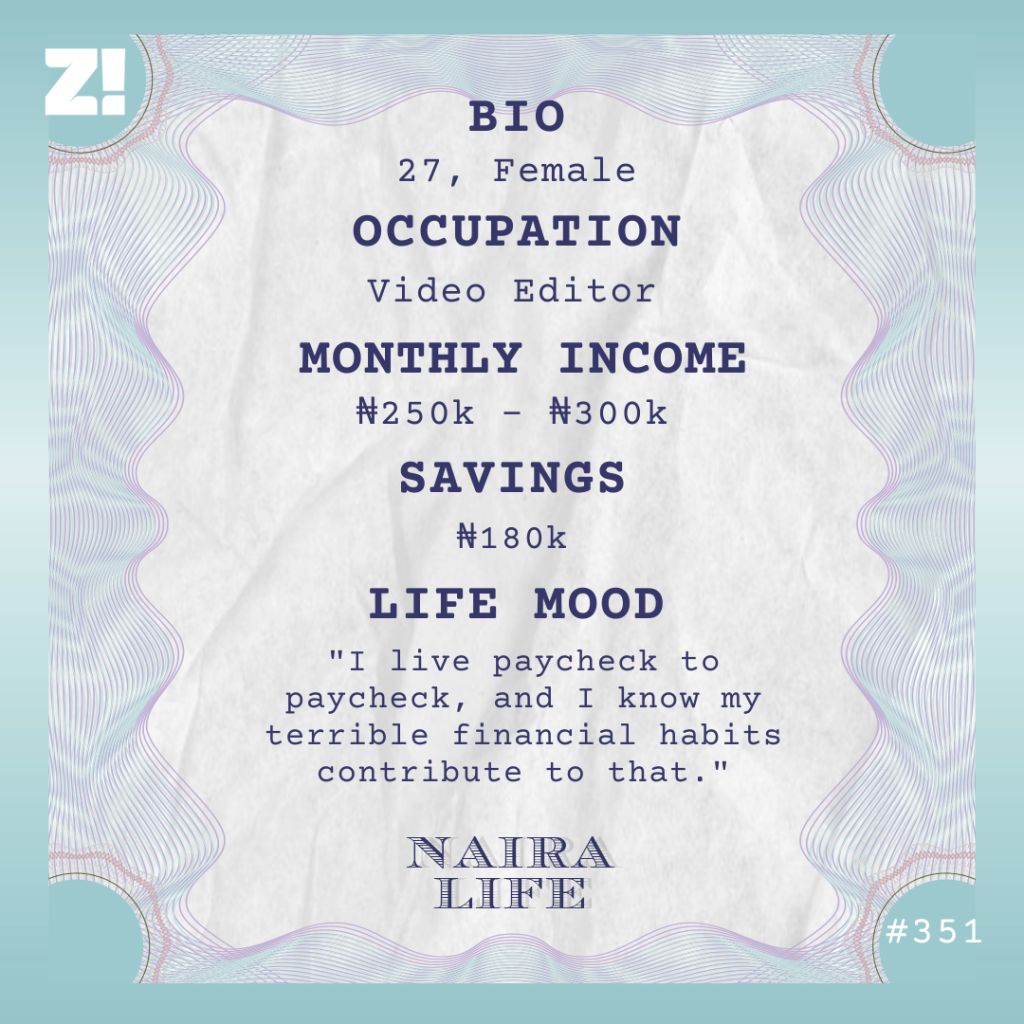

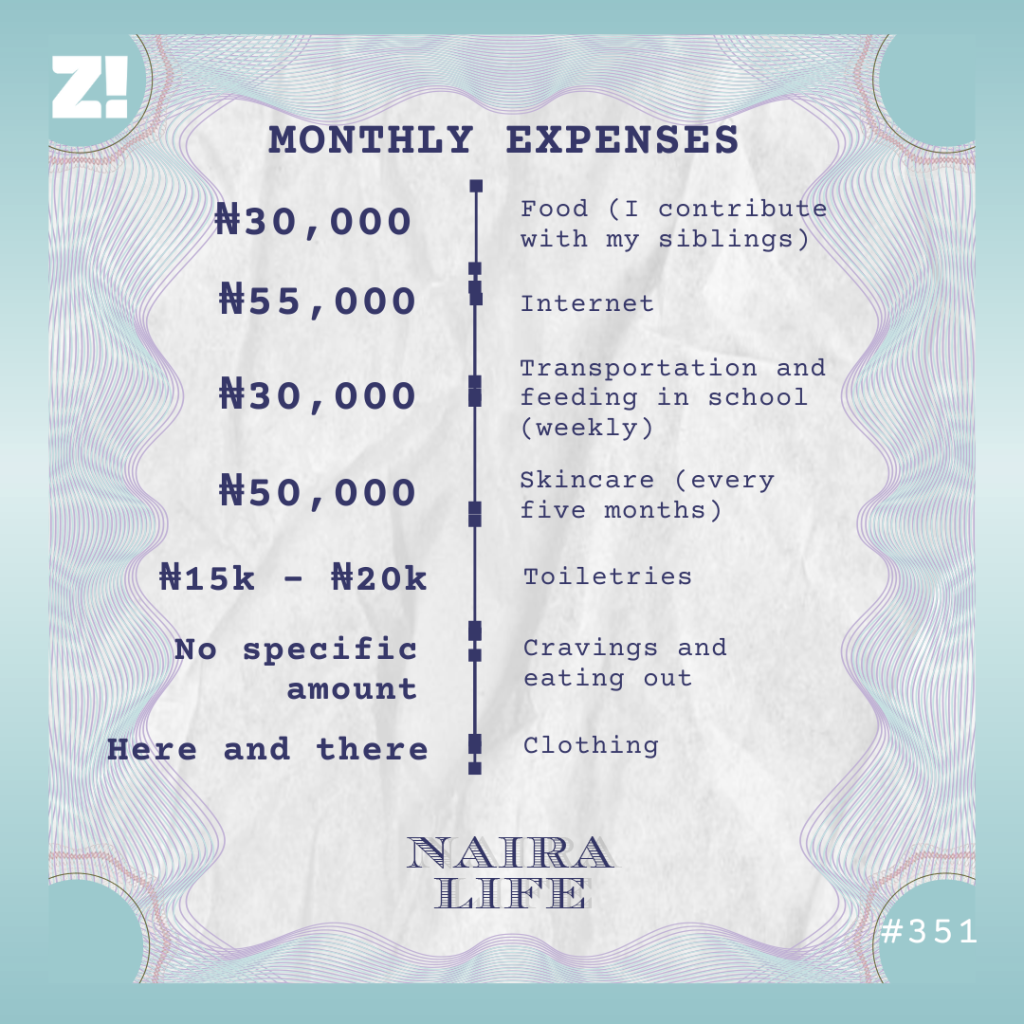

The topic of how young Nigerians navigate romantic relationships with their earnings is a minefield of hot takes. In Love Currency, we get into what relationships across income brackets look like in different cities.

Interested in talking about how money moves in your relationship? If yes, click here.

How long have you been with your partner?

My wife, Rhoda, and I have been together for six years and married for four.

How did you meet?

Through a mutual friend. I needed a tailor to sew some outfits for a family event, and I remembered my friend who always looked sharp in native attire. So, I asked for his tailor’s details, and it turned out to be Rhoda.

The first thing I noticed was how pretty she was. Also, she seemed really hardworking. I went to her studio to give her the materials, and the place was filled with apprentices, with customers dropping in at intervals. I love seeing young people do really good work, and besides her beauty, that was another thing I admired about Rhoda.

I didn’t fall in love on the spot, but there was definitely fascination at first sight. Even when she delayed my outfits and gave multiple excuses like Nigerian tailors usually do, I didn’t get angry (laughs).

So, how did you move from a working relationship to a romantic one?

After I got my outfits, I kept chatting her up at intervals. At first, she wasn’t the most responsive. But she must’ve noticed I was trying to get close because she eventually started responding regularly.

We talked for almost a month before we went on our first date at a restaurant I’d been meaning to check out. I spent about ₦35k on food and transportation for that date. That’s where I popped the question: Will you be my girlfriend? She said yes.

That’s sweet. What were your finances like at the time?

I’d just gotten my first official job, earning ₦100k/month and squatting with my brother to save on rent expenses.

Rhoda and I didn’t really talk about each other’s finances while we were dating, but I’m sure she made more money than I did. Her business was quite successful, and she even bailed me out with the odd ₦10k once in a while when I went broke before salary day.

Also, after we got engaged, she often visited me at my brother’s house to cook for me out of her own pocket. So, while we didn’t actually sit down to track how much either of us was making, we had this unspoken agreement that we’d do nice things for each other whenever we had money. For instance, Rhoda hasn’t paid for internet ever since we got together, because I always buy her data. She also buys me stuff, so it’s vice versa.

The first time we made a specific effort to discuss our expenses was during our 2021 wedding planning.

What did you both agree on?

We agreed that it wasn’t realistic for me to handle all the expenses. I think my salary at the time was just under ₦200k/month, with a few side hustles bringing in extra money here and there.

So, we agreed that I’d handle bills like the hall and photography, while Rhoda would handle the outfits and her makeup. Our parents chipped in to help with food, hall decoration and other small expenses. It wasn’t a big over-the-top wedding. We just did what we could afford. I’m not sure our total expenses reached ₦2m.

What’s the financial dynamic like now that you’re married? Do you still split bills?

Yes, we split bills. However, I can’t say we’ve settled on an approach that works for us. I think this is because we didn’t clearly share our financial expectations with each other before marriage.

I believe that my money is our money, and my wife’s money should be ours too. When one person brings out money to pay house rent or buy food, it’s not a case of “I paid the rent,” it’s all our money. So whether it comes from my wife or me, we should use it together for the good of our home.

However, Rhoda can be particular about her money. She believes I should take on the bulk of the expenses, so whenever she has to pay for something, she complains or acts like she’s shouldering my responsibility.

It’s strange because she didn’t give me this impression of her when we were dating. Or maybe I didn’t notice because we didn’t have shared expenses.

Get More Zikoko Goodness in Your Mail

Subscribe to our newsletters and never miss any of the action

Hmm. Does this cause friction between the two of you?

At first, we fought a lot about it. I’m a salary earner, so it’s inevitable that I’ll be broke before salary day.

