work. In primary school, I had several collections of Enid Blyton books.

I believe we were on track to have a really good life. Then, life dealt my parents bad cards.

What happened?

Things just started to go bad. My dad’s business partner got into some bad deals that negatively affected the firm. Not long after, my mum lost her job as a bank manager due to the 2008-2009 banking crisis.

These events didn’t change our finances much, as my parents still tried their best to provide what we needed. However, I noticed how money affected their relationship. They quarrelled and fought more. It made me start thinking about how important it was for a woman to have money and be financially independent.

I began wanting to do more, to excel at all I did, and gain independence early. Part of it may have been due to the firstborn syndrome, but money definitely played a significant part.

When was the first time you acted on this?

Senior secondary school. I attended a boarding school, and I would save my ₦2k – ₦3k per term pocket money and give it to someone to smuggle contraband in for me. Contraband in this context was anything from snacks to chocolates and sardines.

It was cheaper to buy these items outside school and resell them to classmates for a profit. Sometimes, I pooled money with friends to buy more items, then we split the profit. It was too long ago to remember the exact details, but I often made twice what I spent on items. I did this “business” at different points between SS 1 and SS 3.

I graduated from secondary school in 2017 and got admitted into the university immediately after.

Did you try to earn money in uni as well?

Oh yes. I tutored some of my classmates in 100 level. My tutoring was voluntary, but people sometimes appreciated me with a little money here and there. I used that to augment whatever pocket money I received from home.

My first official job was in 2019, during the holidays just before I resumed my second year. I worked with a family friend as a personal assistant for three months. We didn’t have a payment structure, but she gave me data and transport stipends. At the end of the three months, she gave me ₦50k. It was technically my pay for the months I worked, but she held on to it until the end so I’d have money to take back to school.

I worked with her again during the 2020 lockdown. She’d dismissed her domestic help and needed someone she could trust with her kids. I lived with her family for about four to five months and made about ₦100k.

Finances still weren’t great at home, so after completing these two stints, I started actively job-hunting.

How did that go?

My efforts got me the job I have today. I saw a vacancy for a Customer Experience (CX) intern on an online job site and applied. A tech firm was hiring people to train AI. They were building their CX function and were open to training hires.

Something interesting happened after I applied. The application involved an assessment. Shortly after I completed the assessment, they reached out to ask me to redo it. I think it had something to do with my first assessment not going through, or they wanted to make sure all applicants completed it. Either way, I was grateful they gave me the opportunity to redo the assessment.

I got a ₦40k/month offer letter a day later, but instead of Customer Experience, they placed me in their AI training arm.

Was there any reason for that?

They probably had enough hands in their CX team. I wasn’t mad about the switch because machine learning and AI training were worlds apart from what I was studying in school, and I was excited to learn something new.

The internship lasted three months, and then they converted a bunch of us to full-time staff. My salary increased to ₦70k/month. I should mention that the job was remote, so I was able to juggle my work with school. That doesn’t mean it didn’t often get stressful, though.

A year into the role, I applied for a three-month internship at an investment firm because it was more in line with my course of study. I wanted that career path as an option if the need ever arose. The firm paid me ₦60k/month.

So, at some point, you were a full-time student with two jobs

Exactly. I was on the verge of collapse most of the time, but the money was good. I was balling. I could afford to buy food, pay people to wash my clothes and still have money left to save. I also hired a private tutor (who was pretty much my friend) to ensure my studies didn’t suffer. He’d tutor me for two months before exams, and I’d pay him ₦15k-₦20k per month.

After my internship at the investment firm, I re-focused all my energy on work and school. My trajectory at work has been really good. I’ve been promoted a couple of times, and each promotion has come with a salary increase.

