Every week, Zikoko seeks to understand how people move the Naira in and out of their lives. Some stories will be struggle-ish, others will be bougie. All the time, it’ll be revealing.

Tired of your money giving you zero returns? With Mkobo’s Save & Win, your ₦10,000 could turn into ₦1,000,000 —no stress, no long stories. Just save smart and win big! The more you save, the higher your chances. Click here to get started. #EveryKoboCounts

What’s your earliest memory of money?

I made my first “big” money in 2011. I was in 200 level and had just gotten an undergraduate scholarship from an international company. They paid me ₦150k. It was the first time my account saw that kind of money.

I didn’t even need money. My parents covered school fees and regularly sent pocket money, so I wasn’t sure what to do with ₦150k. Ultimately, I gave my mum ₦100k and spent the remaining ₦50k on food and random things.

Mad. How much was pocket money?

It wasn’t a specific amount, but the least amount was ₦20k. Also, I could always go home for more money or foodstuff if I ran out. My parents were pretty comfortable — we weren’t wealthy, but we were comfortable.

I received the scholarship every year until I finished uni, but subsequent payments were ₦75k. I also received ₦50k yearly from my uni for being a first-class student, meaning I was sure of ₦125k annually. Most of my money went into buying food. I didn’t enjoy cooking, so I ate a lot at restaurants.

When was the first time you worked to earn money?

2015. I had finished university and was on a three-month internship in a consulting firm owned by a relative. The job paid ₦30k/month.

NYSC came next, and I spent the entire service year job hunting, fine-tuning my CV, and sending cold emails on LinkedIn. My first proper job came after my service in 2016. I was sure I didn’t want anything that paid less than ₦100k/month. Fortunately, I landed an accountant role at a medium-sized manufacturing firm for ₦150k/month.

It was good money for 2016, but I wasn’t very wise with some of my spending choices.

Tell me more

I lived at home, and my parents didn’t ask me for anything, so I thought I was good. I forgot I was now primarily responsible for myself. I continued eating at fairly expensive places and developed a habit of hailing cabs instead of public transportation. I was almost always broke by the middle of the month.

When that happened, my parents grudgingly helped with extra cash. They always said, “You’re working, so there’s no reason we should be giving you money.” When I couldn’t get money from them, I’d take a salary advance from work. My office also had a ₦5k/day allowance for people who worked on weekends. So, I worked Saturdays and Sundays for ₦10k when I was extra broke.

I left after a year for a job at one of the Big Four accounting firms. I was frustrated with my job at the manufacturing firm. My duties were to post sales transactions and invoices on the ledger; a glorified office manager job, and I didn’t feel challenged.

The job at the Big Four was an opportunity to try something new. It was an advisory role, and even though it came with a pay cut, I jumped at it.

How big was this pay cut?

My new salary was ₦120k/month. Besides the immediate benefit of leaving core accounting, my career had better long-term benefits at a Big Four. I could get a promotion yearly, and learning was around the clock.

However, the work was hectic. My closing time at the former job was 5.30 p.m., but leaving work by 8 p.m. at the Big Four was considered early. Most times, I got home by midnight or 1 a.m.

I worked there for two years, and my salary grew to ₦200k. However, my financial lifestyle didn’t improve.

How so?

Working at a Big Four firm exposed me to a lifestyle I couldn’t sustain. This wasn’t peculiar to me; almost everyone who works at the firm experiences it.

I was always treated to lunch from proper restaurants whenever I visited client sites for work. The firm also paid for my cab rides when I worked late. I got so used to taking cabs that I started taking them for personal trips.

Transportation and food were the two biggest strains on my salary. While you could still get meals from local places for ₦500 – ₦750, I frequented restaurants and paid up to ₦3k per meal. I barely had anything left to save when all those expenses came together.

The only savings I managed to have were from a ₦30k monthly deduction for my office cooperative. I was consistent with this because the money went to the cooperative before my salary hit my account. But that ended when I left the firm in 2019.