So, what usually happened was that I’d spend all my money on transportation and household expenses. When it finished, I’d ask her to support my transportation and pick up the rest of the bills.

I didn’t know she found that uncomfortable. To her, it was as if I was forcing her into a breadwinner role and collecting her money. So, she’d complain about it, and that didn’t go down well with me. It felt like she was saying she didn’t want to contribute at all. As a result, we fought a lot about money in the first two to three years of our marriage. We even saw counsellors in church.

We’re better now, but it’s not necessarily because Rhoda has changed; I’m just learning to live with it. She now covers most of the food expenses, while I handle the rest. Despite that, she often complains about how expensive things have become, but I just try to ignore her. Sometimes, I support the food expenses. Other times, I simply tell her to manage what we have. If there’s no money, we can drink garri.

Do you both know what the other earns now?

My wife knows how much I earn. She also knows that I regularly take on side hustles to cover expenses, but we don’t really discuss how much I earn from side gigs because the amount is not a constant figure.

My wife doesn’t work a salaried job, and I don’t track everything that enters her account, so I can’t say this exact figure is her monthly income. However, since we’ve been taking our money issues to counsellors, she’s been trying to be open about her income. She can just say, “A client paid me ₦50k today, so I used it to buy chicken” or something like that.

I still think she isn’t pulling her weight, though. I mean, she helps, but I don’t think she’s contributing fairly. I work multiple jobs to earn around ₦600k monthly, but we’re not living a good life. It’s even more difficult because we have a child. I believe we’d be more comfortable if my wife were more open to pooling resources, but raising matters like this often leads to long talk, so I just let it be.

Interesting. Do you both have safety nets?

It’s mostly for rent. Our rent costs ₦800k/year, and I save ₦50k monthly, while Rhoda pitches in whenever she has extra money to make up the full amount. I also have a different ₦50k/month savings for emergencies. I have a little under ₦800k in the emergency fund.

Over the years, we’ve had to take loans for major projects. For instance, in 2022, we took a ₦1m loan to set up our solar electricity system and inverter. I don’t think I’ll do that again anytime soon. Since I couldn’t manage to save and repay the loan at the same time, I asked Rhoda to fund part of the monthly repayment — we were paying around ₦100k/month, so she was bringing ₦65k. I know the complaints I got from her during that period. It’s like, you’re also enjoying this thing, but you want me to carry all or most of the financial burden because I’m the man. That’s not realistic.

I just hope things will continue to improve and we’ll understand each other better as we spend more time together.

How do dates and gifts work in your relationship?

Dates are usually limited to birthdays and anniversaries. If it’s my birthday, my wife takes me out and handles the bills and vice versa. I usually handle the bills for anniversary dates, but we buy each other gifts. For our last anniversary, Rhoda bought me a pair of shoes, and I bought her a jewellery set for ₦20k.

What’s your ideal financial future as a couple?

I’d just like us to be a true unit when it comes to finances one day. I think it’s only then that we can have big dreams, such as owning our own house or relocating in the future.

Interested in talking about how money moves in your relationship? If yes, click here.

*Names have been changed for the sake of anonymity.

If your long-distance relationship (LDR) is caused by one or both partners being frequent travellers or digital nomads, you’re dealing with a different kind of challenge. In most LDRs, the main problem is partners missing each other. However, in addition to that, you’re dealing with navigating time zone differences, cross-border payments, spontaneous travel changes, and financial stress.

It’s a whole lot, and if you spot these signs, it means your relationship might struggle to endure the complexities of life on the move.

Someone refuses to adjust for time zone differences

In a travel-based LDR, scheduling calls involves making significant shared sacrifices. Is your boo in a time zone seven hours away, and they always expect you to be the one to stay up until 2 a.m. for a quick call?

A good partner shares the inconvenience. If they can’t lose two hours of sleep to spend time with you, do we really need to tell you there’s a problem?

You genuinely don’t know when you’ll see each other again

If you and your partner haven’t discussed a concrete plan, date, and budget for the next time you’ll physically see each other within the next 6-12 months, your relationship is likely running on vibes.

A small travel change sends them into financial chaos

Travel is all about unexpected changes. A flight can get cancelled, or you urgently need to make an emergency payment in a foreign currency.

If any of these spontaneous moments sends your partner into panic mode because of the fear of bank fees or getting stranded without access to their money, they’re probably not equipped for this lifestyle. When your partner is far away, you need them to be financially flexible and prepared. If they are still stressing over basic cross-border payments, they are wasting energy that should be spent on you.

They’re still paying wild fees for currency exchange

You and your partner are essentially throwing money away if you’re paying high airport exchange rates and incurring multiple international transaction fees every month.

You can’t be serious about travel if you are not smart about money. This is where Timon comes in. It’s the one fintech app that simplifies payments, currency exchange, and secures international transactions, ensuring your money works everywhere, without limitations.

Instead of sifting through multiple fintech apps to find one that works with your naira abroad, think of Timon as the only financial passport you need for global travel.

Your calls are filled with complaints about travel logistics

If every video call is dominated by complaints about visa woes or payment issues without space for a genuine emotional connection, your romance might be on holiday. Besides, why should you still be dealing with the stress of travel when you can go the Timon way?

Ready to upgrade your life (and your wallet)? Get Timon

If your love is strong enough to survive international borders, it deserves a financial tool that makes life smooth.

Timon is the essential travel fintech app simplifying global payments and effortless connectivity with a range of exciting features:

The Timon Black Card gives you the freedom to pay seamlessly using Google Pay or Apple Pay, making transfers to merchants across African countries without the usual hassle.

The Timon USD card allows you to fund your account in naira and spend internationally with ease. On top of that, global eSIMs keep you connected 24/7, no matter where your travels take you.

Whether you are a frequent traveller, a remote worker, or someone who simply wants to enjoy better payments across borders, Timon brings all these solutions into one easy-to-use app.

So, download the Timon app today, sign up, and explore all the different ways Timon makes your money work everywhere, without limitations.

[ad]

Every week, Zikoko seeks to understand how people move the Naira in and out of their lives. Some stories will be struggle-ish, others will be bougie. All the time, it’ll be revealing.

What’s your earliest memory of money?

I began to have a strong desire to make money when I was 11 or 12 years old. It was largely due to my family’s financial situation. I didn’t know what having money meant, but I knew what poverty looked like, and I wanted better.

Tell me more about your family’s financial situation

I was raised by a single mother who didn’t make a lot of money as a civil servant, so things were difficult. While my friends attended private school and received toys, I attended public school and managed food.

I noticed this difference in our quality of life pretty early, so I often thought about making money. The first time I was able to do so was at 15 years old.

What did you do?

I taught primary school students. I was still in secondary school at the time — either SS1 or SS2 — but I’d work as a holiday lesson teacher for makeshift schools in the area for ₦4k/ month.

I also made money running errands for people, mostly in the ₦20 or ₦50 change they told me to keep. There was also an estate beside my street where I’d go to help rich people bathe and walk their dogs for little money here and there. When the dogs had puppies, I helped the owners market and sell them on an online marketplace and earn between ₦2k – ₦4k in commissions.

I finished secondary school in 2016 and returned to teaching at schools. The first job I got paid ₦8k/month, but I worked there for only two months. I was more of an errand boy and cleaner than a teacher. I moved on to another school that was supposed to pay me ₦12k/month. I didn’t last one month there because the middle-aged proprietor began to move funny.

How so?

The man was making some “funny” sexual advances. I ignored him until he started asking me to wait behind after others had left. Ah, I resigned immediately.

Next, I worked as a cleaner at a school for ₦15k/month. I worked there for three months before I got an admission offer to the university. This was still 2016.

Did you also try to make money in uni?

I had to. I didn’t have a specific allowance from home. Sometimes I’d get ₦2k per week, other times ₦5k or even ₦1k if I collected food stuff. Money wasn’t consistent, so I needed to find ways to support myself. I did that by rearing rabbits.

Rabbits?

Yes. I love animals. I bought one rabbit, which I reared at home before I got into uni. She gave birth to six kits. Three died, and I took the remaining three with me to school when I resumed. That drew attention to me, and I became the guy who bred rabbits.

Gradually, people started to find me whenever they wanted to buy rabbits. I’d help arrange the purchase from a farm and earn commission. Over time, I expanded my operations and used any extra money that came my way to buy a few more rabbits and build a cage. That way, I could breed my own rabbits, sell them, and make a higher profit. I was selling them as pets, not for meat, but I was still making good money.

“Good” might be a stretch because I’m talking like ₦3k/week, but for someone who often trekked an hour to school because of transport fare, it was good enough for me to survive.

You mentioned you were selling the rabbits as pets, not meat. Is there a difference?

Yes. To sell rabbits for human consumption, you need to sell in large quantities to be able to meet clients’ demands. That’s big man business, which I didn’t have the capacity for. I only had like 7 or 8 rabbit kits a month. So, selling them as pets was the way to go for me.

People hardly bought rabbits as pets, but I had a strategy that allowed me to sell them at a premium price. I’d create content about how rabbits were quieter, cheaper to feed and maintain than dogs. I also spread the word that my rabbits were trained. Rabbits aren’t easy to train, but since mine were often in my room, they got used to being around humans.

I’d make videos to show how I could call them to come to me. The rabbits came because they knew I probably had food, but to people, it showed that the rabbits were trained and could listen to commands. So, while others could sell a rabbit for ₦1500 or ₦2k, I could sell mine for as much as ₦5k or ₦8k. Guys even bought them to gift their girlfriends. Business was good.

However, as I was getting money, everything went back into the business. I had to expand and feed the rabbits, and it became difficult to maintain. Then, a bag of rabbit food was ₦3k. Imagine a struggling student buying bags of food every week for rabbits.

So, even though the business grew very fast in just a year, it fell off just as fast. The final blow came when I was in 200 level.

What happened?

There was an outbreak of the RHD virus that unfortunately affected my rabbits. I had 8 breeding does at the time and I lost them one by one. I tried different remedies, even asked the person I got them from, but nothing worked.

So, whenever I noticed one got sick, I’d ask my roommate to put it down, so at least we could eat. I eventually sold off the remaining three for about ₦26k and the cage for ₦1k. I was able to make that much from the rabbit sale because one of them was an imported Angora rabbit I’d bought for ₦30k. I eventually sold it off for ₦20k. That’s how I stopped the business.

Get More Zikoko Goodness in Your Mail

Subscribe to our newsletters and never miss any of the action

Phew. Sorry about that. What did you do next?