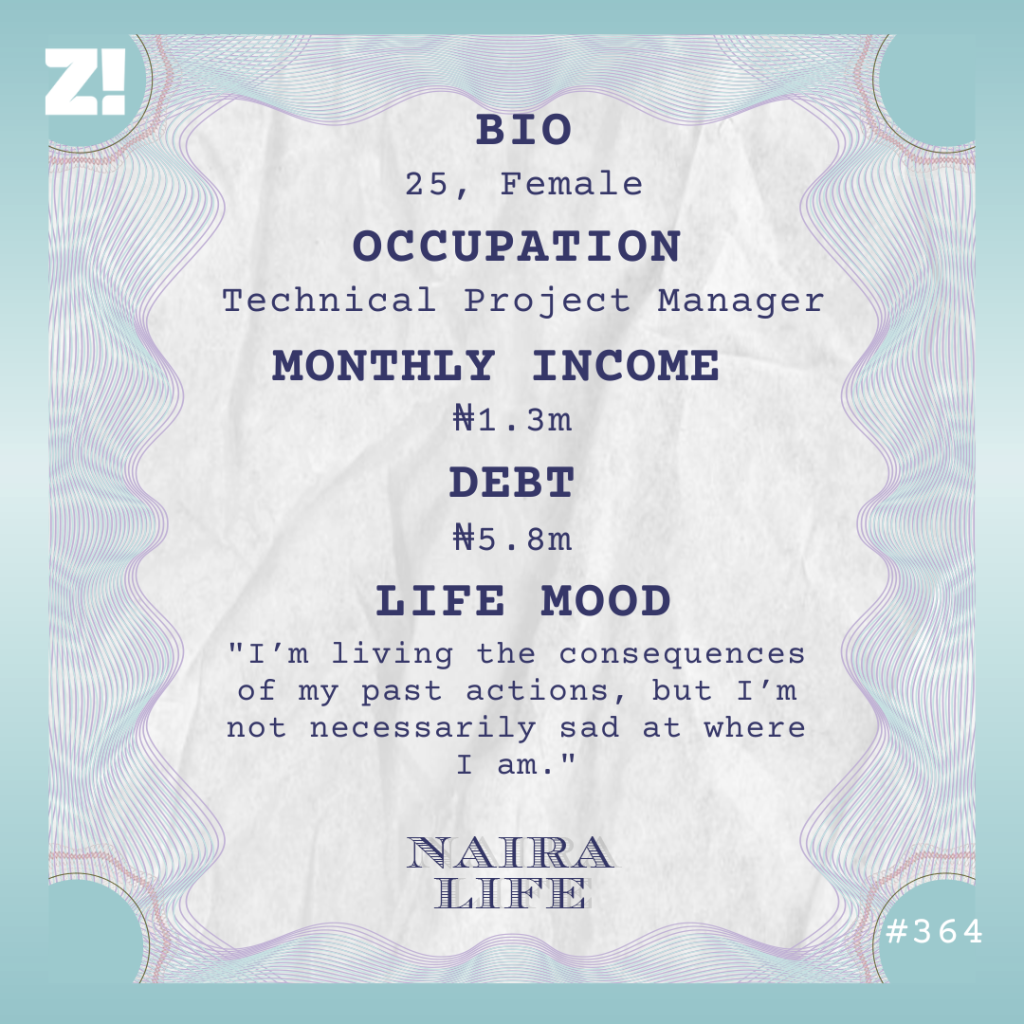

When I graduated from uni in 2023, I’d moved into the role of project coordinator, earning about ₦400k per month. Right now, I’m a technical project manager with a ₦1.3m/month salary.

That’s not bad at all

It isn’t. Interestingly, I’m currently in debt of about ₦5.8m.

Wait. How did that happen?

The debt thing is a snowball effect. When I first started earning money, my parents knew my income. I stopped telling them when the knowledge became a weapon fashioned against me.

Anyway, around the time I was earning ₦400k in 2023, my dad asked me to loan him ₦150k to complete the rent. My money was locked away in a savings app, and it occurred to me that my bank had told me I was eligible for a loan, so I took that. My dad didn’t pay me back, and I ended up repaying the loan out of pocket.