Join 1,000+ Nigerians, finance experts and industry leaders at The Naira Life Conference by Zikoko for a day of real, raw conversations about money and financial freedom. Click here to buy a ticket and secure your spot at the money event of the year, where you’ll get the practical tools to 10x your income, network with the biggest players in your industry, and level up in your career and business.

Why did you leave the firm, though?

I got a better offer to join a trendy commercial bank as a finance manager. At ₦600k/month, it was triple my Big Four salary and my first big income jump.

Also, it came at a time when it was becoming a struggle to sustain a family with ₦200k. I’d gotten married at this time, and often had to augment my salary with loans to make it to the end of the month. So, the job offer was very welcome.

I can imagine. How did the income jump impact your lifestyle?

I worked at the bank for a year, and I was able to achieve some stability during that time. I upgraded our apartment to a ₦500k/year two-bedroom and furnished it a bit.

I still continued my expensive transportation habits, spending almost ₦100k on cabs monthly, but it was easier to absorb the difference because I earned more. I also didn’t have to rely on loans anymore.

Why did you only spend a year with them?

I got a better offer. An ex-client from my time at the Big Four poached me. I’d consulted on a project for them before, and they wanted someone with experience on the project for my role. I only did one interview stage — I even knew everyone on the panel — and landed the job: $5k/month for the role of assistant finance manager.

₦600k to $5k is crazy

I was so shocked when I saw the figure. My employer is a development bank (also known as a DFI), and I knew they paid well when I consulted for them, but I didn’t imagine joining them or earning that much.

I had to relocate to another African country to work from one of their branches, and fortunately, the country’s cost structure is similar to Nigeria’s. It was like I was earning $5k while living in Nigeria. So, while the cost of things like rent and food remained the same, I became comfortable spending more money. My lifestyle changed.

What were some of these changes?

They were mostly lifestyle upgrades. For instance, I paid $1k/month for house rent in an area that was equivalent to VI or Lekki. I could’ve easily gotten something cheaper, but I wanted something really nice.

I got iPhones for myself and my wife, and increased her monthly allowance from ₦50k to ₦250k. I also increased my parents’ allowance from ₦80k to ₦200k and began contributing to bills much more than I did before.

My new salary also allowed me to begin exploring investments. However, I made some early investment mistakes that resulted in losing money.

Tell me about these mistakes

I bought a lot of US growth stocks towards the end of 2020. I saw how the value of stocks like Tesla, Zoom and the rest went through the roof because of COVID, and I wanted to join the momentum.

Unfortunately, I bought these stocks when their value was high. Within six months, a market downturn occurred, and the prices crashed again. Another mistake I made was selling them immediately. I should’ve stayed for the long run because some of them recovered in a year. I spent $5k on the stocks and lost 70% of my investment.

Damn

Same thing happened with crypto, and I lost some money there as well. The only upside was that I earned significantly enough to absorb those losses, so I took them as a learning experience. But I still wanted to learn, so I found a finance coach online and joined their free personal finance course.

That course started my investment journey properly. I learned I have a moderately aggressive risk tolerance level, and I structured my investment options into three categories: low, middle and high risk. Then I fixed $1k as the amount I’d put into investments monthly; my investment budget.

For my low-risk investments, I invested 30% of my investment budget in fixed-income funds using digital investment platforms.

Then, 60% went into medium-risk investments, which were basically real estate. That included real estate plans on investment platforms, where I received monthly returns, and real estate partnerships in Nigeria. For the latter, I partnered with friends in Nigeria to buy and rent out an apartment on a short-let basis.

The remaining 10% went into crypto, mostly Bitcoin and Ethereum. Crypto served as my high-risk investment channel.