I briefly worked as a hostel agent and reposted pictures and videos of available hostels from another agent.

The first day I went for a physical inspection myself, I realised there are some jobs that need you to be mentally and physically fit. I went down with malaria after one inspection waka and decided the business wasn’t for me. ₦4k in commission was the only money I made from that stint.

During this period, forex had started to gain ground in my city. Someone I knew from another hostel did a giveaway, which I participated in but didn’t win. Then I entered his DM and was like, “Omo, this giveaway you did. I’m broke o. I really needed the money.”

He asked me to come to his office to see him. I did, and he told me how I could start a forex business.

He explained that I could raise money from people, invest it on their behalf, and collect a percentage of the profit. He gave me ₦4k to start. With that ₦4k, I designed a flyer and started posting about the forex opportunity.

To be clear, were you trading forex?

No, I was just the middleman. I worked with a trader who traded the money for about two weeks before paying out the profit. The profit margin on investments was around 20% – 30% bi-weekly, and my cut was typically 5% or 10% of the total investment + profit, depending on my agreement with the investor (the person whose money I was taking).

For instance, if someone invested ₦1m and we earned ₦1.4m after two weeks, I’d only return ₦1.2m or ₦1.3m and keep the balance. Fortunately for me, people trusted me, and it was easy to convince them to give me their money.

In the first month, I rallied five people who invested between ₦400k and ₦3m. By the end of that month, I had earned ₦1m in commissions. To give you a full picture of how crazy that was, I’d never had up to ₦80k cash at once at that time in my life.

When I saw that ₦1m, I went to the bank and withdrew ₦200k. Then, I took it home, poured the money on my bed and slept on it. I had never seen that amount in cash before. The next day, I packed the money again and deposited it back into my account.

That’s wild. How did this sudden windfall impact your lifestyle?

Omo, I didn’t handle money well, and I think that was natural. I mean, I went from struggling to survive to making my first million. It was a big change.

Some people say that money can’t change them, but I believe it’s because they haven’t seen the amount that’ll change them. Money changed me, and I didn’t quickly realise that I was losing my head.

I started making money from forex, and suddenly I couldn’t cook again. Me, who used to cook palm oil rice and slice onions inside tomato paste to make stew, suddenly realised I wasn’t eating healthy. So, I started ordering food.

I went from eating chicken once in a blue moon to three times a day. Now, I can’t bring myself to eat chicken anymore because that’s all I ate when I started making money, and I’m tired of it.

My lifestyle completely changed. I bought my first iPhone, an 11 Pro Max. Also, I started going to the club, buying expensive stuff and hanging out with friends.

You were balling

I was. People kept investing in the forex business, and I continued to make money. This was around 2019. I even registered my brand as a proper business, employed a graphic designer and social media manager to create content for me. I think I paid the designer ₦15k/month.

It was a structured setup, and I made money. At some point, I had up to ₦9m and was even considering buying a car. Then, you could get a small Toyota car for like ₦1.5m. I didn’t go through with the purchase because I couldn’t drive and didn’t really need a car.

Interestingly, the period when I finally attempted to get a car was when the business came crashing down. This was in January 2021.

It turned out that the people trading the money weren’t legitimate forex traders. It was a Ponzi scheme, and they ran away with ₦6 billion of people’s money, including mine and my investors.

Damn. I imagine your investors tried to recover their money from you

Of course. I nearly died during that period. Interestingly, I had just returned from a vacation and only had ₦32k in my account when everything went to shit. Investors wanted to kill me with calls. Some turned to the police.

One time, I had just returned home from settling police officers after one arrest when a police van from a different station came to pick me up. I became a celebrity; the police were just looking for me. I couldn’t stay at my hostel either because of the guys who wanted to beat the hell out of me and burgle my apartment. I had to stay at a friend’s place.

How did you get out of that situation?

My saving grace was that I’d made my investors sign an MOU. In the document, I’d set up the contract so that they were essentially agreeing to recover only 5% of their initial investment in the event of a crash. I’d done that after a smaller crash had happened to limit my exposure and how much I had to pay back. Many people didn’t read the fine print of the MOU and simply signed it.

So, when that wahala started, I created a group with all 19 investors affected and showed them evidence of what had happened. I’d been clear from day one that I wasn’t the trader; just a middleman. Fortunately for me, most of the people who invested heavy amounts of money chose to let it go. It was the ones who invested little money that wanted to take my life. One of the guys who arrested me invested ₦10k. I eventually returned his 5% as ₦500 data.

I sha found a way to return most people’s 5%. Some of them argued that the agreement wasn’t legal because there was no lawyer present when they signed it. It was a lot of back and forth, but that’s how that era ended.

I lost everything and went right back to being completely broke.

Phew. Out of curiosity, did you invest in any safety net when you were making money?

Hmm. I invested in myself alone. I consider that period the biggest mistake I’ve made, but also not exactly a mistake. There is some money you make in life that only comes with lessons. People say, “opportunity comes but once,” but that’s only helpful when the opportunity comes to someone prepared and mature.

Imagine that kind of opportunity coming when I was barely 19 and with the limited exposure I had. I was bound to make mistakes, and I don’t regret it. I’d make the same mistakes again if the situation repeated itself with the same level of knowledge I had then.

Omo, I lived the life then. Land of ₦1k, I didn’t buy. Instead, I invested in myself aggressively. I went on multiple vacations, started looking good, and bought whatever I wanted. I even bought diamond earrings for the girl I was dating at the time. On her birthday, I used a car to deliver gifts to her. Me too, I know I made mad idan moves. Giveaway dey cry.

I’m screaming. How did you cope with the lifestyle changes that came with losing everything?

It was tough. A few weeks after the forex incident, I travelled out of my school area to stay with a family friend for about a week. I just needed a place to survive. That visit unexpectedly provided me with a lifeline.

When I had money, I’d developed an interest in drones and had bought one for ₦40k just to practice with. When I visited the family friend, I decided to do what I knew how to do: be a middleman. But this time, for drones. So, I got prices from a vendor and began posting drones for sale.

My first sale came with a ₦35k profit. When I closed that deal, I said to myself, “Okay. Maybe there’s something here.” That’s how I started selling drones. I also took on a few drone event coverage gigs and got someone to operate the drone while we shared the ₦15k – ₦30k coverage cost.

Over time, I made enough money to upgrade my drone, which cost approximately ₦500k, then later to a more expensive one. In 2022, I upgraded my business registration to include my drone sales and event coverage business. It’s still my primary source of income today.

I also earn random money from real estate commissions on the side, as I served my NYSC year with a real estate company between June 2024 and 2025. However, it’s not consistent. I don’t market it a lot because I don’t want to take attention away from my major hustle, which is selling drones.

What’s your income like these days?

My income is wildly unpredictable. I run a business, and can’t determine when people will buy. I can make ₦300k this month, ₦1m the next and absolutely nothing for the next couple of months.

In March 2023, I made ₦2m in one month. The next time I made money from drones that year was in December, and I made only ₦40k. That’s how it is. I’m not selling fish. Drones are expensive, and I tend to only make a good profit when people buy expensive ones. I might only make ₦20k on a ₦200k drone, but I can make over ₦200k from a ₦3m drone. Unfortunately, those deals only come occasionally.

Besides the drones, I take on various random jobs to earn money. I can take on a video editing gig today and help someone buy a pet tomorrow for little money here and there. Even if it’s ₦10k or ₦15k, just bring.

I get it

I’m also on the lookout for remote cybersecurity internships. I studied a professional diploma course in cybersecurity during my NYSC year after a Twitter contact told me about a scholarship opportunity. The scholarship allowed me to pay $15/month instead of $30 for the one-year program. I was interested in tech and mostly curious about the field, so I joined.

The only problem now is that landing my internship might mean rearranging my life. I’m not based in Lagos, and most of the opportunities I’ve found require moving there. It’s crazy because these internships don’t want to pay more than ₦50k/month.

Even crazier, I’m seeing jobs requiring three years of experience offering ₦250k – ₦300k. That’s not nearly enough to justify a move to Lagos. So, my goal is foreign remote jobs that pay in dollars.

How would you describe your relationship with money now?

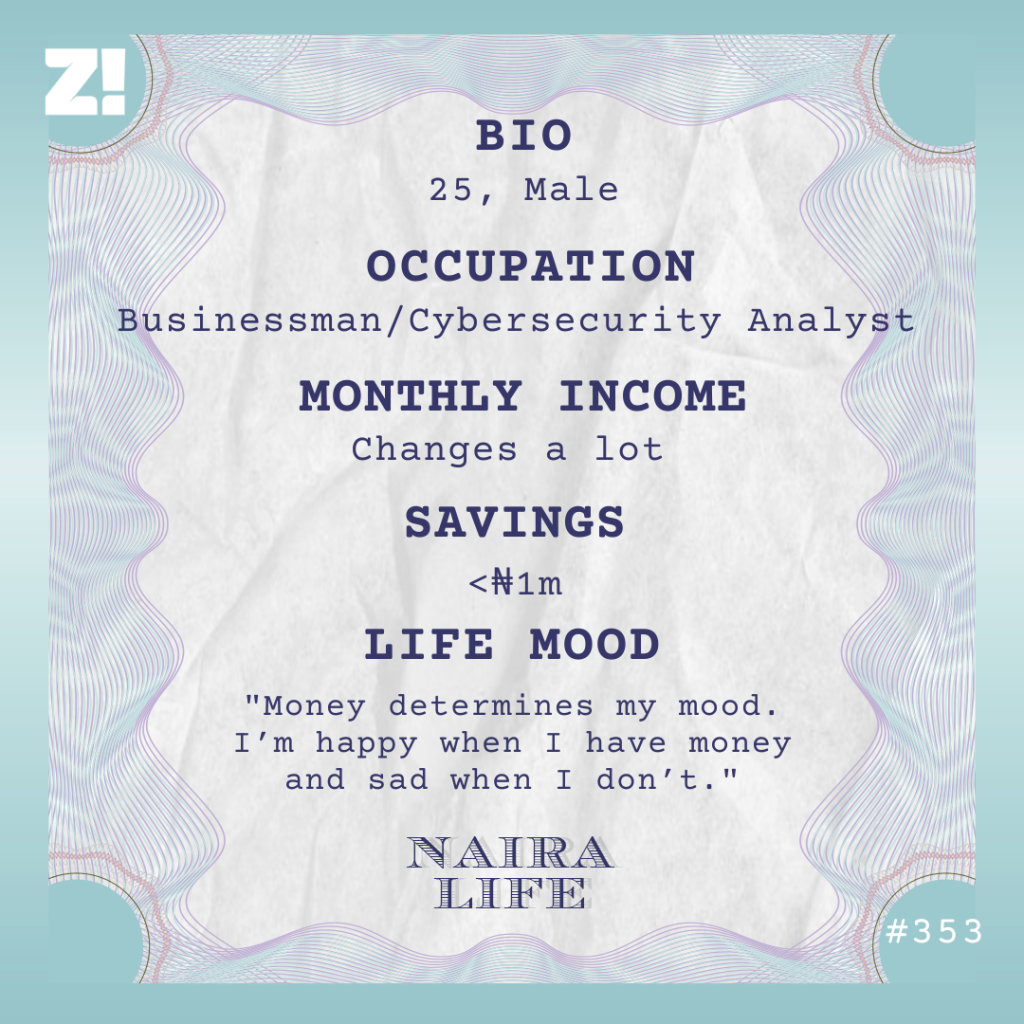

I’ve seen money, so it doesn’t freak me out anymore. It’s safe to say I can’t make the mistake I made when I was touching forex money. However, money determines my mood. I’m happy when I have money and sad when I don’t.