Then I took another loan to buy a phone. I reasoned that Nigeria wasn’t the best place for delayed gratification. I could be saving money, but the price would have increased by the time I was ready. Also, I wouldn’t default on payments, and the loan would be a faster way for me to get what I needed. So, I borrowed ₦700k from my bank to buy a phone.

That’s how I grew used to taking loans. It wasn’t like I was addicted or needed loans to augment my living expenses. My salary met my basic needs. The loans only came in handy for lending my dad money (which he didn’t repay), and for big needs I couldn’t afford at once.

In 2025, I took my largest loan — ₦3m to renovate my room in my parents’ home. I took that loan because I felt trying to save for the renovations would take me too long.

The thing about loans is that the interest compounds. When I take a new loan on top of an existing one, my monthly payments increase. The interest rate is about 4% per month. That’s how my debt has snowballed to ₦5.8m.

Do you regret taking the loans?

Not really. I don’t necessarily feel bad about them. The loans were a means to an end, helping me meet important needs faster.

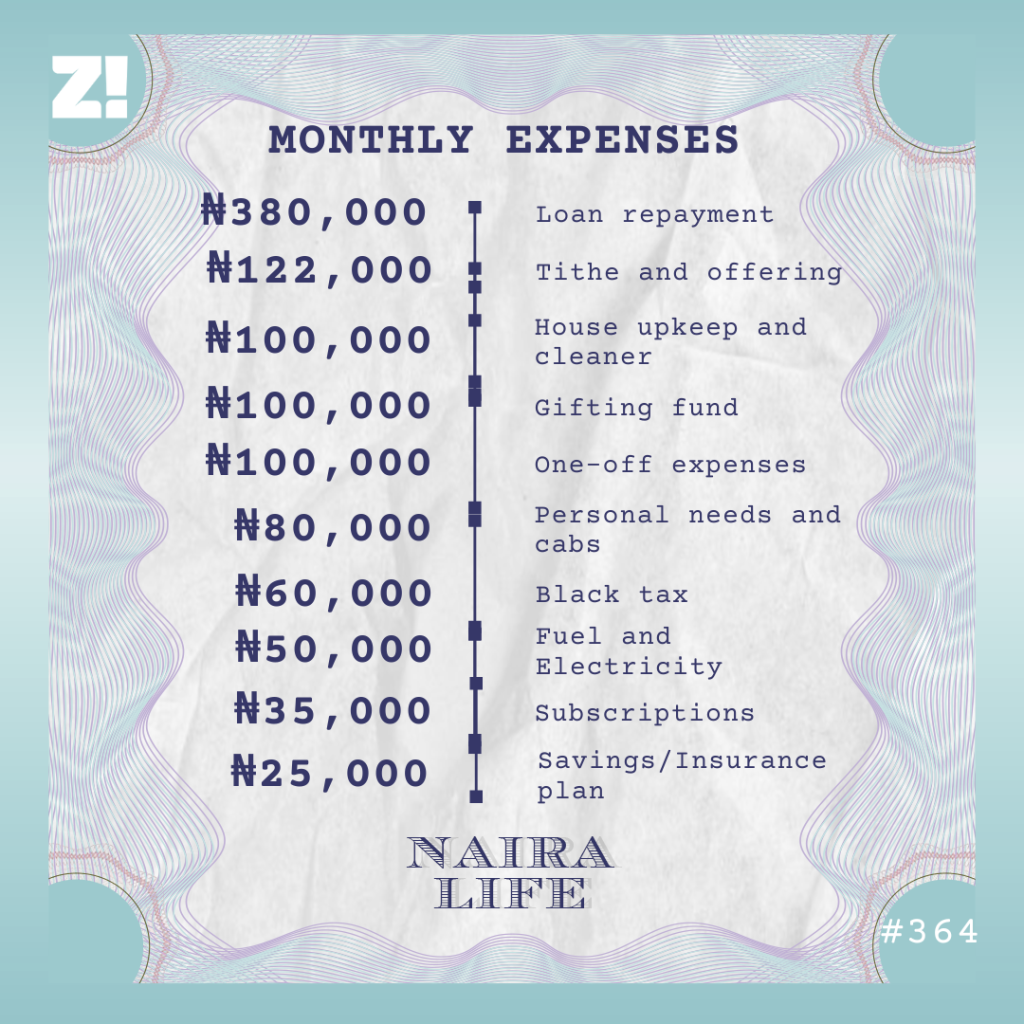

What I don’t like is how the debt is now weighing me down. I have to set aside about ₦380k every month to pay back debt, and with my current income, I’d be repaying debt until the end of 2027.

₦380k is a large chunk of my monthly expenses. By the time I remove family responsibilities and other expenses, I’m left with very little money.

So, it often feels overwhelming. If I didn’t have debt, I’d be adding that money to my savings and feeling a lot more comfortable. I’m hoping for a better job so I can fast-track my repayment plan.

Can you break down your typical monthly expenses?

The insurance savings thing is part of a ₦300k/year life insurance plan I’m doing because of my mum. She works with an insurance firm, and I’m just doing it so she can get the commission. The idea is that if I die within the year (God forbid), my next of kin will get about ₦1.5m. But if I don’t die, I get back my ₦300k with a little interest.

Also, in this budget breakdown, I have ₦200k set aside for gifting and one-off expenses. I don’t always spend the full budgeted amount, so whenever I don’t, I put the money in my savings. Right now, I have about ₦900k there.

You started at ₦40k at your current job and now earn ₦1.3m. How has the income growth impacted your views on money?

That’s a very reflective question. I think it’s important to niche down in a specific area, career-wise, to increase one’s earning capabilities. I believe that once you’ve expanded your skill set and established expertise, you can secure job security and access top-paying opportunities.