Sounds like a well-thought-out plan

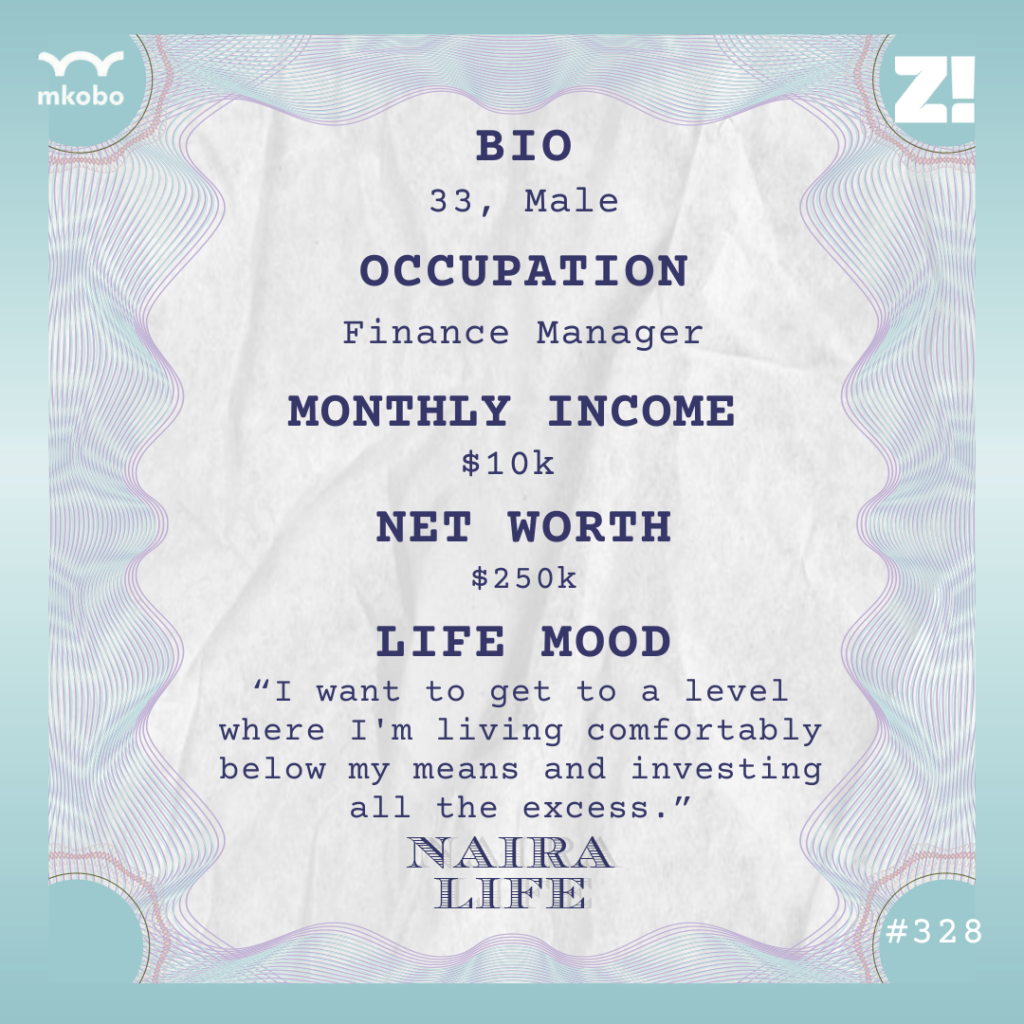

It was, and I still follow the same strategy today, with a few changes. My monthly income is now $10k, so my investment budget has grown to $2k, minus the extra I invest whenever I get bonuses at work. My high-risk investment budget has also increased to 25%.

I should mention that I set up an emergency fund before I started investing seriously. This was the biggest lesson I learnt from the personal finance course. My emergency fund needed to be sufficient to cover my basic expenses for three to six months.

I figured $12k was a healthy base for an emergency fund, so I saved $2k from my salary in USDT for six months. Then I felt comfortable enough to start the other investments. I still channel money to my emergency funds account, usually when I get extra income. I also get 4%-5% annual returns on my savings. My emergency fund is currently at $20k.

What does your total investment portfolio look like today?

My net worth is around $250k, but there are some variables I should explain.

In 2023, in addition to the low, medium, and high-risk investments I explained earlier, I joined an angel network — it’s basically a group of investors who invest in startups. I pay a $1k per annum fee to remain a member, which gives me access to several startups I can fund.

The network recommends specific early-stage investment deals, and the expectation is that each member spends at least $10,000 every year on the recommendations. My angel investments fall under high-risk investments because they are very risky (which is why I increased the budget allocation to 25%, to accommodate angel investments).