That said, I think I’m in a better place. I’m not where I want to be, but I can manage my life with what I earn. I may not like chicken anymore, but I can afford it. I don’t spend carelessly, but I still make sure to buy things that make me happy.

I also try to save in a way that my savings can “save” me when I’m not making sales. I don’t have a specific figure I save each month, nor do I lock away money. What’s the point of locking it just to enter debt when I urgently need it? So, I just do what I can.

What do your savings look like now?

I don’t think it’s up to ₦1m. My dog has been ill for a few weeks, and I’ve been spending a lot of money on his health. I also recently got some perfumes and am preparing for December oblee and expenses. So, that’ll most likely eat into my savings.

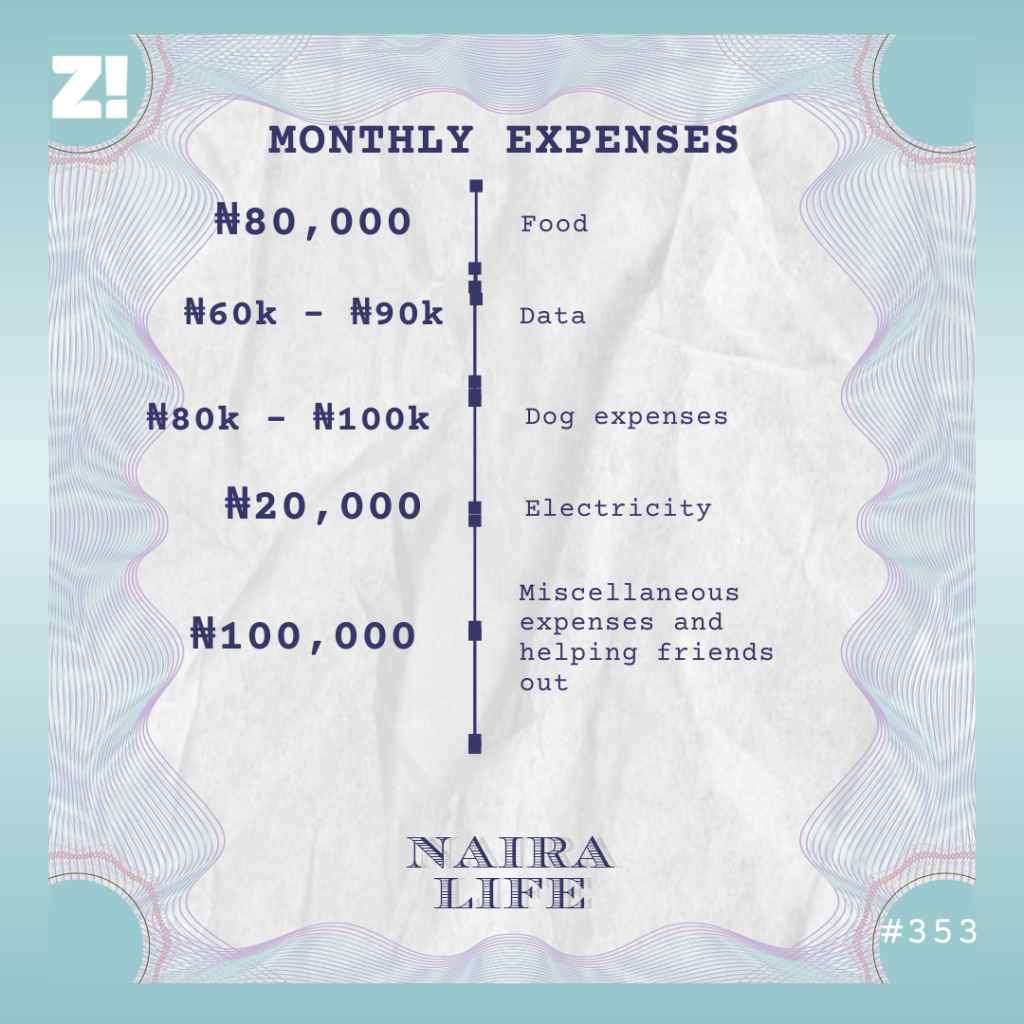

Let’s break down your typical monthly expenses

This depends largely on how much money I make each month. I can spend carelessly when I have money, and be extremely prudent when I’m broke. But here’s a decent average:

What do future plans look like for you?

I hope to have a strong and steady business. I would hate to be working a nine-to-five job. If I have to, it has to be remote work. I just want a stable life with a supportive partner and to be able to afford the basic good things of life. Yearly vacations wouldn’t be bad, either.

Is there anything you want right now but can’t afford?

A power bike. I ride my friend’s own and would really love to own mine soon. I might need around ₦3.5m to ₦4m for that. I can’t even save towards it because expenses keep coming to take away whatever money I manage to keep aside.

I can relate. How about the last thing you bought that made you happy?

I bought my perfume collection a few weeks ago, and my total spend was slightly above ₦200k. I liked that I was able to afford what I wanted.

How would you rate your financial happiness on a scale of 1-10?

5. I’m grateful that I can live a good life to a certain extent. However, I don’t have a stable income, and I’m unable to make long-term plans as a result.

If you’re interested in talking about your Naira Life story, this is a good place to start.

Tunde*, 29, had lived in the UK for barely three months when the requests started pouring in.

It was 2023, and his move on a Global Talent Visa had wiped out 90% of his savings. But the proof his friends and family members needed to believe he now had disposable income was the social media pictures announcing his relocation.

“I didn’t even have a job in the UK yet,” he recalls. “I was still working remotely with the company I left in Nigeria, earning naira and trying to survive as I job-hunted. But how many people could I explain that to? Everyone thought I’d made it.”

Every week, Tunde received WhatsApp messages and Twitter DMs from people asking for financial help and immigration assistance. “A cousin I hadn’t spoken to in years asked me to connect her with an agent who could help her secure a visa,” he says. “When I told her I didn’t use one, and she could find the information online, she said, ‘Just say you don’t want to help me.’”

Tunde’s breaking point came in August 2023 when he woke up to 15 missed calls on WhatsApp from his uncle at 2 a.m. Fearing something had happened, he rang his uncle back, only to find out he was calling to ask for money. His son was getting married, and he wanted Tunde to help with ₦200k.

“He said it was just about £200, so I should be able to afford it,” Tunde laughs dryly. “This man didn’t even know how I got to the UK and how I was surviving. He just heard I was abroad and called to bill me.”

When Tunde refused to send him money, his uncle tried to guilt-trip him, saying he didn’t understand the importance of family. He also reminded Tunde that he’d bought his diapers when he was a baby.

After that incident, Tunde turned off his read receipts on WhatsApp, blocked most of his extended family and locked his Twitter DMs. It’s been two years since, and while he’s in a better financial situation now, he still desperately avoids what he calls the “Nigerian entitlement” to other people’s money.

“Once you start helping out, you can never stop. If you do, you become the devil in their eyes. I’m the black sheep of the family now, but I prefer to be hated than to let anyone suck me dry.”

Tunde’s situation is one that many Nigerians, both at home and abroad, find relatable. Whether you’re landing your first job, announcing a promotion or quietly buying a new car, expectation comes knocking the moment you look like you can give.

In Nigeria, generosity is often expected. Once an individual “blows” (slang meaning an improved financial status), they’ll most likely become a walking emergency fund. Cousin’s rent, friend’s wedding, mother’s church donation, neighbour’s medical bill — everyone looks to the person for help when needs arise.

However, behind the “urgent ₦2k” jokes lies something deeper. In a country where social systems barely function, people have become each other’s safety nets. When healthcare, education, and employment fail, help from others becomes the only form of welfare Nigerians fall back on.

It’s no coincidence that Nigeria remains one of the top remittance-receiving countries in the world. In 2024, Nigerians abroad sent home nearly $21 billion, according to remittance data from the World Bank. This figure marked the highest level in five years, with a notable year-on-year increase of 8.9%. In July 2024 alone, remittance inflows hit $553 million, a 130% increase from July 2023.

While Olayemi Cardoso, Governor of the Central Bank of Nigeria (CBN), attributes these figures to economic reforms and new CBN policies that encourage more Nigerians in the diaspora to choose formal channels for remitting funds, it’s also an indication that many Nigerian residents depend on the financial lifeline from migrant remittances for survival money.

Following a data overhaul, Nigeria’s headline inflation appears to be decreasing on paper (down to 16.05% in October 2025), but unemployment rates continue to rise and remain largely underrepresented.

The inference is simple: With many Nigerians out of jobs or underemployed, and battling with the steep cost of living, success signals ripple out. When someone starts earning well or receives a windfall, they become an entire community’s safety net. More often than not, this knits support and expectation so tightly that boundaries become blurred.

Get More Zikoko Goodness in Your Mail

Subscribe to our newsletters and never miss any of the action

Temi, a 28-year-old product designer in Lagos, calls her family group chat “a monthly GoFundMe.”