I’ve also realised money is an interesting thing. Someone can have all this money now, but if they don’t manage it well or make good use of it, they won’t know where it’s all going.

Is there an ideal amount of money you think you should be earning right now?

$3000/month would be ideal. It’s in dollars because a lot of my work has to do with serving foreign companies, and I’ve built capacity in my field. I know I can do so much more, and my target audience is a foreign employer.

What’s something you’d like to be better at financially?

In retrospect, I shouldn’t have gone into debt as much as I did. It’s like my income grew quickly, but my financial discipline didn’t grow at the same speed. I guess I was just riding on the wings of “buy now, pay later.” Over time, I’ve learned that it’s not always the best way to go.

I mean, loans have advantages, but now I can’t make certain investments because I’m repaying debt and have limited cash flow. If I weren’t, I could be saving ₦500k-₦600k monthly and considering investment options.

Let’s assume you’ve cleared out all your debt. Do you think you’d still take the credit approach to solving your needs?

I don’t think so. I’m now able to match my needs to my income. Also, I’ve realised that the compounded interest is much higher than if I were to save for a few months.

Is there anything you want right now but can’t afford?

A car. It should cost me between ₦10m and ₦15m. However, if my plan to change jobs and earn a better income goes well, I should be able to save up and buy one.

How about the last thing you spent money on that made you happy?

My room renovation project. I spent a lot of money. I got a TV, upgraded my workspace, and made the space a more conducive work environment (since my room doubles as my home office).

How would you rate your financial happiness on a scale of 1-10?

5. I’m living the consequences of my past actions, but I’m not necessarily sad at where I am. My money habits sort of deviated, but I’m still doing quite well. I’d be much happier when I’m debt-free and working a better-paying job.

If you’re interested in talking about your Naira Life story, this is a good place to start.

Find all the past Naira Life stories here.

The Naira Life Conference is returning in June 2026! Expect honest conversations and insightful sessions on building wealth, scaling businesses, as well as practical strategies to manage your money. Join the waitlist to be the first to know when tickets start selling.