Over 50% of startups collapse within the first five years, so the possibility of losing your money is high. Since I joined the angel network, I’ve invested a total of $50k in multiple startups.

I can break down my total portfolio now that we have that context.

I have $50k in startups if I value my angel investments at cost. The companies aren’t listed yet, so I can’t provide current valuations. Then I have another $50k in real estate and fixed-income funds, $70k in US stocks, my $20k emergency fund, and the rest in my short-let apartment real estate investment in Nigeria.

I have two properties for short-let investment: I bought one outright and co-own the other with friends. The apartment I bought was ₦25m at the time of purchase, but its value has increased due to inflation and should now be about ₦50m.

I’m curious. How do you get returns on your angel investments?

That only happens when the company has an exit event. This means that more investors came to invest in the company at a higher valuation, and the angel group gets the opportunity to sell their stake for a profit.

Since I started investing, I’ve only had one exit. I invested $2k in that company and got $6k in the exit event after the angel network removed its 20% fee. Not all angel investments end in a profit. About three or four of the startups I invested in have gone under, so those investments went burst.

Ultimately, angel investment is like playing the long game. Exits typically happen in 7 to 10 years, so it’s not a quick turnaround. Plus, it’s very risky. The best way to de-risk your startup portfolio is to have many companies. If you invest in 20 companies, 50% to 70% might fail. But you only need three or four of them to do very well to get all your money back, plus decent returns.

For example, take those who invested in companies like Flutterwave and Andela when they were valued at $20m – $30m. These companies are now valued at $200m and above. Imagine how much those investors made. I estimate that even if I don’t invest more than the $50k I already have in startups, I should make at least $150k from exit events in five years from the two or three startups that do well.

That’s eye-opening. How would you say your income growth has impacted how you think about money?

To be honest, the only reason you’re probably not saving or investing is because you’re not earning enough. That’s what I’ve learned from my journey. Initially, I was quite reckless with finances, but I changed when I started earning a decent amount.

I know it’s not always the case. Generally, it’s advised that you develop saving habits right from when your income isn’t so great. But that didn’t apply to me. The saving and investment habits came when I started earning a lot. Knowing I had extra made me intentional about how I spent that extra.

How about your lifestyle?