“My parents are retired, and my two younger siblings are in university. Every other month, there’s a new emergency: rent, medical bills their HMO plans don’t cover, pocket money and school needs. If I say I can’t help this time, they’ll remind me of my recent purchases or travels. Suddenly, my personal choices are public considerations.”

This communal culture is in action in many Nigerian low-income households. When one child rises, they rise for many. Over time, it becomes less of a choice and more of an obligation.

Yet the pressure isn’t purely financial. It’s also emotional: the guilt of success and the worry that refusal becomes a betrayal.

“I can’t be earning over ₦1 million monthly and leave my family to suffer. It’s unnatural,” Temi says. “My parents took multiple loans to send me to a private university and set me up for the success I enjoy today. My elder brother even had to drop out so I could stay in school. Yes, I often feel overwhelmed with responsibilities and feel like they’re too demanding, but there’s no one else who’ll come to their rescue if I don’t.”

Even though Temi’s income places her in the top percentile of Nigerians, she has almost no savings or a wealth management portfolio due to the expectation of “black tax” and the entitlement that comes with the Nigerian culture of communal success, where money flows upward and sideways before it flows inward.

But when the flow becomes a flood, resentment begins to build quietly under the surface. This phenomenon isn’t limited to family expectations; it also leaks into friendships and relationships.

Chika*, 31, has been close friends with her two friends for 12 years, but over the last two years, she’s noticed a difference in their dynamic. The switch began after she changed jobs and got a 300% pay increase, a move that made her the highest earner in the friend group.

“I began to notice that my friends expected more from me,” Chika says. “We used to pool funds together for group outings and staycations, but now they tell me, ‘You be rich madam na. Pay for us.’”

Chika insists she doesn’t mind spoiling her friends; the problem is that it has now become a constant expectation for her to handle the bills. Once, she joked about spending all her money on her friends, and one of them accused her of being stingy.

The switch from choice to responsibility is subtle. What started as mutual support turns into expectation. And sometimes, introducing boundaries or resistance can sour relationships.

For Chika, resisting this obligation has meant reducing contact [with her friends]. “When I complained, my friend said, ‘How much are you spending? Is it not just our once-in-a-while outings?’ That hurt because it’s not like they’re broke. I’m unmarried; they have husbands who also support them financially. It doesn’t make sense for me to do everything because I earn more. I still love my friends and I know they don’t necessarily mean me harm, but the cost is making me avoid group outings these days.”

While people with friends like Chika can introduce distance to limit financial expectations, it’s a different play in romantic relationships, where money and love seem to be inextricably entangled.

In the realm of Nigerian relationships, the message is loud: if you love me, you’ll support me financially.

Kemi, 27, once dated a man who got upset when she refused to invest in his business. “He said if I believed in him, I’d show it with money. I was like, sir, I’m your girlfriend, not your bank.”

Here again, the expectation is collective success: your partner’s dream becomes your reality. These aren’t isolated incidents; they’re reflections of a society where economic hardship has blurred the lines between emotional and financial roles. When survival is a love language, money becomes a form of affection and a means of validation.

When entitlement doesn’t come in the form of familial or romantic expectations, it shines in the heavy influence of religion.

In Nigeria, blessings are often tied to giving, and giving is connected to being “a good person.” The scriptures come out quickly when someone needs help: “God loves a cheerful giver.” “Your reward is in heaven.”

Adewale, 33, says a random church member once sent him a WhatsApp message that read like a sermon outline, complete with Bible verses about generosity, all because he said he couldn’t loan him ₦500k to start a business.

“It was like he was trying to guilt-trip me with Jesus,” he laughs. “As if refusing to give meant I didn’t fear God.”

Religious communities often operate like extended families. If you’re “doing well,” you’re expected to support church projects, mosque renovations, welfare programs, and allow yourself to be in a position to be someone’s “helper”, sometimes at the expense of your own financial stability.

Your prosperity isn’t just yours; it’s seen as evidence of God’s goodness to the collective. So, when you say “I can’t,” what people hear is “I won’t let God use me.”

Angel Yinkore, Consultant Psychotherapist at Welcome to Truth, says entitlement is a universal human trait, amplified by Nigeria’s communal society and high poverty rates. While it exists differently in the different socio-economic classes, it’s more prevalent and normalised in the approximately 139 million Nigerians who live in poverty.

“When a low-income family rallies to send one child to school, and that child makes it out of the hood, they’re expected to lift everyone else out of poverty or at least provide for their parents and siblings. It’s like a long-term investment.”

This expectation can also transcend family lines. “Because Nigerian societies are more communal than individualistic, everyone in a community feels like a stakeholder in a child’s life,” Angel explains. “So, they expect to share in whatever success the child attains. The more successful a person is, the wider the net of people who feel entitled to their success.

A multinational company could announce you as its CEO today, and people from your parents’ village who have never met you will go, ‘That’s our child,’ as though they had anything to do with it.”

Angel clarifies that entitlement in itself isn’t always a problem. It’s what comes after it. “Nigerians can share in the success of an athlete who represents the country internationally and wins awards. We feel a sense of pride and some connection to that success. However, sometimes, as in the case of the black tax, it doesn’t end with feeling connected to the person. Entitlement then comes with manipulation and threats; an obligation to share your resources.”

Angel emphasises that addressing poverty in the country is crucial to solving the wave of this phenomenon, as people feel entitled due to financial instability and the pressure of staying afloat.

“We have to look at it as a systemic thing. People are poor. You can’t expect someone living on ₦500, then their brother wins the lottery, and you tell them not to feel entitled to help.”

As it is in all things, balance is key to navigating the Nigerian sense of entitlement.

Tunde is adamant about creating boundaries, but he helps when he can. “I call it structured generosity,” he jokes. “I budget what I can give close family members every other month, and I’m done once I hit that limit. I know people still call me stingy, but I’m not doing this to be liked. I know some people actually need help, and I do what I can. Nothing more.”

Finance manager Seyi A. agrees. “Help, but don’t self-destruct. You can’t pour from an empty account. You’re not the government. The best help is sustainable help. Give what doesn’t deplete your finances.”

Sustainable help doesn’t always have to be cash. It could be connecting someone to a job, sharing information, offering mentorship, or even emotional support.

The nuance is that you’re still generous, but you also take care to watch out for your survival. In a country where inflation is a significant concern, and many live without financial buffers, the expectation that one person will carry the burden of many is unfair. Because if everybody owes everybody, no one truly rests.

And in a country where help is both a virtue and a burden, learning when to stop giving might just be the kindest thing we do for ourselves and for each other.

Perhaps the new lens is this: generosity remains a virtue, but entitlement should not be the default.

*Names have been changed to protect the identity of the subjects.

This story is culled from “Zikoko Daily Shorts”, a weekly series exclusive to the Zikoko Daily Newsletter. Subscribe here to receive the newsletter in your inbox every day and get more stories like this, as well as a round-up of our best articles, inside gist and quizzes.

This is Favour’s story, as told to Boluwatife

I was sorting laundry in the bathroom when my phone buzzed with a WhatsApp notification.

It was an unknown number with a DP of a woman I didn’t recognise. I almost ignored it until the first line of her message appeared as a preview:

“Favour, you don’t know me, but I need to tell you the truth about your husband.”

My heart skipped, and I opened the message with fear lodged in my throat.

The woman introduced herself as Maria. She said she’d been with my husband, Joel, for five years, and attached a photo of a small boy who looked disturbingly like him. The boy even had his dimples.

Then came the part that made my legs go weak:

“Joel told me you knew about us. He told me he stopped sleeping with you because he’s no longer attracted to you and can’t get it up anymore. But that’s a lie. He has an STI.”

I froze. An STI? Cheating? A whole child?

My breath shook as I scrolled.

It was true that Joel and I hadn’t been intimate for almost the entirety of our marriage. We’ve been married for 10 years, and 7 years ago, he suddenly became impotent. We bought countless medications, but nothing worked. We even secretly adopted our two children when people started whispering about our childlessness. All the while, he had a child?

Maria’s final line felt like an earthquake in my stomach: “He’s lying to both of us. Call me before he warns you.”

Before I could even process my thoughts, Joel walked into the house.

***

This story is culled from a weekly series exclusive to the Zikoko Daily Newsletter. Subscribe here for more stories like this.

I waited until the kids were asleep before I confronted Joel.

I stood in front of him in our bedroom, my phone in my hand and betrayal burning my throat.

“Joel,” I said, “who is Maria?”

He froze like someone had splashed cold water on his face. “Babe… don’t listen to that woman.”

“She said you have a child with her,” I whispered. “She said you told her you stopped touching me because you no longer find me attractive. But you were sleeping with her? How could you do this to me? After all these years of covering your shame and lying to our families that the kids are biologically ours?”

He tried to step closer, but I stepped back.

“You made me lie for years,” I said, my voice trembling. “I faked pregnancies to protect you. You said you were impotent. We even stopped trying because you claimed it made you uncomfortable. Now I know you just didn’t want me anymore.”

“Favour, it wasn’t like that. Please, let me explain,” he said, eyes red.

“Explain what?” I shook my head. “That you hid a whole child? That you let people call me childless for years while you were living another life in secret?”

He dropped to his knees.

“Favour, I beg you. I didn’t tell you because I was scared. I didn’t want to lose you.”

He explained that he had contracted Herpes from a random woman and stopped sleeping with me because he was scared of giving it to me. Apparently, he didn’t know how to bring up the idea of using a condom without me finding out he’d cheated.

I asked about the situation with Maria, and what he said chilled me to my bones.

***

When Joel and I got married, I thought I’d hit the jackpot.

Growing up religious, my mum had drilled the importance of finding the “right man” into my head for as long as I can remember.

I didn’t have boyfriends in secondary school or university. I was determined that the first man I’d ever give my heart to would be my husband. Marrying Joel was like the fulfilment of that decision, and I felt so lucky.

He was my first love, my first kiss, my first everything. I loved him deeply and was prepared to weather whatever storm life threw at us together. It was why I didn’t flinch even when he became “impotent” or when he suggested adoption without involving our families. I thought we were in it together.

But that night, as I stared at the man I’d loved for ten years, I felt everything crack.

I watched him silently as he explained how he started seeing Maria. Apparently, abstaining became too difficult for him, and she had mistakenly gotten pregnant.

What blew my mind was the fact that he had knowingly infected her with Herpes for his own selfish desires. It was the height of wickedness.

I realised he was a stranger. A man who consciously lied, cheated and denied his wife for years couldn’t be the man I fell in love with.