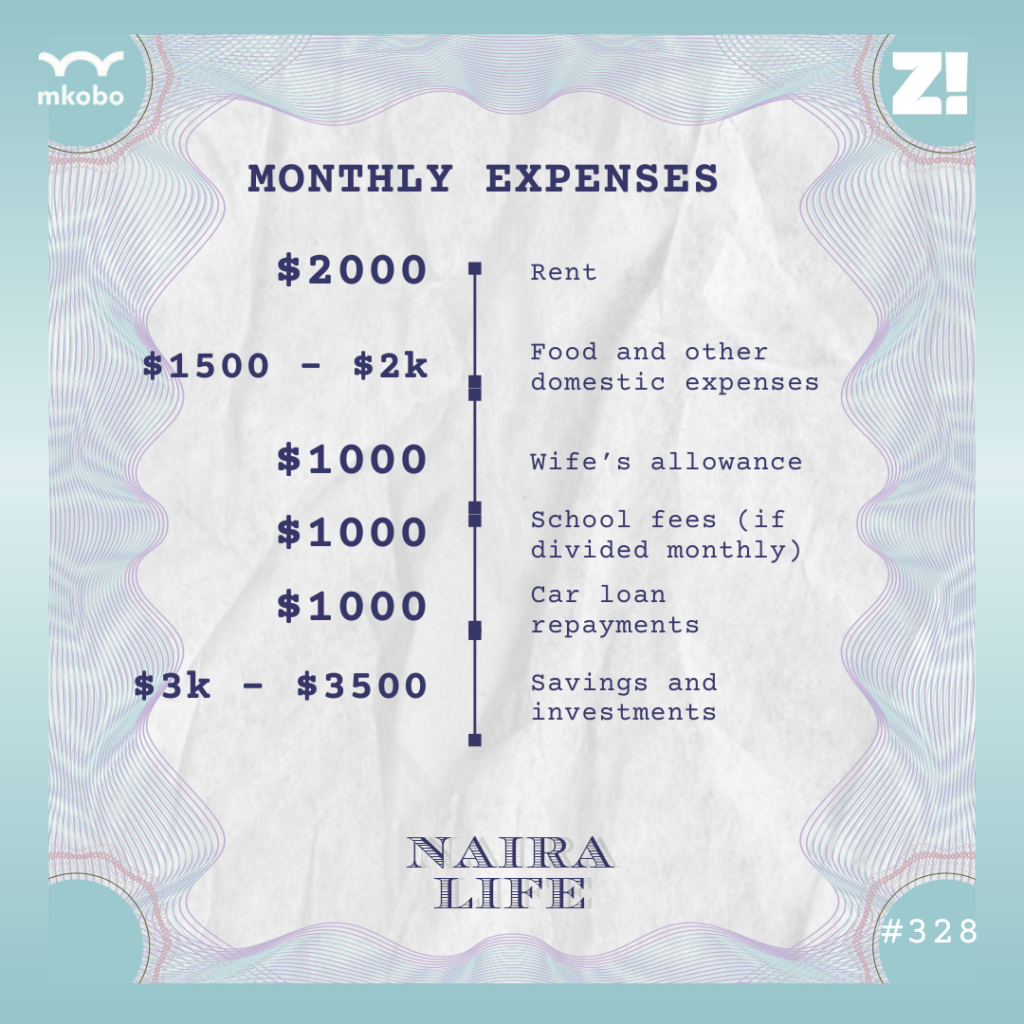

I think it’s inevitable that my lifestyle will change as my income increases. I live slightly below my means, but I can afford a few more things. I live in a bigger house now that costs $2k/month, and I give my wife $1k/month. I make around ₦700k – ₦1m monthly from my short-let apartments, and the whole sum goes into handling my Nigerian expenses, mostly family allowances.

I also frequently go on vacations. I do mini vacations within the country twice or thrice a year, and a proper two-week vacation outside the country with my family at least once every 18 months. These vacations usually cost anywhere between $1k and $10k, depending on where I visit. Although I’m often in Nigeria for work, I also make sure to spend two weeks of personal downtime there every year.

I still plan to cut my expenses to the very minimum. One of my goals is to ensure that subsequent salary increases don’t go toward lifestyle expenses but into long-term investments. I want to get to a level where I’m living comfortably below my means and investing all the excess.

Let’s break down your typical monthly expenses

I took out a $55k loan for my car, and will repay $1k monthly for about five years. I could actually have paid cash for the car, but it was cheaper to fund it with a loan. I got a low-interest loan from my workplace and invested the cash instead.

I’m exploring buying a house in the coming months to cut down on rent or repurpose those payments into owning the house. I estimate a house should cost me $150k, and I plan to secure a loan in the local currency to fund it.

That way, when devaluation happens, it’ll be to my advantage. My source of income is in dollars, so if the rates increase, my effective monthly repayments would reduce.

Is there anything you want right now but can’t afford?

I honestly can’t think of anything.

That’s such a flex. What was the last thing you bought that made you happy?

Probably my car. It was brand new, and I felt fulfilled. I also feel fulfilled when I buy gifts for my wife. The most expensive gift I’ve gotten her was jewellery worth $12k.

Is there an ideal amount you think you should be earning right now?

I’ll look at it from the point of view of net worth. I’ll be fine for life if I have a $2m net worth and only earn at least $5k/month. I think a well-invested $2m would give me very decent returns. I’d also be able to ramp up my startup investments and easily make much bigger returns in the future.

I expect to reach $2m in 10 years maximum. It could also happen as quickly as 5 years. My startup investments can make that happen.

How would you rate your financial happiness on a scale of 1-10?

8. I believe I would’ve been doing much more in savings and investments if I’d planned properly early on and started my investment journey with the right knowledge. I wouldn’t have made those early mistakes.

If you’re interested in talking about your Naira Life story, this is a good place to start.

Find all the past Naira Life stories here.