That was when I made my decision. I was leaving.

By morning, I’d packed a small bag for the kids and told them we were going to Grandma’s house. I avoided Joel’s eyes as he stood in the hallway, looking like a man watching his world fall apart. He’d begged me on his knees all night, but I couldn’t breathe in that house anymore.

I drove out of the compound, tears blurring my vision. But halfway to my mother’s house, my phone vibrated.

Joel’s elder sister was calling. She never called me this early.

Something was wrong.

This story is culled from a weekly series exclusive to the Zikoko Daily Newsletter. Subscribe here for more stories like this.

***

Joel called both families immediately after I left the house and told them I’d taken the children away because of a “disagreement.”

By afternoon, both families were gathered in my mother’s parlour: his father, his sister, my siblings and even an elder from our church. They didn’t know the extent of our disagreement. My mum was already saying something along the lines of, “Why will you just leave home because of a fight? When did you start that one?”

I smiled sadly. “Mummy, this isn’t just any fight. Did Joel tell you he has a child outside our marriage?”

Gasps filled the room, and everyone turned to Joel while he bent his head in shame. Or maybe it was embarrassment. Whatever it was, I no longer cared.

With a shaky voice, I explained everything to our families. How he had made me believe he was impotent, how we lied about my going abroad to deliver when we’d actually adopted babies and the revelation about Maria and her child.

By the time I finished speaking, you could hear a pin drop in the room.

After about three minutes of silence, his sister shot up. “Joel, is this true?!”

He covered his face and whispered, “I didn’t know how to say it. Please beg her to forgive me.”

The church elder looked at me and asked, “Favour, what do you want to do?”

I told him all I wanted to do was find a place I could go with my children. I didn’t intend to forgive him and play “happy family” after everything. I’d already wasted 10 years of my life; I couldn’t waste even more.

While the church elder and my mum tried to beg me to take things easy, Joel’s dad asked a question that made us all stop in our tracks.

“Where is Maria and the child now?”

***

While the families busied themselves with calling Maria and trying to arrange a peace meeting, I felt absolutely nothing.

Wait. That’s not entirely true. I felt intense anger and pain, but I was more concerned about how I was going to start a new life with my children.

When Joel’s father told me they were inviting Maria for a proper family discussion, I simply said, “I won’t be there, sir.” And I wasn’t.

I heard later that they agreed to support Maria and the child. Good for them.

As for me, the first thing I did after moving in with my mum was a comprehensive STI test. When I confirmed I was healthy, I found a decent apartment in town and told Joel to pay for it.

He didn’t argue. He simply asked for the amount and which of my accounts he could send the money to. When I told him, he made a final attempt to convince me to return home:

“Favour. I have sinned against you. I’m sorry. Please forgive me and come back. Let’s think of the children.”

“You still have access to the children,” I said. “But forget anything about me and you. You have the mother of your child to worry about.”

He sighed and ended the call. Minutes later, I received the alert for the amount I asked for. It felt like the final nail in the coffin. He had accepted we were over.

Ten years gone in just a few weeks. What would the next few years look like for us?

This story is culled from a weekly series exclusive to the Zikoko Daily Newsletter. Subscribe here for more stories like this.

***

It’s been three years since the Maria incident, and sometimes I’m shocked at how normal my life feels now. Peaceful, even.

Joel and I never officially divorced; mostly because I haven’t seen the need to go through the court stress. If he ever plans to remarry, he can start the process with his own money.

I don’t know if I can say I’ve forgiven him, but I don’t carry anger anymore. That doesn’t mean I’m interested in giving him another chance. That will never happen. He might even still be with his Maria.

We’re cordial, though. The kids visit him regularly, and I make sure he pays every bill he’s supposed to. We adopted them together, and they bear his name. They’re his responsibility, and fortunately, he handles that without argument.

My friends sometimes ask if I’ll ever consider love again, but I just laugh.

Love? As in romantic love? That’s the last thing on my mind.

These days, I’m learning how to show up for myself and my children. I enjoy finding new hobbies and watching my kids grow. That’s all I need.

Sometimes, I remember everything that happened and wonder at how far I’ve come. It’s a miracle I didn’t lose my mind back then. Maybe it’s something I should be grateful for. I went through the fire and came out stronger.

At the end of the day, I didn’t lose anything.

*Names have been changed to protect the subject’s identity.

Subscribe to our newsletters and never miss any of the action

[ad]

Every week, Zikoko seeks to understand how people move the Naira in and out of their lives. Some stories will be struggle-ish, others will be bougie. All the time, it’ll be revealing.

What’s your earliest memory of money?

The lunch money I got from my mum in nursery and primary school. ₦10 could get me ₦5 buns and a plate of rice.

Those were the days. What was growing up like financially?

Terrible. You know how people say their parents weren’t financially well off? My case was different. The roof of our house was once removed because we couldn’t pay rent. It was that bad.

My dad was an artisan; he painted buildings for a living, and my mum was a petty trader. I noticed early that my mum was the risk-taker. If my dad didn’t get an opportunity he wanted, he was fine with what he had. He hardly pushed for more, but my mum was different.

She was constantly hustling, seeking new opportunities and exploring additional trades to try. I think I’m more like my mum in that regard. I started hustling at the age of 10.

Tell me about that

I hawked sachet water in the market to make money. I even raised the business capital myself.

Here’s how: I grew up in a rural area with many cocoa farms nearby. Cocoa merchants bought cocoa pods from farmers and dried them in their stores. When these stores closed at night, they’d pack the cocoa inside, but a few cocoa beans would fall on the ground.

Then, the town children and I would go pick up the beans. If we gathered up to one kilogram of the beans, we could sell them for ₦500. If you could gather two or three kilograms, that was very good money. This gathering often took weeks to reach a decent size.

Anyway, I sold my small stash of cocoa beans and started the business. My dad was against it, but I didn’t care. I bought a bowl for ₦130 and a bag of sachet water for ₦100. The first day I started didn’t end well.

What happened?

I didn’t know much about the business, so I made a few mistakes. After I sold the first batch of water, I went to buy more and repeated the process after selling them off. The sun went down, and I ignorantly bought another batch. Everyone who has sold sachet water knows that it was a wrong move because there was no way I’d sell off the water by that time.

When I inevitably couldn’t sell them, people advised that I return the stock to the person I bought it from. Most pure water sellers had agreements with their “suppliers” that allowed them to exchange warm sachet water for cold ones if they couldn’t sell. I tried to do the same, but unfortunately, the person who sold it to me wasn’t a good person. He refused to change them and even beat me up.

Oh my God

It was discouraging. I had to throw the remaining water away because we didn’t have a freezer at home. It was a big loss, and I was only able to start again because my friend gave me ₦200.

I sold sachet water every day after school for about two years. I could make ₦200 – ₦500 profit daily, and that was big money in school. The business also taught me a great deal, particularly how wicked people could be.

A sachet of water cost ₦10, and someone could take the water, drink it, and then give a 10-year-old ₦1000 to go and look for change. They knew I wouldn’t have change for them, and they’d ask me to come back for my money. I never saw them again.

That’s wild

I stopped the business when I was in SS1 or SS2 because my school started dismissing us late at 4 p.m., and I couldn’t keep up.

In SS3, I dropped out of school altogether because my dad couldn’t afford to register me for WAEC. While exploring what else I could do, I decided to apprentice at a business centre since I was naturally skilled with phones and computers. Plus, having briefly worked as an apprentice typist at a similar place a few years prior, it made sense to continue in that line of work. This was in 2014.

The place I worked was popular with lawyers. They often came to type processes and court judgments.

Was it a paid apprenticeship?

No o. I was essentially learning, so I didn’t have a salary. My dad encouraged me to be patient and just get the skill.

I quickly became popular due to my fast typing skills, and the lawyers always wanted to work with me. Some even started asking me to come work for them, offering to pay more than what I earned at the business centre. I couldn’t even tell them I wasn’t being paid.

My popularity didn’t sit well with the business owner; he didn’t like people praising me and always called me weird because I read a lot. I’d install PDF readers on the computers to read random things like philosophy. I often obsessed over learning random things. For instance, I could think about something like YouTube videos and go all in with learning everything about creating them.

So, I was really good. I could say I even knew more than the owner. I worked with him for about two years. During that time, he repeatedly promised to start paying me, but it never happened. I finally left in 2016, because I was considering returning to school and needed to save money. I went on to work with one of the lawyers who’d been trying to poach me.

How much did the new job pay?

₦15k/month to work as a typist for the firm. I also occasionally did some secretarial duties. It was the first time I earned a salary, and the money was okay for me. I was a 17-year-old living with my parents, so I didn’t pay rent or any major bills and was able to save. In 2017, I was able to raise enough money to write WAEC.

Besides the money, working with that lawyer was such a blessing. I still mirror his lifestyle to this day. He was very calm and organised. He taught me how to live a balanced life, and I really enjoyed working with him.

In 2018, while still working with him, I found another income source. One of the other lawyers in the firm gifted me a laptop, and I began using it for research. Every day after work, I’d buy ₦100 data and explore the internet for different things I could learn. I also created a blog using one of the free hosting platforms; I think it was Blogger. I knew it was possible to monetise the blog and start earning from Google Ads, but I also knew it would take a considerable amount of time, effort, and web traffic.

Fortunately, I found a way.

What did you do?

Around this time, a betting company was really popular, and people were always looking for information on how to become a company agent and open a betting shop. So, I wrote a post about the process on my blog and used it to sell an ebook I created about becoming an agent.

My post ranked well on Google, and people started buying my ebook. At first, I sold it for ₦1k, then increased the price to ₦2500 when I noticed it was selling quickly. In a month, I could sell 10 ebooks. At the same time, my blog got monetised, and I could make $100/month — about ₦32k — using Infolinks to display ads. In addition to the ebook sales and my salary, I was making over ₦80k monthly.

I wrote the JAMB exam that same year and had even gotten admission into the university when my income took a hit.

What happened?

Google regularly pushes out updates, and that year, one of these updates hit my site and affected my blog’s traffic. I stopped ranking, and revenue dropped. After gathering all I had (which was about ₦120k), I still needed about ₦350k to complete school payments and rent a place close to campus. The blog wasn’t bringing in money anymore, so I needed to shift direction.

I came across a European site that sold football betting tips for gamblers. The tips were quite expensive at $499/month (approximately ₦140k at the time), and I had a crazy idea of reselling them. I took all the money I had, added my salary and sent it to the guy selling the tips. I could’ve easily been scammed, but fortunately, I wasn’t. The guy added me to a group where he sent the games. I noticed the tips were actually genuine and profitable, but I wasn’t interested in playing them.

Instead, I went on Facebook, made a video and started running ads. In the video, I explained how, instead of $499/month for that site, people could just pay me ₦7k/month for the same genuine tips. I also showed proof that I bought them from the $499 site.

Omo, the kind of money I started seeing.

Too much sense wanted to finish you

My offer was too stupid for anyone to refuse, and people were just buying left, right and centre. I just created a Telegram group, added them, and sent them the games. By the end of the first month, I had almost ₦600k in my account.

The money helped me resume at uni and rent an apartment. I was still young and didn’t know a lot about money, so I was just spending. The iPhone 7 was in vogue at the time, so I bought one. I even changed my laptop.

In early 2019, Facebook started disabling sports betting ads. Luckily, I’d grown an email list of subscribers who trusted me. The thing about betting is, it’s very difficult to find someone who is not a scammer. Since I didn’t scam them, they kept resubscribing. Plus, people were winning too, which was good. Sometimes, they even dashed me money. So, my income was stable and almost passive due to the monthly subscriptions.

However, towards the end of 2019, I suddenly lost interest in the betting business. I don’t know why; I just stopped liking the idea and gradually stopped. My subscribers even reached out asking why I stopped, but I didn’t have a valid reason. That’s how that income source dried up.

Get More Zikoko Goodness in Your Mail

Subscribe to our newsletters and never miss any of the action

Interesting. What did you do next?

My school was close to one of the most prominent markets in Nigeria, so I started going there, looking for products I could sell online and make 3x the cost.

I mostly sold household products. I could buy an item for ₦1k, and list it on JiJi and Facebook ads for ₦4k. That became a major income source for me. I hardly attended class because I was always at logistics companies to sort out deliveries.

The money wasn’t as good as sports betting; that one was unlimited money. I could sell a game one million times. However, with physical products, I could only sell as much as the available stock allowed. Still, I was making around ₦500k – ₦800k monthly, which wasn’t bad. I lived a comfortable life in school.

I’m also glad I started dealing with products instead of relying on sports betting because it set me up for what I do today. I still work with products, just on a very different level.

What do you do these days?

I’d say it’s e-commerce. I look at the market trends and bring in possible solutions in the form of products. For instance, insecurity has been a significant challenge for Nigerians lately. As a business, I can decide to start selling security gadgets, and people would buy in volumes. If I make ₦3k from each gadget and sell 10,000 units, that’s ₦30 million profit.

I use ads to push my products on Facebook, YouTube and MGID. It’s a thriving business now, and I work with a team of 12 people, generating an average monthly profit of around ₦12 million to ₦15 million. The expansion didn’t happen overnight.

In 2020, I recorded my first ₦1 million profit in a single month from selling a specific mosquito product, and we continued to grow from there. We also sold fitness equipment during that period.

The business faced a small struggle in 2021 when Apple released the iOS 14.5 update. It came with a privacy update that made it difficult for third-party platforms to track user behaviour and show them targeted ads. Now, users had to give permission before an app could track their data, and if they clicked “no,” it was all over.

Ad performance was terrible during that period, but fortunately, we started to recover in late 2022, and it’s been going well ever since.

How do the business operations work?

I have a way of knowing that a product will do well. I think it’s a muscle formed by how long I’ve been doing this. After picking the product, we’ll conduct a test run of like 100 units and use the performance data to determine whether we’ll scale or not.

I have an office where I work with a few full-time employees, but I also have agents in different states in Nigeria who get the products and handle delivery. 90% of the orders we receive work with the pay-on-delivery model because Nigerians don’t trust the internet. When the agents deliver, they remit the money to the business.

I decided to operate this way because I believe there’s a limit to how well a business can perform if it’s a one-man operation. If I’m doing it all alone and making a total revenue of ₦100k, 20% net profit of that is just ₦20k. However, if I’m running a ₦100 million business and I achieve that same 20%, I’ve just made ₦20 million.

Both the ₦100k and ₦100 million could be the same personal level of work, but for the latter, I’m using the leverage of getting more people involved to scale faster. It’s better to own the leg of an elephant than a whole ant.

Hmm. That’s a lot to think about. You mentioned a monthly profit of about ₦15 million. How much of that is your income?

After removing operating costs, salaries, and returning capital to the business, my “salary” is usually about ₦5 million to ₦7 million monthly.

I’m specific about always returning money to the business because it’s easy to lose an opportunity if there’s no available capital to allocate to it. I also don’t joke with expansion. Every extra money returns to the business.

You’ve had massive income growth over the years. How has that impacted how you think about money?

I believe fear is a significant reason why many people struggle to make money. It’s the truth. If you don’t take some kind of risk, you won’t make money. Also, money is a reward for helping people out.

If you aren’t solving a need, making someone’s life better or offering value, it’s almost impossible to make money. I never had any doubt about whether I’d make money or not. It was always a matter of time.

How would you describe your relationship with money?

I have a problem. Once people around me start sharing their problems, I feel an obligation to help solve them. Recently, I calculated how much money I’d given out this year, and it was almost ₦10 million. I’m not happy about that, and I plan to stop giving money away so much.

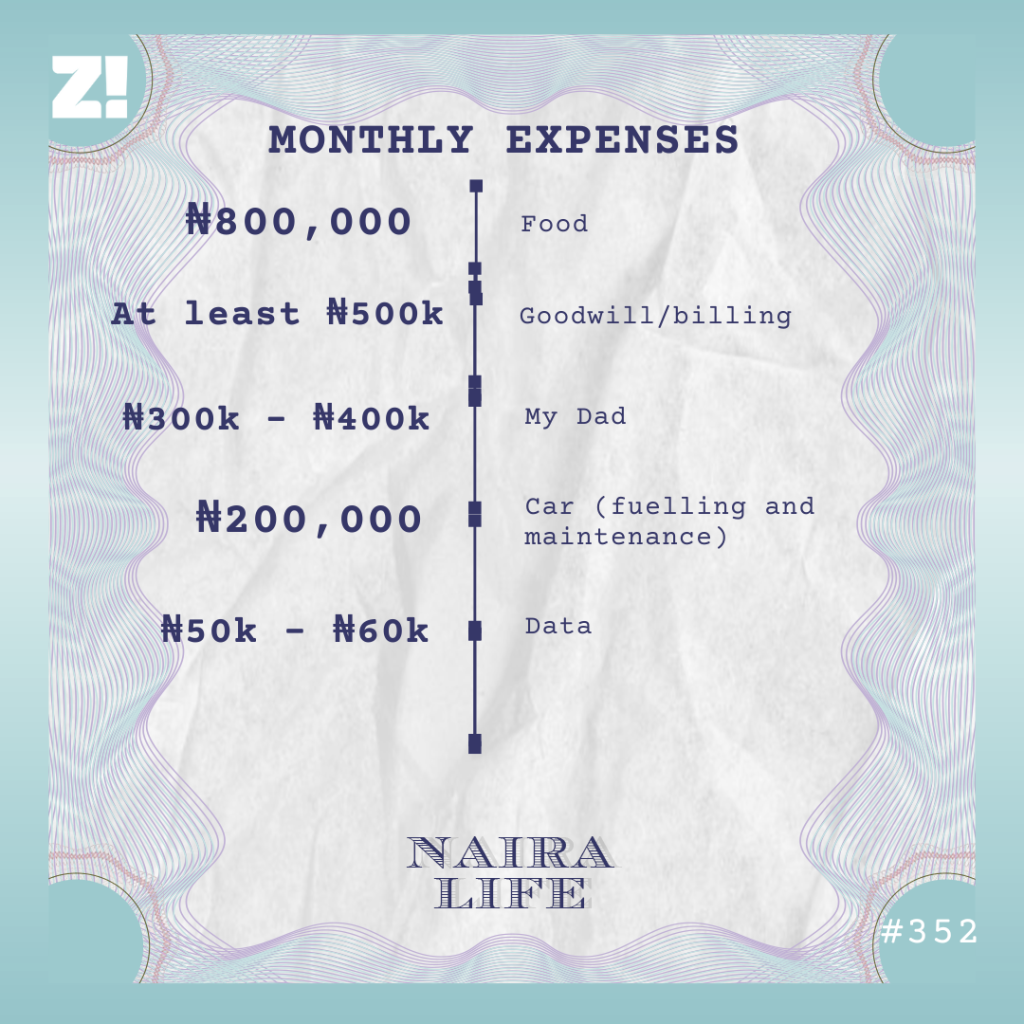

Beyond that, I’m not the materialistic type. My only guilty pleasure is food. It sounds unbelievable, but I spend at least ₦800k on food monthly. It’s that expensive because we (I live with my brother) have a chef whom I pay ₦180k monthly. I also eat out a lot and still spend at least ₦150k on protein powder every month.

Now would be a good time to walk me through your typical monthly expenses

I don’t save money. Whatever reserve I have is reinvested in my business. Another thing that takes my money is travel. I believe travel helps me learn, so I typically spend ₦4m – ₦5m on an annual trip within Nigeria or to an African country. My rent is ₦4 million, but I don’t save for it. Once it’s time, I just pay.

Is there anything you want right now but can’t afford?

Honestly, nothing. I would like to move to the US, but money is not what’s holding me back. It’s the visa; I know it’ll be hard to get as a young person right now.

Is there an ideal amount of money you think you should be earning right now?

I always think in terms of the business, so I think we should be doing a net profit of ₦100 million monthly. We’re currently working towards that, already planning structures and hiring needs to guide expansion to more countries. We already sell in some African countries, but the goal is to scale. By the grace of God, we should have hit over 50% of that ₦100 million goal before 2027.

Rooting for you. What was the last thing you spent money on that made you happy?

A vacation package to Southwest Nigeria in September. It cost me ₦3 million. I’m almost always working, so I don’t go clubbing or things like that, so it’s nice to enjoy travel experiences.

How would you rate your financial happiness on a scale of 1-10?

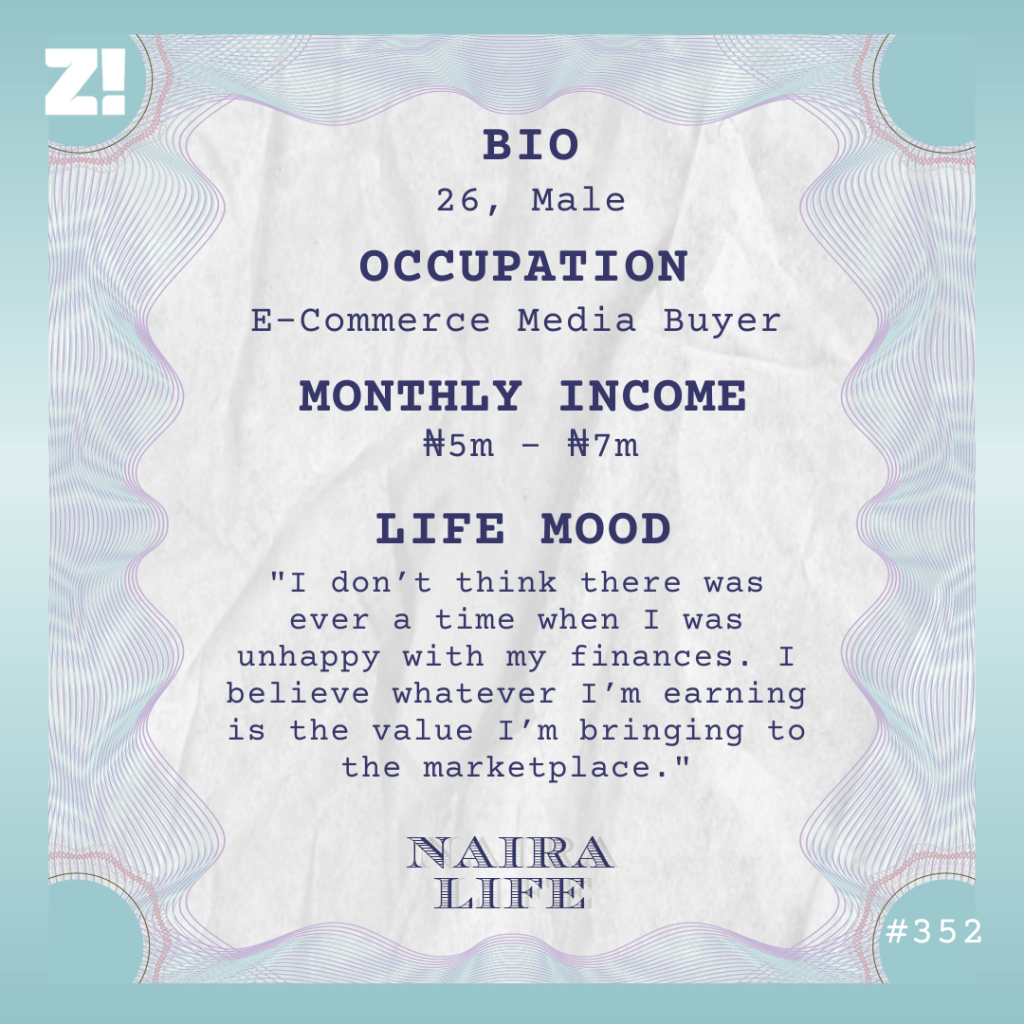

10. Even if you’d asked me this when I earned ₦15k, it’d still be a 10. I don’t think there was ever a time when I was unhappy with my finances. I believe whatever I’m earning is the value I’m bringing to the marketplace. Therefore, if I want to earn more money, I must bring more value. I might sound unconventional, but that’s just the way it is.

If you’re interested in talking about your Naira Life story, this is a good place to start.

Sometimes, life puts you in messy situations where you’re not sure if you’re doing the right thing or not. That’s what Na Me F— Up? is about — real Nigerians sharing the choices they’ve made, while you decide if they fucked up or not.

Amanda* (21) and Happiness* (21) became best friends at the polytechnic, and they remained close even after graduation. When Happiness needed a job, Amanda happily recommended her to her workplace, but that proved to be a wrong decision. Within months, Happiness began to cause trouble at work, leaving Amanda with a tough choice.

When you’re done reading, you’ll get to decide: Did Amanda fuck up or not?

This is Amanda’s Dilemma, As Told To Boluwatife

Sometimes I wonder if I wouldn’t have lost my best friend if I’d just kept my mouth shut and let things play out. But every time I replay what happened, I also understand that silence might’ve cost me my job, or worse, my peace.

Let me start from the beginning.

Before my life became a moral dilemma, I had a simple routine: wake up, go to work at the supermarket on the next street, force myself to smile at customers and count the minutes till closing time. I’d been working as an attendant at the supermarket for about six months, and my relationship with the job was complicated.

While I didn’t love it — being a supermarket attendant wasn’t what I had hoped to do with my Higher National Diploma — it helped me survive. At least, my ₦15k salary helped me “see road” as I jobhunted and tried to save money for NYSC and to continue my education.

So, in March, when my friend of five years, Happiness, complained about being tired of job hunting with no success, I didn’t think twice before recommending her for a job at the supermarket.

When I say “friend,” I don’t mean casual “hi-bye” friendship. Happiness was my best friend. We met in school, bonded over the annoying lecturers in our department, and became inseparable.

Our parents even knew each other through our friendship. Her mum once cooked for me the night my phone got stolen, and I went to her house crying. We shared clothes and passwords; there was nothing we didn’t know about each other. So naturally, I wanted her close. I was excited about the idea of working together and having inside jokes at work.

I connected Happiness with the manager, Mrs Bello, and put my reputation on the line. I’m something of a “manager’s pet” at work because of how good I am at my job. Mrs Bello trusted me a lot, and I only had to assure her that Happiness would be as trustworthy and hardworking as I was. She agreed and employed her.

At first, everything went smoothly. We often worked on the same shifts, so we’d arrange shelves together, gossip during break, and laugh about customers who came in acting like they could afford to buy all of us. It was fun.

However, a few months after she started, strange things began to happen.

Get More Zikoko Goodness in Your Mail

Subscribe to our newsletters and never miss any of the action

Small products, such as snacks, chocolate bars, and random skincare items, would often go missing. Sometimes the cash didn’t tally at the end of the day, and Mrs Bello started side-eyeing everyone.

The first few times it happened, Mrs Bello told us she’d remove the difference from our salaries. Later, the other attendants accused one of us — Miriam, a sweet, quiet girl who always said “sorry” even when you stepped on her. There was no evidence, and she denied it; however, many of the losses occurred during her shift, so Mrs Bello started deducting the money from her salary.

Interestingly, Miriam, Happiness and I often worked the same shifts, but she was the likely suspect. The “manager’s pet” couldn’t steal, and no one expected the person I recommended to do that either.

I even told myself it was the normal store loss. Those things happened a lot. Customers could have stolen the items or a recording error may have caused a difference in the number of items.

But then, one morning, I came in early to set up for a price change and saw Happiness in the back corner. She didn’t notice me at first. She was skillfully sliding a bar of Bounty chocolate into her bag like someone who had rehearsed the move.

Shocked, I confronted her, and she admitted to being behind the recent losses. When she saw the disapproval on my face, she tried to backtrack, claiming it was “just small small things” that she sometimes forgot to pay for. By the time Mrs Bello noticed the loss, she couldn’t admit to taking the item anymore because it’d look like stealing.

When I asked, “So are you comfortable with someone else taking the blame for what you did?” She just shrugged in response and said she wouldn’t do it anymore.

I had no choice but to believe her, so I kept quiet.

I had to believe she was telling me the truth. We’d been friends for years, and I’d never seen her do something like that. Sure, she often took my clothes and shoes without telling me, but I don’t consider that stealing. Friends share clothes all the time.

So, I covered the truth. I kept quiet when two more items went missing over the next few weeks. I kept quiet when Mrs Bello screamed at Miriam again, and the girl resigned out of frustration.

Then Happiness struck again. This time, ₦2k went missing from the register on the night that I, her, and two other ladies worked. Happiness confided in me that she took the money, but she treated the situation like a big joke.

As Mrs Bello ranted about the loss, Happiness kept sharing secret smiles with me and mocking Mrs Bello’s facial expressions.

The whole thing made me really nervous and a little guilty. Since Miriam was gone, what would stop them from blaming me next? If we blamed someone else, would people continue to lose their jobs for no reason? What if I lost my job because I was protecting someone who didn’t even care about the damage she was causing?

Later that night, as we closed, I went up to Mrs Bello and confessed everything. It was clear Happiness wouldn’t change, and I was tired of being in the middle. I assumed she’d just fire Happiness quietly, and I could just pretend not to have anything to do with it.

Unfortunately for me, Mrs Bello publicly lashed out at Happiness and revealed I was the one who snitched. Happiness stared at me with a silent, cold expression, and I immediately wanted the ground to open up and swallow me.

I knew immediately that things would never be the same.

This was in October, and since then, Happiness has blamed me for losing her job and “ruining her reputation.”

She doesn’t pick up my calls or respond to my WhatsApp messages anymore, but she’s constantly shading me on her WhatsApp status, posting things like:

“Beware of friends who smile in your face and stab you behind.”

“Some people pretend to help you, but they only help themselves.”

Our mums have also stopped talking. Her mum called to accuse me of being a bad friend without bothering to listen to my side. My mum feels both mother and daughter are the same and has warned me to stay away from them.

I really miss my friend. I’ve been trying to apologise, but she doesn’t want to hear from me. Was I wrong for speaking up, or should I have just ignored her actions? If I kept quiet, we would still be friends, but I might have lost my job.

Should I have chosen friendship over survival? I ask myself these questions daily, and still haven’t settled on an answer.

*Names have been changed for the sake of anonymity.

The topic of how young Nigerians navigate romantic relationships with their earnings is a minefield of hot takes. In Love Currency, we get into what relationships across income brackets look like in different cities.

Interested in talking about how money moves in your relationship? If yes, click here.

How long have you been with your partner?

My husband, David, and I have been married for five years. We met in 2020 and married that same year.

How did that happen?

I’d just started my service year in Ekiti when the COVID lockdown happened. My parents live in Delta, which is quite a distance from Ekiti. I thought the lockdown would end quickly, so I stayed back, believing it would be a waste of money to go home.

At that point, I was already a member of David’s father’s church, and the church helped corps members who didn’t want to go home find accommodation with church members. I stayed with a lady who lived close to David’s house, and almost every day, he would visit me, bearing food.